There's a new financial investment program on CNBC in the evenings now. Its host is Dylan Ratigan, one of the network's on-air anchors. He has a BA in political economy from Union College.

The program is called "Fast Money," and features Ratigan with four guest pundits who opine on stocks at a furious pace. Their promo picture has them standing together, sans jackets, arms folded, looking "tough." This is serious business. The show's slogan is, "Game On!"

There are two things which confuse me about this new program. First, does it not cover the same ground as CNBC's "Mad Money" with Jim Cramer? Second, in contrast to the networks gushing tributes to Lou Rukeyser upon his passing, does this show not emphasize exactly what the esteemed late financial program host constantly warned viewers against, e.g., 'short-termism?'

Since CNBC is a cable-TV network, I understand that Fast Money is supposed to have entertainment value. It looks like something a producer pitched to the CNBC brass as "Cramer's Mad Money meets Crossfire." Four guys arguing about how fast to pump and dump various name stocks, with Ratigan mugging for the camera, being jocular with his 4 buddies and directing the action on camera. I've caught some of the show, and it pointedly focuses on, well, "fast money," i.e., how to rapidly churn trades to make instant cash.

In fact, my clearest recollection of Ratigan, whether interviewing Cramer at 3:30PM each day for the "Stop Trading" segment, or on Fast money, is him uttering a phrases such as,

"Jimmy, what's your best trade right now," or, "So what's the trade here?"

Maybe CNBC is worried that Cramer, like all entertainers, eventually wear out his welcome with his viewers. In that event, they have a look-alike ready to slip into that slot and retain ad dollars. Or perhaps they think Cramer will simply blow up on camera one day, and want to hedge their bets. Or maybe that he'll finally go too far one day, and find himself subpoenaed by the SEC.

On the second point, though, I really am puzzled. If I'm not mistaken, Rukeyser had chosen, or allowed to be chosen, Ratigan to guest host Wall Street Week in its last days, as Lou became too ill to go on air. WSW's hallmark was patient, longterm investing, under the careful, calm guidance of its well-regarded host.

What happened all of a sudden to this investing ethic? Has CNBC gone "mad?"

Perhaps the network saw the same data in the media lately that I have, regarding the nearly-50% volume of daily trading that hedge funds now comprise. Since they certainly don't have 50% of the market's assets yet, this means they must be turning over positions at a furious rate.

Is it possible CNBC figures that what's good enough for hedge funds is good enough for its viewers?

Friday, August 04, 2006

Richard Moore's 15 Minutes of Fame

Yesterday morning, CNBC's guest host was Richard Moore, Treasurer of the State of North Carolina.

I'm not really sure what the financial officer of a non-profit entity has to offer viewers of the network. Perhaps he is one of those aggressive, 'proactive' State Treasurers who feel they must assume the role of Chief Market and Investment Guru for their state. But he did provide some interesting information from an investor standpoint.

For instance, he referred many times to the portfolio he manages for the State, and some of its larger holdings. One was either Wal-Mart or some other retailer-ish company which has been in a slump for several years. Moore cheerily assured the CNBC on-air staff that the company in question was 'a fine company, we're not worried, they'll do just fine over time. We're long term investors.' Things like that.

His next pronouncement really took me by surprise. Asked about Microsoft, one of his portfolio's major equity holding, he professed complete faith in keeping the position for the next several years. When asked why, he rambled on in the following sort of vein,

'Well, it's just a great company. It's been down for a while, but it's great. It will be back. They have that X-box, and it's great. My kids tell me they love it, so don't count Microsoft out. They'll do fine, and we're a long term investor."

My own view, based upon my proprietary research and portfolio history, is decidedly different. I wrote here about how no technology companies have ever reappeared, years apart, among my selections, as of the date of the November, 2005 post. Since then, Apple has reappeared in the portfolio, after an absence of more than 10 years. However, it's arguably not the "same" Apple at all. And the reason it is back is not computers, but special-purpose, application-specific digital processing hardware and software combinations, a/k/a, "iPods."

However, for all other technology companies to date, the rule seems to be that their deep commitment to their original technologies prohibits them from taking advantage of opportunities spawned by the very success of those technologies. They learn to work 'one way,' with one legacy technology orientation, and pretty much die with it. If Microsoft has any second act whatsoever, and I doubt that it does, it will be reinventing itself as a niche hardware vendor, rather than a resurgent software titan. Its 'software in a box' approach is dead, Ballmer is still in charge, and the company's arguably too big to be sufficiently nimble now. In fact, on this last point, see yesterday's piece about GE.

So here we have the Treasurer of what I would guess to be a multi-billion dollar portfolio, making stock picks on the advice of his pre-teen children. I'm sure Tarheels throughout the state will be thrilled.

So much for Mr. Moore's 15 minutes of fame.

As for me, I'm actually pretty happy. If this is the competition in the marketplace of investors, I'm sleeping more easily tonight.

I'm not really sure what the financial officer of a non-profit entity has to offer viewers of the network. Perhaps he is one of those aggressive, 'proactive' State Treasurers who feel they must assume the role of Chief Market and Investment Guru for their state. But he did provide some interesting information from an investor standpoint.

For instance, he referred many times to the portfolio he manages for the State, and some of its larger holdings. One was either Wal-Mart or some other retailer-ish company which has been in a slump for several years. Moore cheerily assured the CNBC on-air staff that the company in question was 'a fine company, we're not worried, they'll do just fine over time. We're long term investors.' Things like that.

His next pronouncement really took me by surprise. Asked about Microsoft, one of his portfolio's major equity holding, he professed complete faith in keeping the position for the next several years. When asked why, he rambled on in the following sort of vein,

'Well, it's just a great company. It's been down for a while, but it's great. It will be back. They have that X-box, and it's great. My kids tell me they love it, so don't count Microsoft out. They'll do fine, and we're a long term investor."

My own view, based upon my proprietary research and portfolio history, is decidedly different. I wrote here about how no technology companies have ever reappeared, years apart, among my selections, as of the date of the November, 2005 post. Since then, Apple has reappeared in the portfolio, after an absence of more than 10 years. However, it's arguably not the "same" Apple at all. And the reason it is back is not computers, but special-purpose, application-specific digital processing hardware and software combinations, a/k/a, "iPods."

However, for all other technology companies to date, the rule seems to be that their deep commitment to their original technologies prohibits them from taking advantage of opportunities spawned by the very success of those technologies. They learn to work 'one way,' with one legacy technology orientation, and pretty much die with it. If Microsoft has any second act whatsoever, and I doubt that it does, it will be reinventing itself as a niche hardware vendor, rather than a resurgent software titan. Its 'software in a box' approach is dead, Ballmer is still in charge, and the company's arguably too big to be sufficiently nimble now. In fact, on this last point, see yesterday's piece about GE.

So here we have the Treasurer of what I would guess to be a multi-billion dollar portfolio, making stock picks on the advice of his pre-teen children. I'm sure Tarheels throughout the state will be thrilled.

So much for Mr. Moore's 15 minutes of fame.

As for me, I'm actually pretty happy. If this is the competition in the marketplace of investors, I'm sleeping more easily tonight.

Thursday, August 03, 2006

Another Thought on Longshoremen

I was discussing my longshoremen's post with my business partner over lunch yesterday. Having just published it, I didn't want to go back and alter it.

However, this thought occurred to me as we chatted about my analysis of the situation involving US unionized ports, shipping lines, and the two large longshoremen's unions.

These unions, together, have about 100,000 members, according to the WSJ piece. I just checked the Yahoo profiles on Ford and GM. They have a combined total workforce of about 630,000. Figure roughly 600,000 are UAW members. Gross that up 50% for related workers at other auto producers, or parts manufacturers, like Delphi (184,000 employees). That's about 900,000 members, or between 9x the size of the longshoremen's unions.

My point is, the longshoremen are hardly the sort of "union" Samuel Gompers and Walter Reuther had in mind when they began organizing labor in the first half of the last century. The Teamsters and the UAW are still largely, legitimately, "blue" collar unions.

The longshoremen sound like they wear pastel polo shirts these days, with khakis, and maybe topsiders. Sort of like a private version of PATCO, the air traffic controller's union with which Ronald Reagen so effectively dealt in the 1980s.

As I reflect on yesterday's piece, and these numbers, I have to say, I don't really even consider the longshoremen a "union" in the classic sense. They just don't evoke hordes of minimum wage immigrants, clamoring to get "better conditions" or "more jobs." Heck, these guys don't care how many jobs get displaced, so long as they are paid for theirs. Talk about pulling up the ladder!

If anything, I'd consider the dockworkers of today a sort of min-professional association. More like an engineering, medical society or the attorney's bar than the classical union of old. Their intelligent outmaneuvering of the management of US ports and global shipping lines suggests that, though they may call themselves a union, they behave like one of the better-organized "businesses" I think I've observed.

However, this thought occurred to me as we chatted about my analysis of the situation involving US unionized ports, shipping lines, and the two large longshoremen's unions.

These unions, together, have about 100,000 members, according to the WSJ piece. I just checked the Yahoo profiles on Ford and GM. They have a combined total workforce of about 630,000. Figure roughly 600,000 are UAW members. Gross that up 50% for related workers at other auto producers, or parts manufacturers, like Delphi (184,000 employees). That's about 900,000 members, or between 9x the size of the longshoremen's unions.

My point is, the longshoremen are hardly the sort of "union" Samuel Gompers and Walter Reuther had in mind when they began organizing labor in the first half of the last century. The Teamsters and the UAW are still largely, legitimately, "blue" collar unions.

The longshoremen sound like they wear pastel polo shirts these days, with khakis, and maybe topsiders. Sort of like a private version of PATCO, the air traffic controller's union with which Ronald Reagen so effectively dealt in the 1980s.

As I reflect on yesterday's piece, and these numbers, I have to say, I don't really even consider the longshoremen a "union" in the classic sense. They just don't evoke hordes of minimum wage immigrants, clamoring to get "better conditions" or "more jobs." Heck, these guys don't care how many jobs get displaced, so long as they are paid for theirs. Talk about pulling up the ladder!

If anything, I'd consider the dockworkers of today a sort of min-professional association. More like an engineering, medical society or the attorney's bar than the classical union of old. Their intelligent outmaneuvering of the management of US ports and global shipping lines suggests that, though they may call themselves a union, they behave like one of the better-organized "businesses" I think I've observed.

GE : Sized to Perform for Investors?

Since my various posts on GE, Jeff Immelt and Jack Welch, I've been musing about why the company performs as it does. Which is to say, poorly.

I'm not a balance sheet type of guy. Most of my analysis focuses on changes in income statement items, because I believe that the ultimate goal of CEOs, and investors, should be to earn consistently superior total returns with a company's assets. My proprietary research has found that changes in income statement items are most associated with changes in total returns, especially for growth companies.

However, I am aware that GE is among the largest, if not the largest, US public company by assets. It's certainly among the top 5, I would think.

In the company's recent annual report, which you may find on the GE website, Immelt, the CEO, claims, in a bold headline, that GE is "sized to perform for investors."

Really?

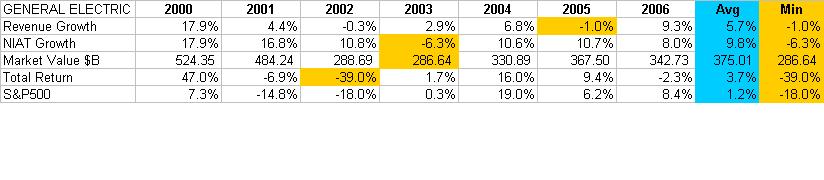

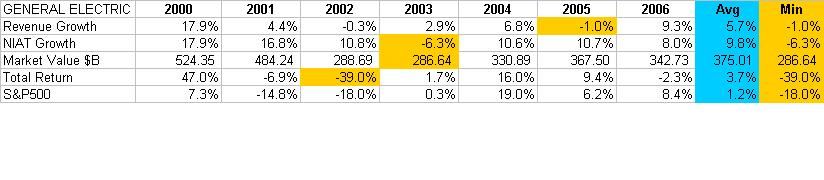

Here's a table of GE's recent "performance," in terms of growth in revenues and NIAT, market value, and total return for its investors (click on the table to see an enlarged version) from July of 2000 to July of 2006. The S&P500 Index annual return is included for comparison purposes. The blue column provides the average for the last seven years, while the tan column and cells display the minimum values over the seven year period.

Here's a table of GE's recent "performance," in terms of growth in revenues and NIAT, market value, and total return for its investors (click on the table to see an enlarged version) from July of 2000 to July of 2006. The S&P500 Index annual return is included for comparison purposes. The blue column provides the average for the last seven years, while the tan column and cells display the minimum values over the seven year period.

As I look at this table, what jumps out at me is how mediocre GE has been. Its sales growth is an S&P ballpark average of roughly 6%. NIAT growth is a bit higher, so that means management is squeezing profits out of the slow-growing company, to get the 10% average on that measure. Average total return is an anemic 3.7% over the period. Better than the 1.2% average for the S&P, but with 3 negative years, including one in which return plunged almost 40%. Immelt is responsible for the period 2002-2006, when the average total return of the company was -2.8%, compared to the S&P's +3.2%.

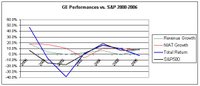

Here is some of the same data, in chart form (again, clicking on the chart will bring up a larger version). On balance, GE has been, for the last 7 12-month periods, an inconsistently mediocre company. The slim margin of 2.5 percentage points of outperformance over the S&P is hardly worth the risk entailed by holding the company's stock for 7 years.

Here is some of the same data, in chart form (again, clicking on the chart will bring up a larger version). On balance, GE has been, for the last 7 12-month periods, an inconsistently mediocre company. The slim margin of 2.5 percentage points of outperformance over the S&P is hardly worth the risk entailed by holding the company's stock for 7 years.

So, I ask again, for "what" exactly is GE "sized to perform for investors?" Certainly not returns.

No, I've come to the conclusion that GE is sized to provide highly compensated jobs for its senior managers, particularly Jeff Immelt.

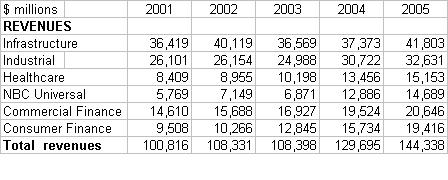

Consider this. The company now has a market value of roughly $350B. It is organized into six major business units, no one of which currently has revenues of less than $15B. Here is a table from the GE annual report providing the details (once again, click on it to enlarge). This is one huge company. And it's not all that lopsided. The largest major component, Infrastructure, has $41B in revenues, or less than 3x that of the smallest unit, NBC Universal.

Consider this. The company now has a market value of roughly $350B. It is organized into six major business units, no one of which currently has revenues of less than $15B. Here is a table from the GE annual report providing the details (once again, click on it to enlarge). This is one huge company. And it's not all that lopsided. The largest major component, Infrastructure, has $41B in revenues, or less than 3x that of the smallest unit, NBC Universal.

In this era of private equity buyouts and plentiful capital, why do these business units need to be under one corporate umbrella? It's hard to believe finance and adminstration functions require such scale. In fact, each unit probably has its own basic administration functions. And if the vaunted GE research labs are really key to every unit, they could jointly fund those labs and buy desired research results, patents, and inventions.

With such a mediocre track record for the better part of a decade, while compensating Immelt so richly, as I have discussed here, what possible defense is there for keeping this behemoth intact anymore?

The days of Thomas Edison's end-to-end electrical system supply enterprise are long, long gone. I contend that each of these business units, and perhaps even more, at lower levels, could be spun off independently, to GE's investors' benefit. It's hard to believe that this collection of such different businesses can realistically derive value from being in a common corporate domicile, let alone generate excess returns because of that common home to pay for the lush compensation of the various senior executives.

I can't see any downside to breaking up GE into its component businesses. Does anyone else?

I'm not a balance sheet type of guy. Most of my analysis focuses on changes in income statement items, because I believe that the ultimate goal of CEOs, and investors, should be to earn consistently superior total returns with a company's assets. My proprietary research has found that changes in income statement items are most associated with changes in total returns, especially for growth companies.

However, I am aware that GE is among the largest, if not the largest, US public company by assets. It's certainly among the top 5, I would think.

In the company's recent annual report, which you may find on the GE website, Immelt, the CEO, claims, in a bold headline, that GE is "sized to perform for investors."

Really?

Here's a table of GE's recent "performance," in terms of growth in revenues and NIAT, market value, and total return for its investors (click on the table to see an enlarged version) from July of 2000 to July of 2006. The S&P500 Index annual return is included for comparison purposes. The blue column provides the average for the last seven years, while the tan column and cells display the minimum values over the seven year period.

Here's a table of GE's recent "performance," in terms of growth in revenues and NIAT, market value, and total return for its investors (click on the table to see an enlarged version) from July of 2000 to July of 2006. The S&P500 Index annual return is included for comparison purposes. The blue column provides the average for the last seven years, while the tan column and cells display the minimum values over the seven year period.As I look at this table, what jumps out at me is how mediocre GE has been. Its sales growth is an S&P ballpark average of roughly 6%. NIAT growth is a bit higher, so that means management is squeezing profits out of the slow-growing company, to get the 10% average on that measure. Average total return is an anemic 3.7% over the period. Better than the 1.2% average for the S&P, but with 3 negative years, including one in which return plunged almost 40%. Immelt is responsible for the period 2002-2006, when the average total return of the company was -2.8%, compared to the S&P's +3.2%.

Here is some of the same data, in chart form (again, clicking on the chart will bring up a larger version). On balance, GE has been, for the last 7 12-month periods, an inconsistently mediocre company. The slim margin of 2.5 percentage points of outperformance over the S&P is hardly worth the risk entailed by holding the company's stock for 7 years.

Here is some of the same data, in chart form (again, clicking on the chart will bring up a larger version). On balance, GE has been, for the last 7 12-month periods, an inconsistently mediocre company. The slim margin of 2.5 percentage points of outperformance over the S&P is hardly worth the risk entailed by holding the company's stock for 7 years.So, I ask again, for "what" exactly is GE "sized to perform for investors?" Certainly not returns.

No, I've come to the conclusion that GE is sized to provide highly compensated jobs for its senior managers, particularly Jeff Immelt.

Consider this. The company now has a market value of roughly $350B. It is organized into six major business units, no one of which currently has revenues of less than $15B. Here is a table from the GE annual report providing the details (once again, click on it to enlarge). This is one huge company. And it's not all that lopsided. The largest major component, Infrastructure, has $41B in revenues, or less than 3x that of the smallest unit, NBC Universal.

Consider this. The company now has a market value of roughly $350B. It is organized into six major business units, no one of which currently has revenues of less than $15B. Here is a table from the GE annual report providing the details (once again, click on it to enlarge). This is one huge company. And it's not all that lopsided. The largest major component, Infrastructure, has $41B in revenues, or less than 3x that of the smallest unit, NBC Universal.In this era of private equity buyouts and plentiful capital, why do these business units need to be under one corporate umbrella? It's hard to believe finance and adminstration functions require such scale. In fact, each unit probably has its own basic administration functions. And if the vaunted GE research labs are really key to every unit, they could jointly fund those labs and buy desired research results, patents, and inventions.

With such a mediocre track record for the better part of a decade, while compensating Immelt so richly, as I have discussed here, what possible defense is there for keeping this behemoth intact anymore?

The days of Thomas Edison's end-to-end electrical system supply enterprise are long, long gone. I contend that each of these business units, and perhaps even more, at lower levels, could be spun off independently, to GE's investors' benefit. It's hard to believe that this collection of such different businesses can realistically derive value from being in a common corporate domicile, let alone generate excess returns because of that common home to pay for the lush compensation of the various senior executives.

I can't see any downside to breaking up GE into its component businesses. Does anyone else?

Wednesday, August 02, 2006

Ports, Shippers & Longshoremen: The Auto Industry & the UAW Redux?

Last Wednesday's Wall Street Journal carried a very informative article about the nation's longshoremen's unions.

According to the Journal's piece, there are 100,000 members of the two longshoremen's unions, with average annual compensation of $120,000. They are reputed to be the highest paid blue-collar workers in the country.

What struck me immediately about this union is how similar the country's shippers, ports, and other related business entities have dealt with the longshoremen's unions. Basically, it echoes how the once-Big 3 of the US auto industry, GM, Ford and Chrysler, handled the UAW. The WSJ piece describes how port management companies have agreed to pay longshoremen for containers they don't even touch, just because they come through a union port. In example after example, the unions exercised their power to extort...er....extract concessions from management that build costs into shipping and docking operations.

Technological improvements are allowed if the displaced longshoremen are paid as well, and the union workers given the jobs of operating the new equipment. Union ports won't handle goods from non-union ports, on penalty of the longshoremen simply refusing to unload the cargo. The West Coast's longshoremen's union pioneered the use of master agreements, whereby the shipping lines agree not to use non-union ports, in order to have union workers handle their ship's cargos in the valuable ports of California, Oregon and Washington.

At first, I thought that this might be highlighting a situation that could go the way of the automakers. Upon discussing this with my business partner, I was musing about whether, say, Mexico could create a parallel, non-union transportation system for goods. Perhaps upgrade a port on each of their coasts, link each by rail to the US, and proceed to undercut the American ports and, thus, longshoremen. Apparently, Wal-Mart and some other companies are using just such a fledgling operation already.

Apparently, the master operating agreements will preclude this gaining much ground. Such a parallel system would need its own fleet, and railroads as well. The entire operation would have to be replicated, from originating production point to end-user commercial site. Possible, but burdensome. Maybe a modest amount of production can move this way, but I wonder how much of the US total shipping by tonnage can go such a route within the existing port constraints.

What's similar in the longshoremen's unions case to the auto workers case is that the union has adroitly grabbed the choke points of its dependent business system, and created substantial value for its members.

What's different is that, unlike auto makers, who cannot prevent other companies from rendering their pacts with unions uncompetitive, there seems to be no alternative for anyone to using unionized ports and laborers for existing shipping and dockwork. Give these guys credit, the longshoremen's leaders seem to have sewn up every alternative to their control. The only way this would change is if the nascent efforts of a country like Mexico, mentioned in a prior paragraph, can build sufficient volume to threaten the competitiveness of the unionized port management company's profits, and, thus, the jobs of the union workers there.

So, perhaps the longshoremen more closely resemble the dairy and sugar farmers. They are relatively few in number, and thus gain substantially from the economically-indefensible tariffs they have created in the shipping and transport system. The real cost each of us 250+ million Americans pay, per item, is tiny, compared to the surplus wages the 100,000 longshoremen enjoy. Just like the few dairy and sugar producers, who split the various tariff revenues among a very few farmers. Who thinks sugar is overpriced in the US, despite the fact that it is at something like twice the world price?

At a 2500-to-1 US population to longshoremen ratio, each of us pays about $48/year to these union workers. That's why we probably won't see an industrial challenge to their monopolistic position astride the world's, and America's, logistics/supply chains. And since non-union ports can't be used, there's no real competition for Los Angeles or Seattle. Thus, the businesses aren't really incented to break ranks with the union, so to speak. Unlike foreign auto makers, who could, and did, enter the US and create disaster for GM, Ford and Chrysler, there's really nobody on the global scene who can effectively do that to ports in any country.

Here's the real eye-opener from the WSJ piece. It cited an anecdote of former white-collar managers successfully landing longshoremen's jobs in Charleston, SC. Could it be that your son or daughter should aspire to be come a longshoreman?

According to the Journal's piece, there are 100,000 members of the two longshoremen's unions, with average annual compensation of $120,000. They are reputed to be the highest paid blue-collar workers in the country.

What struck me immediately about this union is how similar the country's shippers, ports, and other related business entities have dealt with the longshoremen's unions. Basically, it echoes how the once-Big 3 of the US auto industry, GM, Ford and Chrysler, handled the UAW. The WSJ piece describes how port management companies have agreed to pay longshoremen for containers they don't even touch, just because they come through a union port. In example after example, the unions exercised their power to extort...er....extract concessions from management that build costs into shipping and docking operations.

Technological improvements are allowed if the displaced longshoremen are paid as well, and the union workers given the jobs of operating the new equipment. Union ports won't handle goods from non-union ports, on penalty of the longshoremen simply refusing to unload the cargo. The West Coast's longshoremen's union pioneered the use of master agreements, whereby the shipping lines agree not to use non-union ports, in order to have union workers handle their ship's cargos in the valuable ports of California, Oregon and Washington.

At first, I thought that this might be highlighting a situation that could go the way of the automakers. Upon discussing this with my business partner, I was musing about whether, say, Mexico could create a parallel, non-union transportation system for goods. Perhaps upgrade a port on each of their coasts, link each by rail to the US, and proceed to undercut the American ports and, thus, longshoremen. Apparently, Wal-Mart and some other companies are using just such a fledgling operation already.

Apparently, the master operating agreements will preclude this gaining much ground. Such a parallel system would need its own fleet, and railroads as well. The entire operation would have to be replicated, from originating production point to end-user commercial site. Possible, but burdensome. Maybe a modest amount of production can move this way, but I wonder how much of the US total shipping by tonnage can go such a route within the existing port constraints.

What's similar in the longshoremen's unions case to the auto workers case is that the union has adroitly grabbed the choke points of its dependent business system, and created substantial value for its members.

What's different is that, unlike auto makers, who cannot prevent other companies from rendering their pacts with unions uncompetitive, there seems to be no alternative for anyone to using unionized ports and laborers for existing shipping and dockwork. Give these guys credit, the longshoremen's leaders seem to have sewn up every alternative to their control. The only way this would change is if the nascent efforts of a country like Mexico, mentioned in a prior paragraph, can build sufficient volume to threaten the competitiveness of the unionized port management company's profits, and, thus, the jobs of the union workers there.

So, perhaps the longshoremen more closely resemble the dairy and sugar farmers. They are relatively few in number, and thus gain substantially from the economically-indefensible tariffs they have created in the shipping and transport system. The real cost each of us 250+ million Americans pay, per item, is tiny, compared to the surplus wages the 100,000 longshoremen enjoy. Just like the few dairy and sugar producers, who split the various tariff revenues among a very few farmers. Who thinks sugar is overpriced in the US, despite the fact that it is at something like twice the world price?

At a 2500-to-1 US population to longshoremen ratio, each of us pays about $48/year to these union workers. That's why we probably won't see an industrial challenge to their monopolistic position astride the world's, and America's, logistics/supply chains. And since non-union ports can't be used, there's no real competition for Los Angeles or Seattle. Thus, the businesses aren't really incented to break ranks with the union, so to speak. Unlike foreign auto makers, who could, and did, enter the US and create disaster for GM, Ford and Chrysler, there's really nobody on the global scene who can effectively do that to ports in any country.

Here's the real eye-opener from the WSJ piece. It cited an anecdote of former white-collar managers successfully landing longshoremen's jobs in Charleston, SC. Could it be that your son or daughter should aspire to be come a longshoreman?

Tuesday, August 01, 2006

Private Equity Buyouts: The Fairness Question

A few months ago, I wrote a post about private equity buyouts, triggered by the Kinder Morgan deal.

In that post, I discussed the larger trend of private equity buyouts as they may effect the larger pool of equities, the S&P500 Index, and, lastly, my equity portfolio strategy.

Last week, my partner and I were discussing this phenomenon again, as HCA is being taken private. And, further, a flurry of Wall Street Journal articles have focused on this trend, plus the trend of hedge funds to turn to private equity as a tool for asset allocation.

Whereas in my prior post, I deliberately chose to omit any discussion of the ethics of buyouts, and the multiple roles of investment banks, plus the question of fees charged to the buyouts. In this post, I will comment on those aspects of modern private equity buyouts.

First, it does seem, frankly, grossly unfair that a small group of managers of a firm like HCA, or Kinder Morgan, who clearly know more about the future prospects of a company than the average shareholder, would tender to take out those other owners at a price which, by definition, has to be below that felt to be attainable by the internal management leading the buyout.

It is inconceivable that a veteran management group would get into bed with a private equity group or a hedge fund, and then offer the remaining (soon to be ex-) shareholders a "fair" price for the latter's interest in the firm.

If there were ever to be legislation to clean up this ethical loophole, my partner and I reasoned something like the following would work. A sort of reverse greenmail. If a management tendered to take the firm private, regulation should provide for the offering of a similar ownership share in the newly-private firm, without voting rights, but with equity rights equal to that of the management's holdings. In effect, whatever management deals itself in for would be available to any shareholders who wished to stay on board for the ride. It would be interesting to see how such a change in the law to mitigate gross underpayment to existing shareholders by the buyout group would affect future private equity deals.

Another popular recent topic regarding private equity buyouts is the weight and number of fees connected with the deals which are ultimately charged back to the company being taken private. Add to this the multiple roles of some investment banks- advisor, participant, and perhaps even competitor to finance the deal- and you have another ethical mess.

I had to laugh recently when John Mack, CEO of Morgan Stanley, deadpanned that there would be 'some potential conflicts' as he planned to move his firm heavily into financing and participating in the private equity business in order to sustain and increase fee revenues at his firm.

The Journal ran a long piece on July 25th, providing some examples of he egregious fees with which the target companies are saddled during and after a buyout. Cash is looted to repay legal and financing fees, plus generous dividends, "just because." Now, mind you, as the new owners, the buyout firm and management team are perfectly within their rights to do this. However, one has to wonder, for a firm such as Burger King, if the company will have much of a chance of ever becoming a consistently superior total return company, post-IPO, when it has to incur all these questionable, largely non-economic costs on behalf of the short-term buyout owners.

I don't have information pertaining to this question, but I wonder how many private buyouts of size, when taken public again via IPOs, become reasonably attractive on the basis of total returns. It could well be that, my earlier legislative suggestion notwithstanding, prior shareholders are actually better off to take the cash and run before the buyout. Unless, of course, their receipts of the many rich fee and cash streams, as part of the new ownership class, make up for post-IPO weakness in the company's share price and returns.

Adding hedge funds to this mix seems to be like pouring gasoline on a fire. These guys are even shorter-term oriented than the buyout firms and their accomplices, the target firms' managements. One can just imagine the kind of explosions that could result from letting money managers who are essentially day-traders, self-privatized from Wall Street banks, play around with private equity buyouts lasting even as little as 18-24 months.

As my partner and I discussed these various aspects of the newly-popular private equity buyout trend, we reminded ourselves that our equity strategy will be largely unaffected. Managers take firms private when they feel that their company's stock price is 'getting no respect.' That doesn't typically describe our selections. So, fortunately, we will be watching this circus continue from the sidelines.

In that post, I discussed the larger trend of private equity buyouts as they may effect the larger pool of equities, the S&P500 Index, and, lastly, my equity portfolio strategy.

Last week, my partner and I were discussing this phenomenon again, as HCA is being taken private. And, further, a flurry of Wall Street Journal articles have focused on this trend, plus the trend of hedge funds to turn to private equity as a tool for asset allocation.

Whereas in my prior post, I deliberately chose to omit any discussion of the ethics of buyouts, and the multiple roles of investment banks, plus the question of fees charged to the buyouts. In this post, I will comment on those aspects of modern private equity buyouts.

First, it does seem, frankly, grossly unfair that a small group of managers of a firm like HCA, or Kinder Morgan, who clearly know more about the future prospects of a company than the average shareholder, would tender to take out those other owners at a price which, by definition, has to be below that felt to be attainable by the internal management leading the buyout.

It is inconceivable that a veteran management group would get into bed with a private equity group or a hedge fund, and then offer the remaining (soon to be ex-) shareholders a "fair" price for the latter's interest in the firm.

If there were ever to be legislation to clean up this ethical loophole, my partner and I reasoned something like the following would work. A sort of reverse greenmail. If a management tendered to take the firm private, regulation should provide for the offering of a similar ownership share in the newly-private firm, without voting rights, but with equity rights equal to that of the management's holdings. In effect, whatever management deals itself in for would be available to any shareholders who wished to stay on board for the ride. It would be interesting to see how such a change in the law to mitigate gross underpayment to existing shareholders by the buyout group would affect future private equity deals.

Another popular recent topic regarding private equity buyouts is the weight and number of fees connected with the deals which are ultimately charged back to the company being taken private. Add to this the multiple roles of some investment banks- advisor, participant, and perhaps even competitor to finance the deal- and you have another ethical mess.

I had to laugh recently when John Mack, CEO of Morgan Stanley, deadpanned that there would be 'some potential conflicts' as he planned to move his firm heavily into financing and participating in the private equity business in order to sustain and increase fee revenues at his firm.

The Journal ran a long piece on July 25th, providing some examples of he egregious fees with which the target companies are saddled during and after a buyout. Cash is looted to repay legal and financing fees, plus generous dividends, "just because." Now, mind you, as the new owners, the buyout firm and management team are perfectly within their rights to do this. However, one has to wonder, for a firm such as Burger King, if the company will have much of a chance of ever becoming a consistently superior total return company, post-IPO, when it has to incur all these questionable, largely non-economic costs on behalf of the short-term buyout owners.

I don't have information pertaining to this question, but I wonder how many private buyouts of size, when taken public again via IPOs, become reasonably attractive on the basis of total returns. It could well be that, my earlier legislative suggestion notwithstanding, prior shareholders are actually better off to take the cash and run before the buyout. Unless, of course, their receipts of the many rich fee and cash streams, as part of the new ownership class, make up for post-IPO weakness in the company's share price and returns.

Adding hedge funds to this mix seems to be like pouring gasoline on a fire. These guys are even shorter-term oriented than the buyout firms and their accomplices, the target firms' managements. One can just imagine the kind of explosions that could result from letting money managers who are essentially day-traders, self-privatized from Wall Street banks, play around with private equity buyouts lasting even as little as 18-24 months.

As my partner and I discussed these various aspects of the newly-popular private equity buyout trend, we reminded ourselves that our equity strategy will be largely unaffected. Managers take firms private when they feel that their company's stock price is 'getting no respect.' That doesn't typically describe our selections. So, fortunately, we will be watching this circus continue from the sidelines.

Searching for Patterns in Financial Information: Part 2

Recently, I discussed the similarities between entropy theory, information theory, and efficient markets theory. Essentially, my equity portfolio strategy is a pattern-seeking machine for use in financial markets.

Because all three phenomena make use of distributions, the concept of uncertainty applies to all of them.

In entropy, uncertainty is seen as the non-uniform distribution of, say, gas molecules in a container. Due to randomly differing energy levels, a gas tends not to be evenly distributed. Physicists came to the conclusion that the use of probabilistic distributions was necessary to accurately to make predictions of the behavior of gases in a container.

Similarly, Shannon's information theory deals with uncertainty. Until one can find sufficient symbol redundancy to ascertain "information" amidst a series of symbols, uncertainty is high. Finding the signal amidst the noise uses probabilistic distributions to ascertain likelihoods of information content, and what that content is.

In the same way, our equity portfolio selection and management process seeks out patterns amidst the noise of financial data. Taken on its face, this torrent of financial information, both market (technical), and company-specific (fundamental), is full of uncertainty. Especially over short periods of time, such as hours or days, the data may seem to contain little in the way of useful patterns. Indeed, in today's markets, with hedge funds accounting for up to 50% of the trading volume on many days, it would seem that rapid-fire trading and asset turnover preclude the search by most investors for patterns beyond a few days in duration.

On the contrary, we carefully sift through a variety of longer-term data which proprietary research has shown contains redundancy. That is, we have found that, when certain predictor data are of a certain pattern, then dependent variables, such as total return, have a high probability of also fitting a certain pattern. This redundancy, while not perfect, seems to provide for a significant amount of probability that the "tails" of distributions of certain data will contain desired information.

While much portfolio management and equity analysis seems to focus on point-estimates of prices and earnings, we prefer to make use of probabilistic distributions of key data in order to increase the chances that the equities we choose will continue to behave in a virtuous pattern, pursuant to our research findings.

As I discussed in my earlier post, the fact that tickers represent real companies, full of real people producing real products and services, increases our confidence that the patterns we seek, and find, are reliable and profitable. Borrowing from the probabilistic approaches to pattern discovery and uncertainty reduction in entropy and information theories, we believe we have developed something as powerful and functional in the management of equity portfolios in finance.

Because all three phenomena make use of distributions, the concept of uncertainty applies to all of them.

In entropy, uncertainty is seen as the non-uniform distribution of, say, gas molecules in a container. Due to randomly differing energy levels, a gas tends not to be evenly distributed. Physicists came to the conclusion that the use of probabilistic distributions was necessary to accurately to make predictions of the behavior of gases in a container.

Similarly, Shannon's information theory deals with uncertainty. Until one can find sufficient symbol redundancy to ascertain "information" amidst a series of symbols, uncertainty is high. Finding the signal amidst the noise uses probabilistic distributions to ascertain likelihoods of information content, and what that content is.

In the same way, our equity portfolio selection and management process seeks out patterns amidst the noise of financial data. Taken on its face, this torrent of financial information, both market (technical), and company-specific (fundamental), is full of uncertainty. Especially over short periods of time, such as hours or days, the data may seem to contain little in the way of useful patterns. Indeed, in today's markets, with hedge funds accounting for up to 50% of the trading volume on many days, it would seem that rapid-fire trading and asset turnover preclude the search by most investors for patterns beyond a few days in duration.

On the contrary, we carefully sift through a variety of longer-term data which proprietary research has shown contains redundancy. That is, we have found that, when certain predictor data are of a certain pattern, then dependent variables, such as total return, have a high probability of also fitting a certain pattern. This redundancy, while not perfect, seems to provide for a significant amount of probability that the "tails" of distributions of certain data will contain desired information.

While much portfolio management and equity analysis seems to focus on point-estimates of prices and earnings, we prefer to make use of probabilistic distributions of key data in order to increase the chances that the equities we choose will continue to behave in a virtuous pattern, pursuant to our research findings.

As I discussed in my earlier post, the fact that tickers represent real companies, full of real people producing real products and services, increases our confidence that the patterns we seek, and find, are reliable and profitable. Borrowing from the probabilistic approaches to pattern discovery and uncertainty reduction in entropy and information theories, we believe we have developed something as powerful and functional in the management of equity portfolios in finance.

Monday, July 31, 2006

Comcast's Big Internet Video Bet

There have been several pieces in the last month or so in the Wall Street Journal concerning Big Media's attempts to grapple with video on the internet.

Will consumers figure out how to watch video, even television programming, while bypassing broadcast and cable networks? Will it be possible, with the aid of boxes supplied by a number of companies said to be developing them, including Apple, to surf the web for content to play over your television, without resorting to using your cable television signal? In effect, finally treating your television as a giant monitor, having a web-enabled remote control, and accessing, say, producers' websites to buy serial program content, or movie libraries, directly?

Comcast sure hopes not. They have been busy trying to collect and organize a group of licenses, in order to provide 'direct' access to web content through their network. In other words, providing a sort of intermediated web-access, to stop their customers from terminating the entire cable television data, and revenue, stream.

Will it work?

When I first read the Journal's piece in late June, I thought Comcast might have a chance. It's expensive, and risky, but what choice do they have? I like seeing businesses at least go for the big strategic advantage, provided there's a reasonable chance of success, based upon consumer behavior and technical or other relevant factors.

Lately, though, I'm thinking differently. The WSJ's digital report a few weeks ago featured a long piece consisting of an interview with Disney's Bob Iger. In it, Iger casually mentioned licensing content to anyone Disney thinks will help them get more reach and revenue. He mentioned Comcast- but clearly as a non-exclusive license. This was a valuable tidbit, in my opinion.

Now, it seems, Comcast is probably collecting a variety of mismatched, non-homogeneous content licenses, some or many of them non-exclusive. This means that they will be in no position to actually stop customers from accessing content elsewhere. Comcast just hopes it will be easy enough to do it "their way," for their monthly television cable fee, to prevent most of their customer base from dropping half of their Comcast service and going surfing for the rest via high-speed digital broadband.

It should be very interesting to see how this plays out. On one hand, I can see plenty of customers taking a semi-packaged solution to this situation. On the other hand, I could also see plenty of early-adopters doing otherwise, being as this is a 'technology' product to begin with. That is, it's not like buying or using something rather mundane, like, say, a washing machine, an iron, or your toaster.

No, this is "technology" coming hard and fast into Comcast's customers' living rooms. We'll soon see if their stop-gap solution to stem their customer base from going surfing directly onto the web for video content works. Or if it proves to be their last-ditch, expensive rear-guard action as they sink into oblivion, along with once-mighty forces like your old telephone land-line provider.

Will consumers figure out how to watch video, even television programming, while bypassing broadcast and cable networks? Will it be possible, with the aid of boxes supplied by a number of companies said to be developing them, including Apple, to surf the web for content to play over your television, without resorting to using your cable television signal? In effect, finally treating your television as a giant monitor, having a web-enabled remote control, and accessing, say, producers' websites to buy serial program content, or movie libraries, directly?

Comcast sure hopes not. They have been busy trying to collect and organize a group of licenses, in order to provide 'direct' access to web content through their network. In other words, providing a sort of intermediated web-access, to stop their customers from terminating the entire cable television data, and revenue, stream.

Will it work?

When I first read the Journal's piece in late June, I thought Comcast might have a chance. It's expensive, and risky, but what choice do they have? I like seeing businesses at least go for the big strategic advantage, provided there's a reasonable chance of success, based upon consumer behavior and technical or other relevant factors.

Lately, though, I'm thinking differently. The WSJ's digital report a few weeks ago featured a long piece consisting of an interview with Disney's Bob Iger. In it, Iger casually mentioned licensing content to anyone Disney thinks will help them get more reach and revenue. He mentioned Comcast- but clearly as a non-exclusive license. This was a valuable tidbit, in my opinion.

Now, it seems, Comcast is probably collecting a variety of mismatched, non-homogeneous content licenses, some or many of them non-exclusive. This means that they will be in no position to actually stop customers from accessing content elsewhere. Comcast just hopes it will be easy enough to do it "their way," for their monthly television cable fee, to prevent most of their customer base from dropping half of their Comcast service and going surfing for the rest via high-speed digital broadband.

It should be very interesting to see how this plays out. On one hand, I can see plenty of customers taking a semi-packaged solution to this situation. On the other hand, I could also see plenty of early-adopters doing otherwise, being as this is a 'technology' product to begin with. That is, it's not like buying or using something rather mundane, like, say, a washing machine, an iron, or your toaster.

No, this is "technology" coming hard and fast into Comcast's customers' living rooms. We'll soon see if their stop-gap solution to stem their customer base from going surfing directly onto the web for video content works. Or if it proves to be their last-ditch, expensive rear-guard action as they sink into oblivion, along with once-mighty forces like your old telephone land-line provider.

Proctor & Gamble: Poised for Sustained Growth?

I mentioned in a recent post that I read an interview with James Stengel, chief marketing officer of Proctor & Gamble. His focus on customer problems, lifestyles, and how P&G can improve their customers' lives was quite impressive.

In discussing this with my business partner, I mused about whether P&G may be, for the first time, heading toward inclusion in our equity portfolio of consistently superior companies. After all, with a clear-headed, viable focus on consumers, and customer needs, one might think that the firm is within reach of becoming a really well-led, well-managed creator of shareholder returns, based upon solid business concepts and executions leading to consistently superior revenue growth.

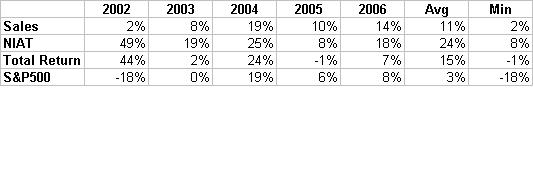

To get a better understanding of this, I did some analysis of the company's recent sales, NIAT, and total returns. They are presented in the table at left, on which you may click to enlarge.

To get a better understanding of this, I did some analysis of the company's recent sales, NIAT, and total returns. They are presented in the table at left, on which you may click to enlarge.

The first thing I notice is that P&G's sales accelerated in 2004 and this year. A friend who works at the firm, locally, confirmed that these are the effects of the last two major acquisitions. The latter one being Gillette, last year.

This has an interesting effect on P&G, called "riding the tiger." Notice that its sales growth rates, pre-acquisitions, were in the single digits, on the low side, on average. In the years prior to 2002, they were also rather meager. Thus, P&G has bought growth, twice. The year in between the acquisitions displays a 10% sales growth- higher than the earlier years, but still not so high as with the immediate folding-in of the purchased sales bases.

My proprietary research shows that the market tends to favor companies which can consistently generate superior revenue growth. P&G has begun to buy its growth. Either of two things need to occur, if the company is to have a good chance of becoming a consistently superior total return-generating company.

Either it needs to generate organic growth to match that of the effects of the acquisitions, or it needs to be able to continue its acquisition program, making it a sort of 'standard operating procedure," for which investors are prepared to pay. The company is hitting some pretty high revenue growth targets for a consumer goods conglomerate. While the 10% revenue growth in 2005 was good, and better than the long-term S&P average, it was by no means near the upper end of the distribution of revenue growth in the S&P500.

NIAT growth at P&G has also been getting better, but the best years were in the earlier years of this period.

Taken together, the revenue and NIAT growth pictures lead to the total return performance shown in the table. P&G has a much better average than the S&P for the last five years. However, the last two years have been a close call. Most of the 12 point spread in average total return between the S&P and P&G is accounted for by 2002. I would guess that would have been from a "flight to quality" by investors, as the tech-bubble-bursting recession drove investors to safer havens. Too, the low returns in 2004 and 2006 could be the result of investor verdicts on the prices of each of the two major acquisitions in the the prior two years.

I like P&G's customer focus. I understand the broadening of their product and business portfolios recently. However, from the data above, I seriously wonder if they can sustain raw revenue growth in the next few years. This is where consistency of revenue growth at fairly high rates really challenges a company. If too much of the firm's recent success on this dimension was simply purchasing growth, then I think total returns will ebb, along with organic growth.

It will be very interesting to watch P&G in the next few years to see how their fundamental operating capabilities prove out, and whether the market rewards the firm, if they do.

In discussing this with my business partner, I mused about whether P&G may be, for the first time, heading toward inclusion in our equity portfolio of consistently superior companies. After all, with a clear-headed, viable focus on consumers, and customer needs, one might think that the firm is within reach of becoming a really well-led, well-managed creator of shareholder returns, based upon solid business concepts and executions leading to consistently superior revenue growth.

To get a better understanding of this, I did some analysis of the company's recent sales, NIAT, and total returns. They are presented in the table at left, on which you may click to enlarge.

To get a better understanding of this, I did some analysis of the company's recent sales, NIAT, and total returns. They are presented in the table at left, on which you may click to enlarge.The first thing I notice is that P&G's sales accelerated in 2004 and this year. A friend who works at the firm, locally, confirmed that these are the effects of the last two major acquisitions. The latter one being Gillette, last year.

This has an interesting effect on P&G, called "riding the tiger." Notice that its sales growth rates, pre-acquisitions, were in the single digits, on the low side, on average. In the years prior to 2002, they were also rather meager. Thus, P&G has bought growth, twice. The year in between the acquisitions displays a 10% sales growth- higher than the earlier years, but still not so high as with the immediate folding-in of the purchased sales bases.

My proprietary research shows that the market tends to favor companies which can consistently generate superior revenue growth. P&G has begun to buy its growth. Either of two things need to occur, if the company is to have a good chance of becoming a consistently superior total return-generating company.

Either it needs to generate organic growth to match that of the effects of the acquisitions, or it needs to be able to continue its acquisition program, making it a sort of 'standard operating procedure," for which investors are prepared to pay. The company is hitting some pretty high revenue growth targets for a consumer goods conglomerate. While the 10% revenue growth in 2005 was good, and better than the long-term S&P average, it was by no means near the upper end of the distribution of revenue growth in the S&P500.

NIAT growth at P&G has also been getting better, but the best years were in the earlier years of this period.

Taken together, the revenue and NIAT growth pictures lead to the total return performance shown in the table. P&G has a much better average than the S&P for the last five years. However, the last two years have been a close call. Most of the 12 point spread in average total return between the S&P and P&G is accounted for by 2002. I would guess that would have been from a "flight to quality" by investors, as the tech-bubble-bursting recession drove investors to safer havens. Too, the low returns in 2004 and 2006 could be the result of investor verdicts on the prices of each of the two major acquisitions in the the prior two years.

I like P&G's customer focus. I understand the broadening of their product and business portfolios recently. However, from the data above, I seriously wonder if they can sustain raw revenue growth in the next few years. This is where consistency of revenue growth at fairly high rates really challenges a company. If too much of the firm's recent success on this dimension was simply purchasing growth, then I think total returns will ebb, along with organic growth.

It will be very interesting to watch P&G in the next few years to see how their fundamental operating capabilities prove out, and whether the market rewards the firm, if they do.

Sunday, July 30, 2006

America's Largest Banks: It's About More Than Size

This week's Wall Street Journal featured an article, on Friday, announcing that Bank of America (really the renamed NCNB of old) is about to become a larger bank, by market value, than Citigroup.

This week's Wall Street Journal featured an article, on Friday, announcing that Bank of America (really the renamed NCNB of old) is about to become a larger bank, by market value, than Citigroup.If this doesn't highlight the wrong measure, I don't know what does? Ranking the banks by deposits?

As it happens, BofA has been superior by a truly important measure for some time now. As the table above shows (click on it for a larger view), over the last five years, it's total return to shareholders has averaged 14.4%, while Sandy Weill/Chuck Prince's Citigroup has lost shareholders 3.9%, on average. During the same period, the S&P500 has gained 3.2% per year, on average. Further, BofA outperformed Citi for 3 of the 5 12-month periods, and nearly tied it in a fourth (2004).

Tying in with the Friday article, and another one earlier in the week, about Prince's vow to grow "operating leverage" are the upper rows of the table above. It clearly shows that Citi's revenue growth has been anemic for the past five years. Once again, except for 2002, BofA outgrew Citi in terms of revenues. Both have been accelerating since the bottom of the recent recession in 2002. Citi may be improving, but, again, BofA has done even better.

Granted, BofA is not yet sufficiently superior to make it into my portfolio selections. But at this rate, it'll be there years before Citi.

Size has nothing to do with the comparison of these two financial giants. Ken Lewis has been doing something a lot better than Chuck Prince and, or course, his predecessor, Sandy Weill. And the consistently better total returns prove it.

Subscribe to:

Posts (Atom)

{kind=link}