Today's Wall Street Journal featured a story on Microsoft's long road to embracing online advertising. It followed the gradually rising fortunes of Joanne Bradford, whom the company hired in 2001, from McGraw-Hill, to head that effort. She is soon to be named to head the MSN online group, at just 43 years of age.

That's the basic news contained in the story. The sad part is why it took the company five years to accept Ms. Bradford's strategy and efforts to do the job for which Microsoft hired her. Particularly embarrassing for the company are the reported antics of a David Cole, now on leave from Microsoft, and her one-time manager.

The article reminds me of my years at ATT, where outsiders had to attempt to break through resident narrowmindedness as the telecommunications giant struggled to ready itself for deregulation. Countless middle- and senior-level executives were hired to do jobs which some even more senior ATT executives and officers did not even agree were necessary.

Such seems to have been the case for Joanne Bradford at Microsoft. Meanwhile, as the WSJ piece details, Google roared past the software giant and revolutionized the online advertising business.

In taking five years to finally come to a realization that online ads are important to its future, it makes me wonder if Microsoft has enough time to recover from its mistakes in this area.

And, now, rather than recruit an online business executive, they are simply promoting Ms. Bradford, their online advertising executive. Granted, she seems to have finally persevered and won acceptance of her function at the firm. Does this make her the best overall online business leader?

Personally, I'd think more of Microsoft if it expanded Ms. Bradford's advertising duties and objectives, while recruiting a senior online business executive for the MSN online group.

Blogger is misbehaving today, so I am unable to paste a chart comparing Microsoft's five year stock price with the S&P500. Suffice to say, the latter is up about 20%, and the former is still negative.

Reading stories like this one, about the company's inability to coordinate its hiring and funding of key areas such as online advertising, suggest to me that Microsoft will continue to stumble in its efforts to compete in non-software-based business areas for some time to come.

Friday, November 17, 2006

Thursday, November 16, 2006

Wal-Mart In The Democrat Party's Crosshairs

This morning, on CNBC, the co-anchors discussed yesterday's attacks by Democratic Senator Obama (Ill), and former Democratic Senator Edwards (NC), upon Wal-Mart.

It has taken less than two weeks for the Democrats to begin to feel their oats over the prospect of the slimmest of majorities possible in the US Senate, come January.

Both Democrats, heard via recorded statements, excoriated the retailer for its wage levels and structures, and its health care policies. Edwards nebulously referred to "billionaire" senior executives of Wal-Mart, offering no evidence of his assertions, contrasting the alleged wealth to further assertions that low-level employees of the firm must apply for food stamps, school lunch programs, and other governmental transfer payments.

To his lasting credit, co-anchor Joe Kernan, apparently the only sensible, moderate voice on the panel, noted that Edwards offered no proof of his sweeping assertions, and that many individuals and institutions are the actual owners of Wal-Mart, via shareholding positions. Senior executives of the firm, whatever their compensations, are unlikely to hold any significant voting interest in their employer.

As readers of this blog may know, I am no fan of Wal-Mart. In many prior posts, which you may find by searching on the company's name at the top of the page, I have opined that Wal-Mart's executives have made some fairly spectacular blunders in the past year. Additionally, I simply believe that their current business model has run out of room for growth.

However, that does not merit these attacks from liberal Democrats who are prospective candidates for President in 2008. It would seem that, despite their single-seat Senate majority, the Democrats are beginning to behave as if they have veto-proof clout. By Obama's, and Edward's, demagogery, they are already revealing their true intentions, which were carefully hidden during the recent election campaign.

If memory serves me, Wal-Mart's lowest-level employees are now more likely to be part-time. Thus, they would probably not qualify for benefits such as health care. Whether this is a wise strategy or not, time will tell. If it proves to be a lightning rod for this type of publicity and, in time, legislation aimed at Wal-Mart, then it probably will not have been wise. But, this is the nature of free market enterprise. Companies experiment with their business models, within the context of the society and legal environments in which they exist.

My personal opinion is that Wal-Mart is suffering an unusual amount of self-inflicted damage from its various personnel, compensation and marketing strategies. However, the consequence for that should, and may be, a loss of business. It shouldn't be to become the corporate whipping boy of national office-seeking politicians.

Sometimes, the law of unintended consequences acts in exceptionally circuitous ways. It would be ironic indeed if, as a result of their recent victories in both Houses of Congress, the Democrats engaged in such virulent attacks upon the engines of economic wealth creation in America, such as Wal-Mart, so quickly, that they assured their own loss of control in the next cycle of elections.

For more on that theme, see this post.

It has taken less than two weeks for the Democrats to begin to feel their oats over the prospect of the slimmest of majorities possible in the US Senate, come January.

Both Democrats, heard via recorded statements, excoriated the retailer for its wage levels and structures, and its health care policies. Edwards nebulously referred to "billionaire" senior executives of Wal-Mart, offering no evidence of his assertions, contrasting the alleged wealth to further assertions that low-level employees of the firm must apply for food stamps, school lunch programs, and other governmental transfer payments.

To his lasting credit, co-anchor Joe Kernan, apparently the only sensible, moderate voice on the panel, noted that Edwards offered no proof of his sweeping assertions, and that many individuals and institutions are the actual owners of Wal-Mart, via shareholding positions. Senior executives of the firm, whatever their compensations, are unlikely to hold any significant voting interest in their employer.

As readers of this blog may know, I am no fan of Wal-Mart. In many prior posts, which you may find by searching on the company's name at the top of the page, I have opined that Wal-Mart's executives have made some fairly spectacular blunders in the past year. Additionally, I simply believe that their current business model has run out of room for growth.

However, that does not merit these attacks from liberal Democrats who are prospective candidates for President in 2008. It would seem that, despite their single-seat Senate majority, the Democrats are beginning to behave as if they have veto-proof clout. By Obama's, and Edward's, demagogery, they are already revealing their true intentions, which were carefully hidden during the recent election campaign.

If memory serves me, Wal-Mart's lowest-level employees are now more likely to be part-time. Thus, they would probably not qualify for benefits such as health care. Whether this is a wise strategy or not, time will tell. If it proves to be a lightning rod for this type of publicity and, in time, legislation aimed at Wal-Mart, then it probably will not have been wise. But, this is the nature of free market enterprise. Companies experiment with their business models, within the context of the society and legal environments in which they exist.

My personal opinion is that Wal-Mart is suffering an unusual amount of self-inflicted damage from its various personnel, compensation and marketing strategies. However, the consequence for that should, and may be, a loss of business. It shouldn't be to become the corporate whipping boy of national office-seeking politicians.

Sometimes, the law of unintended consequences acts in exceptionally circuitous ways. It would be ironic indeed if, as a result of their recent victories in both Houses of Congress, the Democrats engaged in such virulent attacks upon the engines of economic wealth creation in America, such as Wal-Mart, so quickly, that they assured their own loss of control in the next cycle of elections.

For more on that theme, see this post.

Wednesday, November 15, 2006

Three Blind Mice: The Auto CEOs Visit White House

Yesterday's news featured clips of the White House meeting between President Bush and his staff, and GM Chairman and Chief Executive Rick Wagoner, Ford Chief Executive Alan Mulally and Tom LaSorda, president and chief executive officer of Chrysler Group.

Among the topics said to be on the agenda were: CAFE regulations; health care cost reductions for American auto manufacturers, and; ethanol fuel distribution infrastructural support.

There seems to be an irony that these publicly-held firms want help when others in their industry appear to be making money in this country. One does not see executives from Toyota, Honda, or Mercedes going, hats in hands, to the White House for protectionist favors.

However, with Bill Ford's recent remarks about China in mind, as alluded to in this recent post, yesterday's effort seems to be a case of "spitting into the wind."

To wit, if one really believes that China is the next destination for a large number of global automotive production jobs, why bother asking for help from the US federal government? Trends as large as that of China sucking up the relatively lower-paying auto assembly jobs are hardly going to be stopped by the actions of the American government. A few protectionist laws here or there will just start a trade war, and at a time when the Doha round is already in trouble.

Plus, even if the Detroit-based auto manufacturers were given concessions by the White House and Congress, in exchange for jobs preservation, how will those companies explain the need for even more help, subsequently, when continued cost and pricing pressure from China overwhelm this round of bailouts?

Isn't Ford's investment in China, per the prior linked blog post, evidence that the company sees more future there than in the US for automotive production? Doesn't that make a mockery of petitioning the White House for help, even as Ford relatively disinvests in the US?

Among the topics said to be on the agenda were: CAFE regulations; health care cost reductions for American auto manufacturers, and; ethanol fuel distribution infrastructural support.

There seems to be an irony that these publicly-held firms want help when others in their industry appear to be making money in this country. One does not see executives from Toyota, Honda, or Mercedes going, hats in hands, to the White House for protectionist favors.

However, with Bill Ford's recent remarks about China in mind, as alluded to in this recent post, yesterday's effort seems to be a case of "spitting into the wind."

To wit, if one really believes that China is the next destination for a large number of global automotive production jobs, why bother asking for help from the US federal government? Trends as large as that of China sucking up the relatively lower-paying auto assembly jobs are hardly going to be stopped by the actions of the American government. A few protectionist laws here or there will just start a trade war, and at a time when the Doha round is already in trouble.

Plus, even if the Detroit-based auto manufacturers were given concessions by the White House and Congress, in exchange for jobs preservation, how will those companies explain the need for even more help, subsequently, when continued cost and pricing pressure from China overwhelm this round of bailouts?

Isn't Ford's investment in China, per the prior linked blog post, evidence that the company sees more future there than in the US for automotive production? Doesn't that make a mockery of petitioning the White House for help, even as Ford relatively disinvests in the US?

Tuesday, November 14, 2006

TimeWarner To Buy Kool-Aid: Parsons' Thirst Seems Unquenchable

I caught some of Dick Parsons' interview from Jim Cramer's nightly TV program on CNBC, as it was replayed (mid-last-week) on CNBC's "SquawkBox."

To say that Parsons is self-delusional is to be kind. Let's hope he's simply being "diplomatic," as others have described him with increasing frequency recently.

He opined that TW is all about publishing, and the premier company in print publishing. He went on to blithely proclaim that online publishing is publishing, too, so TW will simply enter that market and triumph there, as well.

Personally, when someone is so disconnected from reality as Parsons seems to be, I find it distinctly unsettling.

For instance, read my posts here and here, regarding TW's travails. A few weeks of mild stock price recovery has not fundamentally altered the five-year picture portrayed in the chart in the second post/link.

Separately, I had a chance discussion recently with a manager from one of TW's units, and the manager confirmed what I have been reading in the press lately. It doesn't sound good.

With Dick Parsons drinking so much Kool-Aid, perhaps TimeWarner should just acquire the brand, and save money on wholesale purchases.

To say that Parsons is self-delusional is to be kind. Let's hope he's simply being "diplomatic," as others have described him with increasing frequency recently.

He opined that TW is all about publishing, and the premier company in print publishing. He went on to blithely proclaim that online publishing is publishing, too, so TW will simply enter that market and triumph there, as well.

Personally, when someone is so disconnected from reality as Parsons seems to be, I find it distinctly unsettling.

For instance, read my posts here and here, regarding TW's travails. A few weeks of mild stock price recovery has not fundamentally altered the five-year picture portrayed in the chart in the second post/link.

Separately, I had a chance discussion recently with a manager from one of TW's units, and the manager confirmed what I have been reading in the press lately. It doesn't sound good.

With Dick Parsons drinking so much Kool-Aid, perhaps TimeWarner should just acquire the brand, and save money on wholesale purchases.

Monday, November 13, 2006

CEO Performance: Terry McGraw vs. Jeff Immelt

Last week's recent appearance of Terry McGraw on CNBC's morning program, SquawkBox, left me with an initial reaction of, "why is that guy hosting this program?"

In the many years that I have run monthly selections for my equity portfolio strategy, I don't believe McGraw's company, McGraw-Hill, has ever been among those chosen. McGraw is apparently the current chairman of the Business Roundtable.

On the same program, a reporter from the Financial Times was interviewed regarding her interview with Jeff Immelt, CEO of GE. This caused someone on the set to refer to Immelt as the "dean of American business."

Now, about this time, I got to wondering, which of the two CEOs has performed better over the past five years? I know Immelt's record- he's essentially wasted his shareholder's money by underperforming the S&P during his "deanship" at the helm of GE.

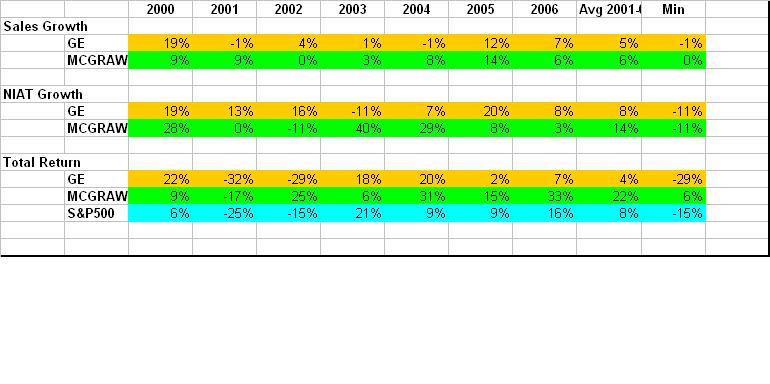

But, being the data-driven guy that I am, I took a fresh look at the current five-year numbers on sales and NIAT growth, as well as total return, for GE and McGraw-Hill.

The chart on the left (click on it to view the enlarged version) contains the annual growth rates for the three measures.

The chart on the left (click on it to view the enlarged version) contains the annual growth rates for the three measures.

It's not even close- Terry McGraw has clearly outmanaged Jeff Immelt, in terms of performance on these three key variables- for the past five years.

First, it's clear that both companies are among the low-growth type of large-caps. They have nearly identical average sales growth rates of 5% (GE) and 6% (MHP). However, McGraw-Hill, at 14%, has nearly double the average growth rate of GE's 8% for Net Income After Tax. As a result, McGraw-Hill's average annual total return for the last five years is 22%, to GE's 4%, and the S&P's 8%.

As my proprietary research has discovered, for slow-growth companies, profit growth and ROE are important determinants of total return performance. Investors clearly view the companies similarly as low-growth enterprises, and, thus, value McGraw-Hill's superior ability to consistently wring profits out of sluggishly-growing businesses. GE has simply not kept pace.

I think FT missed the boat by focusing on Immelt. For such a diversified and tough collection of businesses, Terry McGraw would have had something more to convey to FT's readership. All Immelt can really discuss is how to get overpaid and underperform while running a mediocre closed-end mutual fund. For more detail on this, simply search this blog for "immelt" and you'll find a collection of my prior pieces on Immelt's dismal performance as CEO of GE.

I'm glad I happened to be watching CNBC that morning, because I have a new respect for McGraw-Hill and its CEO. I'm still doubtful that the company will be selected for even my low-growth portfolio component, because its sales growth, while far slower than that of the average high-growth large-cap company, is still sufficiently high to be exceeding the S&P's average rate periodically.

Despite that, Terry McGraw appears to be producing a low-probability event, in that he has outperformed the S&P consistently over the past five years. There's no denying the data- he's clearly done a better job for his shareholders than Jeff Immelt has for his.

In the many years that I have run monthly selections for my equity portfolio strategy, I don't believe McGraw's company, McGraw-Hill, has ever been among those chosen. McGraw is apparently the current chairman of the Business Roundtable.

On the same program, a reporter from the Financial Times was interviewed regarding her interview with Jeff Immelt, CEO of GE. This caused someone on the set to refer to Immelt as the "dean of American business."

Now, about this time, I got to wondering, which of the two CEOs has performed better over the past five years? I know Immelt's record- he's essentially wasted his shareholder's money by underperforming the S&P during his "deanship" at the helm of GE.

But, being the data-driven guy that I am, I took a fresh look at the current five-year numbers on sales and NIAT growth, as well as total return, for GE and McGraw-Hill.

The chart on the left (click on it to view the enlarged version) contains the annual growth rates for the three measures.

The chart on the left (click on it to view the enlarged version) contains the annual growth rates for the three measures.It's not even close- Terry McGraw has clearly outmanaged Jeff Immelt, in terms of performance on these three key variables- for the past five years.

First, it's clear that both companies are among the low-growth type of large-caps. They have nearly identical average sales growth rates of 5% (GE) and 6% (MHP). However, McGraw-Hill, at 14%, has nearly double the average growth rate of GE's 8% for Net Income After Tax. As a result, McGraw-Hill's average annual total return for the last five years is 22%, to GE's 4%, and the S&P's 8%.

As my proprietary research has discovered, for slow-growth companies, profit growth and ROE are important determinants of total return performance. Investors clearly view the companies similarly as low-growth enterprises, and, thus, value McGraw-Hill's superior ability to consistently wring profits out of sluggishly-growing businesses. GE has simply not kept pace.

I think FT missed the boat by focusing on Immelt. For such a diversified and tough collection of businesses, Terry McGraw would have had something more to convey to FT's readership. All Immelt can really discuss is how to get overpaid and underperform while running a mediocre closed-end mutual fund. For more detail on this, simply search this blog for "immelt" and you'll find a collection of my prior pieces on Immelt's dismal performance as CEO of GE.

I'm glad I happened to be watching CNBC that morning, because I have a new respect for McGraw-Hill and its CEO. I'm still doubtful that the company will be selected for even my low-growth portfolio component, because its sales growth, while far slower than that of the average high-growth large-cap company, is still sufficiently high to be exceeding the S&P's average rate periodically.

Despite that, Terry McGraw appears to be producing a low-probability event, in that he has outperformed the S&P consistently over the past five years. There's no denying the data- he's clearly done a better job for his shareholders than Jeff Immelt has for his.

Subscribe to:

Posts (Atom)