Carlos Goshn, CEO of Nissan and Renault, appeared yesterday in an interview on CNBC with that network's talking head, Maria Bartiromo. His visit was no doubt a coup for the network, as Goshn is now the most sought-after executive in all of the automotive sector.

Kirk Kerkorian, GM's largest, and predatory, shareholder, is desperately trying to find a way that Mr. Goshn can, effectively, run GM. To that end, Kerkorian and his associate, now GM board member, Jerry York, have proposed that GM enter an alliance with Nissan/Renault, thus hopefully securing Goshn's services on GM's behalf.

Judging from Goshn's statements in the interview, Kerkorian had better start praying that something else comes along to help GM and its stock price. Because Carlos Goshn made it crystal clear that he had no spare time for GM. However, most interesting were his remarks on what an alliance does for the parties involved.

Goshn explained that while such an alliance might help GM with shared parts, engines, perhaps platforms and designs, each alliance member is responsible for fixing their own company's problems.

Thus, Goshn ruled out being the white knight to come riding in, replace Rick Wagoner, and rescue GM. At best, he left the door open for GM to join the Nissan/Renault alliance, swap equity stakes, and help itself with access to knowledge from the other two members.

I'd say this puts another nail in GM's coffin for the long term. While Rick Wagoner may not be out of a job because of this proposed alliance, he may well be out of a job due to continued unsolved problems and lackluster performance at GM.

Goshn came off as a very resolute, no-nonsense, pragmatic and realistic executive. Pretty much the opposite of Wagoner. I can see why Goshn solved Nissan's problems. And from some of his remarks, I think, were he to actually assume the title of GM CEO, he'd "rescue" GM by carving out a much-reduced core company of decent products and cost structures, while summarily shedding much of the giant's outmoded asset and personnel bases.

It should be very interesting to watch Kerkorian's moves during the rest of the summer, as the alliance discussions and subsequent maneuvers pan out. But, suffice to say, I wouldn't go buy GM stock based upon what I heard from Goshn yesterday.

Friday, July 14, 2006

Thursday, July 13, 2006

Free Media Publishing Leaps Into Video

Bill Gates Praising the Mac

Here's a little example of why Time Warner and other "old" media conglomerates are in trouble. It's a video clip of a much younger (than now) Bill Gates at an Apple developers conference. I found it on YouTube, and linked it to this blog post. Mostly just to demonstrate a point about technological advances in free online publishing.

I wrote a piece about YouTube recently. It's the online video clip site which functions somewhat like ShutterFly or PhotoBucket. My consulting friend S remarked to me the other day that YouTube allows clips to be linked to blogs. In her words, now "everybody is a star." Or soon could be.

She and I have debated the coming integration of online video entertainment and broadcast/cable content. YouTube adds another interesting bit into the mosaic.

Consider what has now happened.

This blog is free to you and me. Google supplies Blogger for free, even without the ads. Dominating more content in a surging product/service space is reasonable strategy, if the basic cost of doing so is buying more servers. I eventually realize something like the price of a cup of coffee for any click-through revenue from the ads on this blogsite.

Now, YouTube seamlessly links its clips to Blogger. Anyone who shoots digital video of interest can post it for free on YouTube. Competition for content has become so stiff already, that YouTube's competitors, such as Revver, are paying people larger slices of ad revenues to post videos on their site.

This morning, the on-air staff of CNBC held a hand-wringing debate over blogs. Apparently, there was a recent incident in which some blogger posted false information about a company, and its stock price suffered.

Aside from the hilarity of an entertainment show like SquawkBox, the show on which the 'debate' aired, treating blogs from a 'news' standpoint, their discussion demonstrates how much reach independent, "free" published media now may have.

Commentary and editorial blogs, such as this one, are unlikely to be running afoul of any laws regarding insider trading. With increasing amounts of online media available on which to comment, and a free base of operations, how much value added can large media conglomerates create anymore, outside of pure entertainment? It seems even they can't make their news operations pay for themselves. And commentary can be published by anyone for free.

Granted, distribution is a challenge. But it's a far cry from a decade ago, when it wasn't even feasible for someone to write a daily "column" without a syndicated deal with a newspaper chain.

If I wanted to, I could "cast" this blog in video, and post it, without cost, on iTunes or YouTube. In the case of YouTube, I can automatically link my video back here to a post. Somebody else's business model is paying for all the transmission bandwidth, disc storage, and server processing to make this happen. In fact, Google's, and other new media firms' business models are all about generating revenues from viewers, not providers. And not even making the viewers pay directly or explicitly, but, rather, through advertising.

Now, where did I see this before? Oh, right. It's the new version of the "old" televsion business model. Except, this time, it's eviscerating broadcast television.

With the arrival of direct viewing of media content on your television, from the internet, cable revenues from "repackaging" content from "channels" and networks will begin to suffer as well.

My, how times have changed. Now, I can read or hear a story, or view a clip, and write about it the same day. Even link, in many cases, to the story or clip. As I did in my recent piece about Jack Welch in Fortune Magazine. Or downloaded this Bill Gates clip from YouTube.

In a world that supports and embraces this sort of inexpensive integration of multi-media, editorializing, and analysis, what does that portend for the media giants of our time- NewsCorp, Time Warner, McGraw-Hill?

Consider what this integration means to the music divisions of media conglomerates, such as Time Warner. Would a new band not now be able to digitally shoot a video of their performance, and post it free to YouTube? Then link the video(s) to their website, and publish the website URL at their concerts? Then go straight to iTunes with the content they record from digital tools on their iMacs, and....voila! Where's the big publishing giant in the middle? Gone.

Suffice to say, I'll be surprised if any of them appear in my portfolio's selections of consistently superior, high-growth companies.

Here's a little example of why Time Warner and other "old" media conglomerates are in trouble. It's a video clip of a much younger (than now) Bill Gates at an Apple developers conference. I found it on YouTube, and linked it to this blog post. Mostly just to demonstrate a point about technological advances in free online publishing.

I wrote a piece about YouTube recently. It's the online video clip site which functions somewhat like ShutterFly or PhotoBucket. My consulting friend S remarked to me the other day that YouTube allows clips to be linked to blogs. In her words, now "everybody is a star." Or soon could be.

She and I have debated the coming integration of online video entertainment and broadcast/cable content. YouTube adds another interesting bit into the mosaic.

Consider what has now happened.

This blog is free to you and me. Google supplies Blogger for free, even without the ads. Dominating more content in a surging product/service space is reasonable strategy, if the basic cost of doing so is buying more servers. I eventually realize something like the price of a cup of coffee for any click-through revenue from the ads on this blogsite.

Now, YouTube seamlessly links its clips to Blogger. Anyone who shoots digital video of interest can post it for free on YouTube. Competition for content has become so stiff already, that YouTube's competitors, such as Revver, are paying people larger slices of ad revenues to post videos on their site.

This morning, the on-air staff of CNBC held a hand-wringing debate over blogs. Apparently, there was a recent incident in which some blogger posted false information about a company, and its stock price suffered.

Aside from the hilarity of an entertainment show like SquawkBox, the show on which the 'debate' aired, treating blogs from a 'news' standpoint, their discussion demonstrates how much reach independent, "free" published media now may have.

Commentary and editorial blogs, such as this one, are unlikely to be running afoul of any laws regarding insider trading. With increasing amounts of online media available on which to comment, and a free base of operations, how much value added can large media conglomerates create anymore, outside of pure entertainment? It seems even they can't make their news operations pay for themselves. And commentary can be published by anyone for free.

Granted, distribution is a challenge. But it's a far cry from a decade ago, when it wasn't even feasible for someone to write a daily "column" without a syndicated deal with a newspaper chain.

If I wanted to, I could "cast" this blog in video, and post it, without cost, on iTunes or YouTube. In the case of YouTube, I can automatically link my video back here to a post. Somebody else's business model is paying for all the transmission bandwidth, disc storage, and server processing to make this happen. In fact, Google's, and other new media firms' business models are all about generating revenues from viewers, not providers. And not even making the viewers pay directly or explicitly, but, rather, through advertising.

Now, where did I see this before? Oh, right. It's the new version of the "old" televsion business model. Except, this time, it's eviscerating broadcast television.

With the arrival of direct viewing of media content on your television, from the internet, cable revenues from "repackaging" content from "channels" and networks will begin to suffer as well.

My, how times have changed. Now, I can read or hear a story, or view a clip, and write about it the same day. Even link, in many cases, to the story or clip. As I did in my recent piece about Jack Welch in Fortune Magazine. Or downloaded this Bill Gates clip from YouTube.

In a world that supports and embraces this sort of inexpensive integration of multi-media, editorializing, and analysis, what does that portend for the media giants of our time- NewsCorp, Time Warner, McGraw-Hill?

Consider what this integration means to the music divisions of media conglomerates, such as Time Warner. Would a new band not now be able to digitally shoot a video of their performance, and post it free to YouTube? Then link the video(s) to their website, and publish the website URL at their concerts? Then go straight to iTunes with the content they record from digital tools on their iMacs, and....voila! Where's the big publishing giant in the middle? Gone.

Suffice to say, I'll be surprised if any of them appear in my portfolio's selections of consistently superior, high-growth companies.

Stop the Presses: Goshn & GM

Yesterday's Wall Street Journal carried a very illuminating piece on Carlos Goshn, Renault, and the potential alliance between Renault, Nissan and GM. This is Kirk Kerkorian's hopeful gambit to exit his considerable position in GM stock at a profit.

What the Journal pointed out, however, is that, while Goshn did turn around Nissan, as he promised, he hasn't yet succeeded with Renault. After 18 months of work, according to the article, Renault is still valued at zero, awaiting Goshn's magic touch. The other pieces of the alliance allegedly comprise the value of the outstanding stock, indicating that investors are awaiting Renault's rehabilitation.

What this means, as the article pointed out, is that GM & Kerkorian may have to wait in line for quite a while for this alliance to develop. Or to show results, if it does develop.

Maybe Rick Wagoner doesn't have much to worry about from Goshn & Co. just yet. And maybe I was premature in suggesting, earlier this week, that my prediction of one less CEO in Detroit is nearing reality faster than I had expected.

Still, it's not good news for GM's shareholders. I think the suggestion of the alliance simply puts GM in the "intensive care" unit for the forseeable future. And as I've written before, I would not look to the prior and current management team to fix what they messed up, on such a large scale, to begin with. My guess is that this new revelation about Goshn's capacity to help GM means the latter will likely be foundering a while longer.

In any case, it highlights a potential pitfall in GM's path out of its misery. And its shareholders are by no means out of the woods yet, by a long shot.

What the Journal pointed out, however, is that, while Goshn did turn around Nissan, as he promised, he hasn't yet succeeded with Renault. After 18 months of work, according to the article, Renault is still valued at zero, awaiting Goshn's magic touch. The other pieces of the alliance allegedly comprise the value of the outstanding stock, indicating that investors are awaiting Renault's rehabilitation.

What this means, as the article pointed out, is that GM & Kerkorian may have to wait in line for quite a while for this alliance to develop. Or to show results, if it does develop.

Maybe Rick Wagoner doesn't have much to worry about from Goshn & Co. just yet. And maybe I was premature in suggesting, earlier this week, that my prediction of one less CEO in Detroit is nearing reality faster than I had expected.

Still, it's not good news for GM's shareholders. I think the suggestion of the alliance simply puts GM in the "intensive care" unit for the forseeable future. And as I've written before, I would not look to the prior and current management team to fix what they messed up, on such a large scale, to begin with. My guess is that this new revelation about Goshn's capacity to help GM means the latter will likely be foundering a while longer.

In any case, it highlights a potential pitfall in GM's path out of its misery. And its shareholders are by no means out of the woods yet, by a long shot.

Wednesday, July 12, 2006

Jack Welch's "Way" Returns to the Spotlight

Today marked the first time in ages that Jack Welch has made an appearance on CNBC.

The occasion was to discuss this article, recently published as the cover story in Fortune magazine. It contends that Jack Welch's "rules" are now out of fashion. That he was a star CEO for the 1990s, but is now passe.

This morning, Welch appeared on CNBC, in a polo shirt, with a lush pastoral scene as a background, from Nantucket. Clearly, Welch chose to rebut the article in the role of retired, wise ex-CEO, rather than suited defender of a track record.

There are several aspects to this topic. One is Fortune's article. The next is Welch's rebuttal. And, finally, there is Welch's actual performance, which is purportedly the basis on which his now controversial views were built.

Betsy Morris' piece is of a mixed nature, in my opinion. While some of her "new rules" are different than Welch's explicit pronouncements, they are not necessarily things with which he would have, or now does, disagree: organizational agility, focus on building niche markets, hiring passionate people, and looking outward from the company.

Morris' "old rules," attributed to Welch, smack of being straw men. I don't personally recall Welch saying any of them verbatim as presented, except for the time honored, still-relevant advice to be #1 or #2 by market share, rather than compete as a distant also-ran. So in this case, Morris probably overstepped herself.

In the main, though, I think her points are well taken. She restated and sharpened them on CNBC this morning, appearing about 20 minutes before Welch did. She essentially noted that Welch and his 'six sigma' preoccupation tended to focus on wringing efficiency from existing businesses. She opined that today, popularly-lauded companies such as Apple and Google rapidly design and release whole new categories of products and services, whereas GE tended to carefully crawl along, grinding out steady earnings increases, rather than torrid product change and revenue growth.

Now, to Welch's reply. He first dismissed the whole matter as directed 'against my wife, Suzy, and me, because we write a weekly column for BusinessWeek, Fortune's competitor.' Then he also dismissed remarks by United Technologies CEO George David, reputed to rebuke Welch, as taken "out of context."

After these qualifiers, Welch essentially lampooned Morris' list of "old rules," and claimed that, in fact, her "new rules" are, in reality, his. And were all along. Welch steadfastly disputed that 'his era' is over, or that his approaches, as CEO, would no longer work, 5 years after his retirement.

A few comments on the matter thus far. Nobody but Jack Welch mentioned his current wife ( #3?) in all of this. Suzy didn't run GE for more than a decade- Jack did. Frankly, I don't really believe anyone else cares what Suzy Welch does or does not think about management.

It's unlikely that Jack Welch would have been against Morris' "new rules," provided that they ground out earnings which fit Welch's GE management style. However, they clearly were not his major foci while leading GE.

My revered mentor, an ex-GE senior planning exec, and Chase SVP of Corporate Planning, used to say, "there are hundreds of business aphorisms, some contradictory. The question at hand is, which are relevant in this situation, for this business."

That's really the nub of the Welch tempest right now. Morris is trying to say, 'Welch never said 'nimble,' so he's against it, and now it's important.' Welch is saying, 'only an idiot would be against a nimble company- I was always for 'nimble.'

Frankly, neither is totally correct. But, on balance, I think Morris is right.

Frankly, neither is totally correct. But, on balance, I think Morris is right.

Despite Morris' citing companies which are, themselves, not consistently superior in growing and delivering total returns to shareholders, I believe she is right in applauding the focus on raw revenue growth and market creation which is shared by companies like Apple, Google, or Gilead.

As I have written before, in this blog, size, by itself, is of little value anymore. Witness GM and Ford. IBM and Microsoft. Intel.

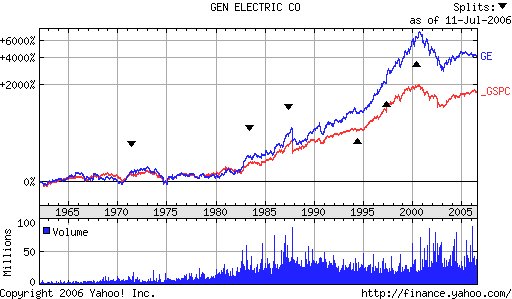

As the chart at the top of this post illustrates, even Welch didn't really manage GE to consistently outperform the S&P over his tenure, from 1981 to 2001. He had a few brief periods of radical outperformance, notably his restructuring of the firm upon his accession to the CEO post. For the most part, GE has never been a highly-consistent growth company which has outperformed the index (GE has never made my portfolio's list of consistently superior performing companies among the S&P500 candidates). I pointed this out to Welch, in person, in a meeting in the mid-1990s. He was shocked, and, literally, speechless for a few minutes, as he studied a chart I presented which showed GE's share price against the Dow-Jones since he took over GE. His comment, when he next spoke, was, "nobody's ever shown me this chart before." Suffice to say, the chart demonstrated that Jack had not added all that much comparative value for his shareholders over his tenure to that point.

As I wrote in a prior post, the most value Welch ever created for his shareholders, comparatively, with the market, was his brilliant triage of the sluggish firm he inherited from Reg Jones, amidst the worst inflationary environment of the modern US business era. The Jones era, for GE, was, as the chart above shows, dismal. Welch revitalized a tired company which had lost its focus and direction. However, owning GE didn't reliably provide equity investors with consistently superior growth and return prospects, as holding many other S&P components would have, over the past 20 years.

Among all of Welch's portfolio of businesses, GE Capital was the only really reliably high-growth unit. Upon taking over GE, Immelt was assailed by critics who suddenly had the scales fall from their eyes, and realized how heavily leveraged the unit was. Somehow, Welch managed to sprinkle magic dust over this easily-observed fact, during his tenure as CEO. Immelt suffered for the clever diversion of analysts' attention to predictable quarterly earnings sans consistently superior topline revenue growth for the firm.

So, for me, this whole episode, while entertaining (hey, it's on CNBC- what'd you expect?), is moot. Welch's GE was never one of those rare, consistently superior growth and return companies which are the hallmark, and components, of my investment portfolios. Arguing over "his rules," is, in my opinion, totally beside the point. If he'd run a more impressively-performing company, I'd feel differently.

But Welch didn't, so I don't.

Tuesday, July 11, 2006

Ford's "Way Forward" in Brazil

Yesterday's Wall Street Journal featured an article about Ford's "Way Forward" program successes in Brazil.

I have to say, I was unimpressed with what it portends for the giant auto maker.

To distill the well-written article to its essence, the Brazilian unit of Ford has scored major gains with a new SUV model by doing two things: sensibly restructuring the physical manner in which they produce the car, and doing intensive consumer market research to design a car which the relevant market segment will buy, at a profitable (to Ford) price.

The good news, of course, is that some people at Ford down in Brazil, led by one Luc de Ferran, pulled this off. It's inspirational, and certainly better, as the saying goes, "than a sharp stick in the eye."

However, the bad news is that this "turnaround" at Ford Brazil is nothing fancy. Basically, the unit had fallen on extremely bad times, and simply rediscovered what, I believe, intelligent business people everywhere would acknowledge are obvious maxims.

They redesigned manufacturing to adapt to current realities, thus cutting wasted time and expense. They returned to classic marketing in the design of a new vehicle, using consumer research to uncover wants and needs, the incorporation of which, in the new Ecosport SUV, caused the car to gain an 80% market share.

This anecdote brings me to recall some of my prior posts regarding mediocrity and ineptitude in the general business environment. Specifically, this post about UAL, this one about Starbucks, and this one about Intel v. AMD.

Why is that Ford's Brazilian unit, or, for that matter, Ford itself, globally, must have its back to the wall in order to rediscover basic business sensibilities?

I suspect that the reason boils down to one word- discipline.

In a process which parallels Aristotle's thoughts on the decline of governmental systems from the pinnacle, the 'philosopher-kin' phase, I think corporate leadership/management undergoes something very similar.

When a company is "on top," competitively and in terms of consistently delivering superior total returns for shareholders, a sense of complacency begins to set in. The questioning, innovative behaviors which probably drove the company's success, begin to be institutionalized by a second tier of acolytes as 'revered processes.' The originators of the initial success move on- retirement of the lauded CEO, perhaps a few SVPs move to head other companies. Too, some of the wizards of the successful change are promoted, focus upward, and leave the nuts and bolts continuation of the success to less-capable subordinates. The new generation of leaders begin to do two things: view the changes wrought by the earlier successful managers as 'codes to live by,' missing the fundamental value of the changes having led to success, not the particular endpoint of the organizational, product, etc, changes, and; beginning to introduce some of their own changes.

Truth be told, management teams that drive companies to truly excellent, consistently superior performances, are pretty rare. Whomever comes after them, like Paul Otellini at Intel, faces are daunting, and, essentially, more difficult task.

In time, the company begins to fill with lesser-talented management, its performance coasting to 'good,' from 'consistently superior.' The focus on prior methods and successes makes it hard for a less-talented group to recapture the successes of an early management generation.

If the company is lucky, another group will rise and repeat the earlier fundamental business practices that, once again, restore manufacturing, production, and/or service delivery to more productive levels, while introducing more relevant new products and services.

In short, it seems that, in large companies, there is simply a lack of discipline, over time, of management to value and retain a focus on 'purposeful change' of the company and its practices. It's as if nobody watches the measurements of performance which might signal that it's time for the company to innovate and change once again.

So, in a sense, Ford is no different, I suppose, than the average US company. And that's both a pity, and, I think, my point. The WSJ piece merely confirms that Ford is a normal US large-cap manufacturer that loses its way more often than it finds it.

Trouble is, today, it may have much less time and financial leeway to recover one more time.

I have to say, I was unimpressed with what it portends for the giant auto maker.

To distill the well-written article to its essence, the Brazilian unit of Ford has scored major gains with a new SUV model by doing two things: sensibly restructuring the physical manner in which they produce the car, and doing intensive consumer market research to design a car which the relevant market segment will buy, at a profitable (to Ford) price.

The good news, of course, is that some people at Ford down in Brazil, led by one Luc de Ferran, pulled this off. It's inspirational, and certainly better, as the saying goes, "than a sharp stick in the eye."

However, the bad news is that this "turnaround" at Ford Brazil is nothing fancy. Basically, the unit had fallen on extremely bad times, and simply rediscovered what, I believe, intelligent business people everywhere would acknowledge are obvious maxims.

They redesigned manufacturing to adapt to current realities, thus cutting wasted time and expense. They returned to classic marketing in the design of a new vehicle, using consumer research to uncover wants and needs, the incorporation of which, in the new Ecosport SUV, caused the car to gain an 80% market share.

This anecdote brings me to recall some of my prior posts regarding mediocrity and ineptitude in the general business environment. Specifically, this post about UAL, this one about Starbucks, and this one about Intel v. AMD.

Why is that Ford's Brazilian unit, or, for that matter, Ford itself, globally, must have its back to the wall in order to rediscover basic business sensibilities?

I suspect that the reason boils down to one word- discipline.

In a process which parallels Aristotle's thoughts on the decline of governmental systems from the pinnacle, the 'philosopher-kin' phase, I think corporate leadership/management undergoes something very similar.

When a company is "on top," competitively and in terms of consistently delivering superior total returns for shareholders, a sense of complacency begins to set in. The questioning, innovative behaviors which probably drove the company's success, begin to be institutionalized by a second tier of acolytes as 'revered processes.' The originators of the initial success move on- retirement of the lauded CEO, perhaps a few SVPs move to head other companies. Too, some of the wizards of the successful change are promoted, focus upward, and leave the nuts and bolts continuation of the success to less-capable subordinates. The new generation of leaders begin to do two things: view the changes wrought by the earlier successful managers as 'codes to live by,' missing the fundamental value of the changes having led to success, not the particular endpoint of the organizational, product, etc, changes, and; beginning to introduce some of their own changes.

Truth be told, management teams that drive companies to truly excellent, consistently superior performances, are pretty rare. Whomever comes after them, like Paul Otellini at Intel, faces are daunting, and, essentially, more difficult task.

In time, the company begins to fill with lesser-talented management, its performance coasting to 'good,' from 'consistently superior.' The focus on prior methods and successes makes it hard for a less-talented group to recapture the successes of an early management generation.

If the company is lucky, another group will rise and repeat the earlier fundamental business practices that, once again, restore manufacturing, production, and/or service delivery to more productive levels, while introducing more relevant new products and services.

In short, it seems that, in large companies, there is simply a lack of discipline, over time, of management to value and retain a focus on 'purposeful change' of the company and its practices. It's as if nobody watches the measurements of performance which might signal that it's time for the company to innovate and change once again.

So, in a sense, Ford is no different, I suppose, than the average US company. And that's both a pity, and, I think, my point. The WSJ piece merely confirms that Ford is a normal US large-cap manufacturer that loses its way more often than it finds it.

Trouble is, today, it may have much less time and financial leeway to recover one more time.

Subscribe to:

Posts (Atom)