If you still had any belief in an "efficient" market, Wednesday and Thursday ought to have cured you.

As I've written here in a prior post, there are two ways markets can be inefficient. I believe this week demonstrated both.

On Wednesday, some data was reported which showed a small rise in core inflation. This had even been commented on, a priori, by no less a person than Bernanke, as expected. So much for 'new information.' Never the less, it caused a market sell off.

If the information was not all that unexpected, how can one explain an "efficient" market dropping by 1.7% ? With individual stocks declining far more just on principle. Hardly very "efficient," eh?

Then, on Thursday, the continued confusion resulted in a flat market. Until Fed official Poole remarked that, at their next meeting, the Fed might raise rats half a point, or maybe, not at all.

This caused an immediate panic of selling. The market sold off to end the session roughly another .7% down.

Mind you, Poole only voiced what most pundits believed, and even Bernanke has said. That the Fed is looking at evolving data, and will make its decision at the appropriate time, on the relevant data at that time. Nothing new here.

No, this further drop was the result of a lot of mediocre, poorly-reasoning investors dumping shares on fear. Nothing more.

There's no sign yet that healthy global growth has lapsed. Any inflation is demand pull, not cost push. If global demand ebbs a little to cool the commodities price froth, so be it. That won't bring construction in Chindia to a standstill anytime soon.

Simply put, nothing "happened" this week to cause the equities of well-managed, profitable, growing large-cap US firms to drop in value by 10%. Temporary perception may be that these companies are now worth much less. But the available information on the environment, and the companies themselves, suggest otherwise.

So much, again, for "efficient" markets. How efficient can they be, if little, or no, information, can bring changes of the scale seen in just two days this week. And how "equal" can all the investors be in processing this "information," if such a stampeded is caused? And then reversed again today, by almost half a percentage point in the opposite direction?

Thursday, May 18, 2006

Wednesday, May 17, 2006

Dell Again: The WSJ Almost Gets It Right

Suffice to say, I feel prescient regarding my comments about Dell's performance, both recently, and beginning in the 1990s. Yesterday's Wall Street Journal "Portals" column by Lee Gomes echoed my points exactly.

What was particularly nice was his mention at the end of his piece of three pairs of companies whom I, too, have discussed recently: AMD & Intel, Google & Microsoft, HP & Dell.

However, whereas I attribute the performances to Schumpeterian dynamics, Gomes, who is primarily a technology writer, merely writes, "something seems to be in the air: Formerly bulletproof business models are fissuring under the pressure of new and unexpected competition."

Well, unexpected if you don't read Schumpeter, and/or have the benefit of my proprietary performance research using thousands of large-cap equity observations over many years. Or haven't bothered even a cursory look at the fate of top technology companies going back to even just the 1960s.

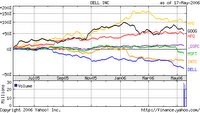

Too, Gomes only references a very short timeframe when he writes, "If you chart the stock performance of Dell vs. H-P over the past year, you get a sideways V, with the trend lines moving in opposite directions, and Dell on the bottom heading lower." He mentions the other pairs, listed above, as having similar relationships of charted performance. I've included a Yahoo-sourced chart of all pairs on the left. The S&P500, by the way, bisects the pairs, three above, three below, for the one-year view.

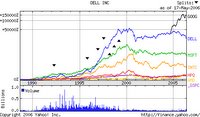

Now, look at a much longer term chart of the same companies, again, with the S&P500 for reference.

What was particularly nice was his mention at the end of his piece of three pairs of companies whom I, too, have discussed recently: AMD & Intel, Google & Microsoft, HP & Dell.

However, whereas I attribute the performances to Schumpeterian dynamics, Gomes, who is primarily a technology writer, merely writes, "something seems to be in the air: Formerly bulletproof business models are fissuring under the pressure of new and unexpected competition."

Well, unexpected if you don't read Schumpeter, and/or have the benefit of my proprietary performance research using thousands of large-cap equity observations over many years. Or haven't bothered even a cursory look at the fate of top technology companies going back to even just the 1960s.

Too, Gomes only references a very short timeframe when he writes, "If you chart the stock performance of Dell vs. H-P over the past year, you get a sideways V, with the trend lines moving in opposite directions, and Dell on the bottom heading lower." He mentions the other pairs, listed above, as having similar relationships of charted performance. I've included a Yahoo-sourced chart of all pairs on the left. The S&P500, by the way, bisects the pairs, three above, three below, for the one-year view.

Now, look at a much longer term chart of the same companies, again, with the S&P500 for reference.

The slopes of the lines approximate the total returns for these stocks, as their dividends tend to be minimal. While it is clear that things never returned to pre-bubble levels for Dell, Intel, and Microsoft after 2000, the stories for the other three are by no means all alike.

What this view demonstrates is that Dell, Intel and Microsoft have taken their shareholders to places AMD and H-P have yet to go, and Google has been for a still-brief time. You have to give the former triumvirate their due for wringing tremendous shareholder returns out of a decade of dominance of the PC market.

To look at just the last year and pronounce them failures, and that 'something seems to be in the air,' is to misunderstand the fundamental nature of company and product lifecycles in technology sectors. Dell, Intel and Microsoft steamrolled their competitors in their heydays. But those days are over. And what is occurring now is by no means "unexpected."

Further, it's not like all three better performers have blunted the older business models of the now-worse-performing three firms. HP has only managed to regain traction in its markets, and to quote an old song, "been down so long, it looks like up to me." AMD has taken advantage of Intel's inability to now manage further technological hegemony in chip making with its resultant size and diversity of product/markets. But AMD languished for decades as a poor performer prior to this.

Google is the one company which represents a greenfield entry which has piggybacked on the environment created by Microsoft, Intel and Dell. But it is also the shortest-lived case of the six. I would say the jury is still out regarding the long term path Google will actually take.

In conclusion, Gomes does a nice job highlighting the recent, resulting total returns and business situations of these pairs of competitors. However, in expressing surprise, he unfortunately displays a shallow grasp of fundamental business dynamics discovered 80 years ago by Joseph Schumpeter. I think we can expect more from a featured columnist of the country's best business daily.

Don't you?

"Forget the S&P" as a Benchmark ?

My partner recently called my attention to Jonathan Clement's piece in the Wall Street Journal which decried the use of the S&P500 as a performance benchmark for portfolios. Actually, it's not quite that simple. Clements seemed to both lampoon the use of, and then use, anyway, the S&P500 as a performance benchmark for various fund styles, and whole portfolios of multiple instruments.

My partner lamented, and I agree, the piece was so obtusely written as to almost defy analysis, let alone understanding.

Mr. Clements begins by stating that many readers of his column have contacted him to crow about their investments having beaten the S&P recently. Clements goes on to state that,

"... I don't believe they're investment geniuses. Here's why beating the S&P 500 is no great accomplishment......In fact, if you haven't outpaced the S&P 500 over the past five or six years, something is likely seriously wrong with your investment strategy. After all, as part of a well-diversified portfolio, you ought to spread your money across large stocks, smaller companies, foreign markets and bonds. Any mix of that kind should have handily beaten the S&P 500."

Well, yes. Let's just forget about risk, and timing. And while we're at it, lets compare the return of various asset classes as if they are all equal. And the brief time period over which the observations are taken.

Clements bounces between lecturing on using the proper benchmark for each type of investment and mutual fund style, and then saying you should compare your entire investment return, across all instruments, to the S&P500. On that basis, he dismisses outperforming the S&P as child's play.

Later, in the article, he talks about how is IRA account has handily beaten the S&P, but then admits its is in "small stocks and foreign markets, both of which have easily outpaced the S&P 500."

Again, let's forget about how much more risk is typically found in foreign markets, or small stocks, too, for that matter. It's not a fair comparison by any means, and certainly not significant over very short timeframes.

Professional portfolio managers undrestand that the S&P500 is an appropriate benchmark for large-cap equity portfolios. Period. For hedged funds, it's cash. For bond funds, I would guess it's some variant on a popularly tracked bond index. Why Clements thinks anyone has implied more than this is beyond me.

What dismays and disappoints me about this muddled, wrong-headed piece by Clements about investment performance, is that it's in a large, broadly distributed, reputable business daily- the Wall Street Journal. And Clements writes a weekly column on investing.

With "help" like this, you wonder if most individuals can just preserved their capital over time, let alone actually make money. We see now just how sadly missed Lou Rukeyser will be.

My partner lamented, and I agree, the piece was so obtusely written as to almost defy analysis, let alone understanding.

Mr. Clements begins by stating that many readers of his column have contacted him to crow about their investments having beaten the S&P recently. Clements goes on to state that,

"... I don't believe they're investment geniuses. Here's why beating the S&P 500 is no great accomplishment......In fact, if you haven't outpaced the S&P 500 over the past five or six years, something is likely seriously wrong with your investment strategy. After all, as part of a well-diversified portfolio, you ought to spread your money across large stocks, smaller companies, foreign markets and bonds. Any mix of that kind should have handily beaten the S&P 500."

Well, yes. Let's just forget about risk, and timing. And while we're at it, lets compare the return of various asset classes as if they are all equal. And the brief time period over which the observations are taken.

Clements bounces between lecturing on using the proper benchmark for each type of investment and mutual fund style, and then saying you should compare your entire investment return, across all instruments, to the S&P500. On that basis, he dismisses outperforming the S&P as child's play.

Later, in the article, he talks about how is IRA account has handily beaten the S&P, but then admits its is in "small stocks and foreign markets, both of which have easily outpaced the S&P 500."

Again, let's forget about how much more risk is typically found in foreign markets, or small stocks, too, for that matter. It's not a fair comparison by any means, and certainly not significant over very short timeframes.

Professional portfolio managers undrestand that the S&P500 is an appropriate benchmark for large-cap equity portfolios. Period. For hedged funds, it's cash. For bond funds, I would guess it's some variant on a popularly tracked bond index. Why Clements thinks anyone has implied more than this is beyond me.

What dismays and disappoints me about this muddled, wrong-headed piece by Clements about investment performance, is that it's in a large, broadly distributed, reputable business daily- the Wall Street Journal. And Clements writes a weekly column on investing.

With "help" like this, you wonder if most individuals can just preserved their capital over time, let alone actually make money. We see now just how sadly missed Lou Rukeyser will be.

Tuesday, May 16, 2006

Gates' and Otelilini's WSJ Op-Ed Piece

Yesterday's Wall Street Journal featured an op-ed piece jointly written by Bill Gates, "chairman and "chief software architect of Microsoft," and Paul Otellini, president and CEO of Intel.

Their letter was apparently a rejoinder to a piece in the WSJ's technology column, written by Walt Mossberg, extolling Apple's 'closed system' approach as now edging out the older, Wintel 'open system' in terms of popularity.

What I find very telling is the authors' confusion between the continued usage of PCs, and their ability to command premium value anymore. It's not so much the "end of the PC era," anymore than the influx of Japanese imports marked the "end of the automobile" era.

As I've written previously in my blog, both Microsoft and Intel are at the end of long periods of having dominanted their respective product spaces. By virtue of their dominances, they have changed the environment within which their firms, and their products, operate.

I don't think anyone seriously believes PCs and laptops are going away anytime soon. However, just like modern automobiles, though, they will probably last longer, offer more features for less money, and, in general, work better with other devices than they have in the past. The pace of replacement of boxes and operating systems is certainly slowing now, in comparison to the past.

If these trends were not occurring, then the PC probably would become obsolete, due to its having walled itself off from the need for customers to connect various devices and media across the internet and their own systems. As it is, the value-adding damage has already been done to PC systems and their software and hardware components.

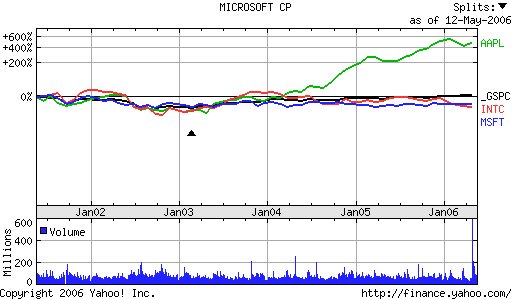

See the chart at the top of this piece for the visual confirmation. It shows Apple pulling away from Microsoft, Intel and the S&P500 beginning in 2004.

It would be fun to speculate on the discussions leading up to the WSJ letter by Gates and Otellini. Better still, to listen in on their conversations and see the drafts. Clearly, they felt a gauntlet had been thrown down, challenging their companies' relevance as being at the heart of today's digitalization trends. It's noteworthy that all it took was a guy who writes a weekly technology column in a business newspaper to spark this reaction from the two company leaders.

Gates' and Otellini's protestations notwithstanding, there is far more activity in application-specific digital devices (digital music players, cellphones, PDAs, etc) and internet connectivity than there is in necessary, but basic, PC systems. Rather than, as their piece asserted, it being the "end of the beginning" for the PC, it may simply now mark the arrival of the device as a low-priced electronic appliance with little more capacity for functionality growth that is not due to some other devices produced by other companies.

Monday, May 15, 2006

HP "vs" Dell

Last week, CNBC made much of Hewlett-Packard's recent short-term revival, and contrasted it with Dell's recent weakness. The latter's revenues have been falling short of expectations, and its total returns are no longer consistently market-beating. I even wrote recently of the positive signs in the nature of the way Mark Hurd seems to be changing HP.

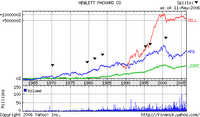

As the five-year price chart from Yahoo above clearly shows, HP has been on a consistently superior total return path for nearly 5 years, and from a serious trough for the last 3-4 years. In contrast, Dell has been flat or declining, both absolutely and relatively, for about 2 1/2 years.

Yes, for the recent period, Dell has seemed played out. Exhausted in the sense of a business model with little headroom for profitably surprising the market.However, as I observed about Intel recently, let me do so for Dell now. Take a look at the Yahoo-sourced long term performance chart below.

For an entire decade, Dell out-performed HP, the S&P500, and not a few other tech companies with its solid business concept and nearly-flawless execution thereof. Isn't a decade enough? This company has excelled, in what should have been, and was, a very tough product/market segment, for much longer than should have been expected. Than is the norm.

To look at just the last 5 years is to seriously misunderstand both business history, and Schumpterian dynamics. Dell is probably not "coming back," anymore than Microsoft or Intel are. That is, it's unlikely that any of the three will soon post a consistently superior total return record, versus the S&P500, on the back of consistently superior revenue growth.

But this in no way diminishes their prior accomplishments. In fact, it is those accomplishments which have brought them to this point. Microsoft has played out its "technology," for the most part. Intel is stretched amongst separating customer segments, while its once-weaker rival, AMD, focuses on profitable opportunities with laser-like precision. Dell simply has little room left to exploit its vaunted direct-sales model, amidst the increasing commoditization of its main products, desktop and laptop PCs.

The funny thing about the second chart, to me, at least, is that, if not for Dell, you'd think HP had done very well. And never really "in trouble" until these last few years. It just shows how moderated our expectations can get, and how we sometimes forget what "really" excellent performance looks like.In fact, in hindsight, you would have been happy holding both for a decade.But who knew in advance? And, of course, it's always easier in hindsight to see the end of a holding period than it is when you're actually doing it.

Subscribe to:

Posts (Atom)