Last Thursday, the Wall Street Journal featured a piece on Indian scientists now returning to India. As with Chinese engineers, many of the scientists have formerly been with large American firms- in this case, pharmaceuticals.

On the whole, though, I believe it's a good thing. India becomes more wired into global trade, as its scientists begin to develop new medicines and seek to export them. It will open India up, much as the evolving economy of China will for that country.

In time, Indian pharma wages will rise, and even it will gradually become less competitive, on a comparative basis. Of course, as more Indian professionals return and start competing firms in technology, pharmaceuticals, commodities, etc, their standards of living will rise, and they will consume more international goods and services. Many, no doubt, will be American in origin.

Perhaps, over the next decade, Western firms will begin to acquire some of these Indian startups, in the same way they often buy ideas and talent in the US that left the paralysis of large corporations, to start new businesses. We don't yet know what India will adopt as a policy involving this sort of acquisition activity, but it may well become more important for world trade in the coming years. Will Western countries and markets remain open to Indian and Chinese markets that constrict asset purchases, ownership, and economic participation by foreign companies?

How will a Democratic US Congress view the loss of higher-paying, management jobs to countries such as India? Especially if the latter maintains trade barriers, while attempting to export newly-developed products and services?

This is free trade. Isn't this what we, as Americans, ultimately want? Comparative advantage and mobility work. If this is what it takes to re-energize some sectors of large corporate America, as it sees an ethnic brain drain, so be it.

The migration of highly-educated talent back to home countries may, on one hand, look like a net loss for America. However, it may well result, as in China, in the accelerated Westernization of these formerly-third-world countries, so that their economic, social and political values and agendas begin to more closely resemble those of America and her Western allies. As we move further into what promises to be a long global war on terror, initiated by radical elements of Islam, can it be a bad thing to have the world's two most populous nations begin to adopt America's perspectives on economic growth, development, and living standards?

Rather than see a brain drain, perhaps we should view developments such as the Indian scientists returning home as a net loss to the US, perhaps we should see it as successful export of, and prostyletizing on behalf of, our values and socio-economic system. Much cheaper, and more effective, than military conquest of foreign lands. This way, our economic system becomes embedded into other cultures, and fosters nascent democratic political appetites, as well.

Thursday, December 21, 2006

Wednesday, December 20, 2006

Home Depot, Again: Leon Cooperman's "Powerful Numbers"

Yesterday afternoon, Maria Bartiromo interviewed Omega Fund founder CEO, Leon Cooperman, by telephone, on CNBC. The "video," with Cooperman's audio, can be viewed here.

I must admit that I found the 'interview' to be rather unusual. Rather than have Cooperman interact, on camera or via microphones, with one Ralph Whitworth, another institutional investor who is assailing Home Depot's board and management for ineptitude, Bartiromo/CNBC chose to simply refer to Whitworth, show a video clip of an earlier interview with him, and then present Cooperman live, alone. She opened the piece by citing Omega's 5 1/4 B of assets under management, and its position of 2.5MM shares of HD. The nature of the introduction seemed calculated to confer some sort of infallibility on Cooperman and his investing choices.

Could Lee be 'pumping' Home Depot, with CNBC's help? Or, at the least, defending it?

Let me be very clear here. I am not saying that Cooperman, Bartiromo, or CNBC did anything illegal. Omega's beneficial interest in Home Depot was explicitly stated at the beginning of the interview. However, it is indisputable that CNBC had Cooperman appear in order to tout a stock in which his fund has a fairly large position. Further, they had him on after another investor who had made pointed allegations of board and managerial failures to perform.

Cooperman went on to list a set of reasons to risk your capital on HD. He gave testimonials on Nardelli, via Jack Welch, Nardelli's one-time manager at GE, on Welch himself, and on two directors of HD. Fine. But, where's the beef?

Maria said, in agreement with Cooperman, of Nardelli's operating record,

"the numbers are powerful....revenues, earnings.....powerful under Nardelli....no doubt about it."

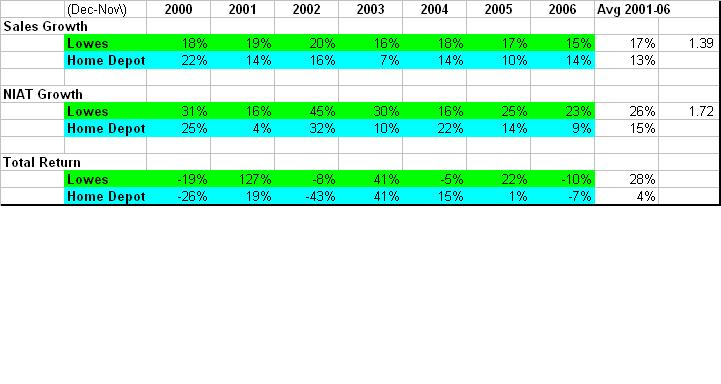

Really? Look at the chart on the left, displaying the performance of sales, NIAT, and total return for Home Depot and Lowes since 2000. You may click on the chart, and on the subsequent stock price charts, to view larger versions of all of them.

Really? Look at the chart on the left, displaying the performance of sales, NIAT, and total return for Home Depot and Lowes since 2000. You may click on the chart, and on the subsequent stock price charts, to view larger versions of all of them.

Sales growth has finally accelerated again at HD in the last twelve months, but it still lags that of its major competitor, Lowes. Net Income Available after Taxes, up 9% for the past twelve months, is the lowest increase since the first full year under Nardelli. And, again, it lags Lowes by more than twofold.

Powerful performance, eh, Bob...Maria....Lee? I just don't see it. I didn't see it, here, or here, either, in my posts on this topic back in July of this year.

Cooperman went on to list a series of rapid-fire 'data' about Home Depot. Its real estate position has increased. Dividends and earnings up over a short period of time. The company bought stock back. So what? These are intermediate activities which are not having an effect on the firm's stock price. That Lee Cooperman thinks they should is beside the point, isn't it? Unless his personal opinion is supposed to be sufficient reason to buy the stock. Which would be nice for him, since his fund, remember, already owns 2.5MM shares of Home Depot.

Cooperman clearly believes, as a result of his fund's analytical team's meetings with HD's management, that the company's stock will eventually be appreciated, even though, now, it's "undervalued." His reeling off of the many operating statistics, mostly rather abstruse numbers, sounded like he was reading from a list his analysts had prepared for him.

Specifically, it reminds me of my own experiences in corporate America. The staffers build a set of numbers and talking points so that the senior executive, who is not as well-versed on the topic, can rattle off seemingly-unassailable numbers. Do you think any of the carefully-selected data presented by Cooperman, on behalf of his analysts, will be negative or cast doubt on Home Depot's 'powerful' operating results? Unlikely.

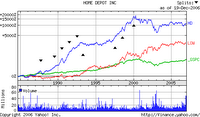

To get a better picture, here's a Yahoo-sourced chart of stock prices for Home Depot and Lowes, plus the S&P500 Index, for the past five years. Lowes is clearly superior, and HD can't even outperform the S&P. Despite Cooperman's plea that the firm is simply misunderstood, the market

To get a better picture, here's a Yahoo-sourced chart of stock prices for Home Depot and Lowes, plus the S&P500 Index, for the past five years. Lowes is clearly superior, and HD can't even outperform the S&P. Despite Cooperman's plea that the firm is simply misunderstood, the market

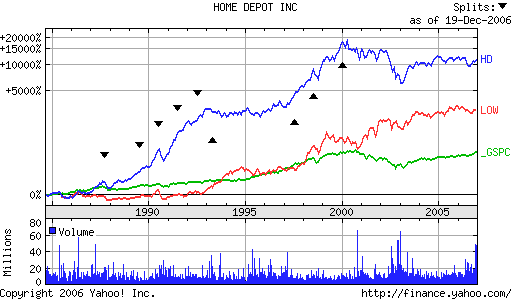

For a little more perspective, here's a chart of the same data for a much longer timeframe. It's clear that, since 2000, things have never been as good for Home Depot as they were before then. Nothing that Nardelli has done for six years has succeeded in improving the company's total return to beat that of the S&P500.

For a little more perspective, here's a chart of the same data for a much longer timeframe. It's clear that, since 2000, things have never been as good for Home Depot as they were before then. Nothing that Nardelli has done for six years has succeeded in improving the company's total return to beat that of the S&P500.

Meanwhile, Lowes' stock price has continued to rise steadily, though not, apparently, much faster than the index since around 2001.

The only basis on which I saw improvement in HD's stock was in the last three months. Blogger is not cooperating with my attempts to paste a stock price chart. However, Yahoo's charts shows that, over the past 90 days, HD has outperformed Lowes, roughly 9% vs. flat, but still underperformed the S&P.

Of course, if Cooperman's premise is that you have to catch the right 3-6 month period in order to earn superior returns in Home Depot, I don't think that's going to help most investors. It sounds more like investing on technical indicators, and hopes of a short-term "pop" from some transitory fundamentals in the near future, then correctly timing your exit from the position.

However, in terms of long-term, consistent performance, Home Depot does not appear to have improved since my analysis in July of this year. And, on a comparative basis, it does not seem to be performing "powerfully" at all, Maria Bartiromo's and Leon Cooperman's contentions to the contrary. I attempt to present the data on which I base my assessments whenever I critique a company's performance. For me, the Cooperman interview on CNBC, and Bartiromo's and Cooperman's statements claiming great fundamental performance for Home Depot, seem empty without clear, written or graphic evidence to substantiate them.

I must admit that I found the 'interview' to be rather unusual. Rather than have Cooperman interact, on camera or via microphones, with one Ralph Whitworth, another institutional investor who is assailing Home Depot's board and management for ineptitude, Bartiromo/CNBC chose to simply refer to Whitworth, show a video clip of an earlier interview with him, and then present Cooperman live, alone. She opened the piece by citing Omega's 5 1/4 B of assets under management, and its position of 2.5MM shares of HD. The nature of the introduction seemed calculated to confer some sort of infallibility on Cooperman and his investing choices.

Could Lee be 'pumping' Home Depot, with CNBC's help? Or, at the least, defending it?

Let me be very clear here. I am not saying that Cooperman, Bartiromo, or CNBC did anything illegal. Omega's beneficial interest in Home Depot was explicitly stated at the beginning of the interview. However, it is indisputable that CNBC had Cooperman appear in order to tout a stock in which his fund has a fairly large position. Further, they had him on after another investor who had made pointed allegations of board and managerial failures to perform.

Cooperman went on to list a set of reasons to risk your capital on HD. He gave testimonials on Nardelli, via Jack Welch, Nardelli's one-time manager at GE, on Welch himself, and on two directors of HD. Fine. But, where's the beef?

Maria said, in agreement with Cooperman, of Nardelli's operating record,

"the numbers are powerful....revenues, earnings.....powerful under Nardelli....no doubt about it."

Really? Look at the chart on the left, displaying the performance of sales, NIAT, and total return for Home Depot and Lowes since 2000. You may click on the chart, and on the subsequent stock price charts, to view larger versions of all of them.

Really? Look at the chart on the left, displaying the performance of sales, NIAT, and total return for Home Depot and Lowes since 2000. You may click on the chart, and on the subsequent stock price charts, to view larger versions of all of them.Sales growth has finally accelerated again at HD in the last twelve months, but it still lags that of its major competitor, Lowes. Net Income Available after Taxes, up 9% for the past twelve months, is the lowest increase since the first full year under Nardelli. And, again, it lags Lowes by more than twofold.

Powerful performance, eh, Bob...Maria....Lee? I just don't see it. I didn't see it, here, or here, either, in my posts on this topic back in July of this year.

Cooperman went on to list a series of rapid-fire 'data' about Home Depot. Its real estate position has increased. Dividends and earnings up over a short period of time. The company bought stock back. So what? These are intermediate activities which are not having an effect on the firm's stock price. That Lee Cooperman thinks they should is beside the point, isn't it? Unless his personal opinion is supposed to be sufficient reason to buy the stock. Which would be nice for him, since his fund, remember, already owns 2.5MM shares of Home Depot.

Cooperman clearly believes, as a result of his fund's analytical team's meetings with HD's management, that the company's stock will eventually be appreciated, even though, now, it's "undervalued." His reeling off of the many operating statistics, mostly rather abstruse numbers, sounded like he was reading from a list his analysts had prepared for him.

Specifically, it reminds me of my own experiences in corporate America. The staffers build a set of numbers and talking points so that the senior executive, who is not as well-versed on the topic, can rattle off seemingly-unassailable numbers. Do you think any of the carefully-selected data presented by Cooperman, on behalf of his analysts, will be negative or cast doubt on Home Depot's 'powerful' operating results? Unlikely.

To get a better picture, here's a Yahoo-sourced chart of stock prices for Home Depot and Lowes, plus the S&P500 Index, for the past five years. Lowes is clearly superior, and HD can't even outperform the S&P. Despite Cooperman's plea that the firm is simply misunderstood, the market

To get a better picture, here's a Yahoo-sourced chart of stock prices for Home Depot and Lowes, plus the S&P500 Index, for the past five years. Lowes is clearly superior, and HD can't even outperform the S&P. Despite Cooperman's plea that the firm is simply misunderstood, the market For a little more perspective, here's a chart of the same data for a much longer timeframe. It's clear that, since 2000, things have never been as good for Home Depot as they were before then. Nothing that Nardelli has done for six years has succeeded in improving the company's total return to beat that of the S&P500.

For a little more perspective, here's a chart of the same data for a much longer timeframe. It's clear that, since 2000, things have never been as good for Home Depot as they were before then. Nothing that Nardelli has done for six years has succeeded in improving the company's total return to beat that of the S&P500.Meanwhile, Lowes' stock price has continued to rise steadily, though not, apparently, much faster than the index since around 2001.

The only basis on which I saw improvement in HD's stock was in the last three months. Blogger is not cooperating with my attempts to paste a stock price chart. However, Yahoo's charts shows that, over the past 90 days, HD has outperformed Lowes, roughly 9% vs. flat, but still underperformed the S&P.

Of course, if Cooperman's premise is that you have to catch the right 3-6 month period in order to earn superior returns in Home Depot, I don't think that's going to help most investors. It sounds more like investing on technical indicators, and hopes of a short-term "pop" from some transitory fundamentals in the near future, then correctly timing your exit from the position.

However, in terms of long-term, consistent performance, Home Depot does not appear to have improved since my analysis in July of this year. And, on a comparative basis, it does not seem to be performing "powerfully" at all, Maria Bartiromo's and Leon Cooperman's contentions to the contrary. I attempt to present the data on which I base my assessments whenever I critique a company's performance. For me, the Cooperman interview on CNBC, and Bartiromo's and Cooperman's statements claiming great fundamental performance for Home Depot, seem empty without clear, written or graphic evidence to substantiate them.

Tuesday, December 19, 2006

Income Inequality

Alan Reynolds wrote a fabulous piece in the Wall Street Journal last Thursday concerning America's alleged income inequality. It is a masterpiece in demonstrating that attention to details, and knowledge of data sources, can make all the difference between a valid conclusion, and useless speculation.

Specifically, Reynolds, who is a senior fellow at the Cato Institute, and co-founder of Polyconomics, identifies the source of Senatorial candidate Jim Webb's statement that,

"the top 1% now takes in an astounding 16% of national income, up from 8% in 1980."

The researchers responsible for these numbers, Thomas Piketty, of Ecole Normale Superieure in Paris, and Emmanuel Saez, of the University of California at Berkeley, used tax returns for their denominator, rather than total income. Major income sources which they omitted, according to Reynolds, were Social Security and other transfer payments. Of course, we would expect these types of payments to go to lower income earners, thus further skewing the findings of the two researchers.

Other sources of error include the non-filing of some income earners, municipal bond and other tax-exempt income sources, and the inclusion of two, joint filers on single tax returns at the higher end of the tax-reported income spectrum. Reynolds estimates that total personal incomes, the denominator for the inequality statistics, was roughly $3.3B in 2004, or slightly more than 1/3 larger than Piketty and Saez estimated.

Another source of error which Reynolds discusses is the tax-policy-driven shift of small, formerly conventionally-filing corporations, to Subchapter S corporations. These are often higher income sources taking advantage of a different reporting structure, thus improperly appearing to inflate upper incomes, when, in reality, they were simply measured as business income sources in prior years.

Reynolds' fine, detailed and sensible work demonstrates how easily such inflammatory statistics as the ones Senator-elect Webb (D-Va) used can become commonly held "wisdom," or "fact."

In reality, it appears that the work on which those statistics are based was very flawed, and has generated suspect results. As time-consuming, dry and tedious as it may be, doing the fundamental work of investigating definitions and research methodologies can often shed valuable, and, occasionally, disconfirming light on apparently important and troubling results. Such is the case with the now-well-publicized 'increasing income inequality' in America, as demonstrated by Alan Reynold's good work and articulate explanations.

Specifically, Reynolds, who is a senior fellow at the Cato Institute, and co-founder of Polyconomics, identifies the source of Senatorial candidate Jim Webb's statement that,

"the top 1% now takes in an astounding 16% of national income, up from 8% in 1980."

The researchers responsible for these numbers, Thomas Piketty, of Ecole Normale Superieure in Paris, and Emmanuel Saez, of the University of California at Berkeley, used tax returns for their denominator, rather than total income. Major income sources which they omitted, according to Reynolds, were Social Security and other transfer payments. Of course, we would expect these types of payments to go to lower income earners, thus further skewing the findings of the two researchers.

Other sources of error include the non-filing of some income earners, municipal bond and other tax-exempt income sources, and the inclusion of two, joint filers on single tax returns at the higher end of the tax-reported income spectrum. Reynolds estimates that total personal incomes, the denominator for the inequality statistics, was roughly $3.3B in 2004, or slightly more than 1/3 larger than Piketty and Saez estimated.

Another source of error which Reynolds discusses is the tax-policy-driven shift of small, formerly conventionally-filing corporations, to Subchapter S corporations. These are often higher income sources taking advantage of a different reporting structure, thus improperly appearing to inflate upper incomes, when, in reality, they were simply measured as business income sources in prior years.

Reynolds' fine, detailed and sensible work demonstrates how easily such inflammatory statistics as the ones Senator-elect Webb (D-Va) used can become commonly held "wisdom," or "fact."

In reality, it appears that the work on which those statistics are based was very flawed, and has generated suspect results. As time-consuming, dry and tedious as it may be, doing the fundamental work of investigating definitions and research methodologies can often shed valuable, and, occasionally, disconfirming light on apparently important and troubling results. Such is the case with the now-well-publicized 'increasing income inequality' in America, as demonstrated by Alan Reynold's good work and articulate explanations.

Monday, December 18, 2006

Toyota's Awesome Drive To Dominance

Last (December 10th) weekend's Wall Street Journal featured an article about Toyota. Having a series of more timely pieces which occurred last week, I elected to wait until now to accord this post the attention it deserves. There are several important insights to be gleaned from the Journal article concerning my research and thoughts about consistently superior performance. Toyota is showing both the good and the bad effects of consistently superior performance- how to do it, what it returns, how fragile and fleeting it can be.

What initially struck me from the Journal piece is how Toyota CEO Katsuaki Watanbe's incredible insecurity fuels his company's continued excellent performance.

What initially struck me from the Journal piece is how Toyota CEO Katsuaki Watanbe's incredible insecurity fuels his company's continued excellent performance.

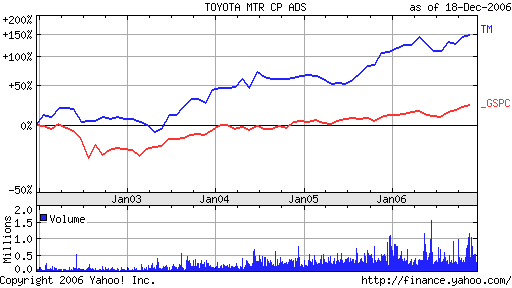

As the nearby, Yahoo-sourced chart of Toyota's stock price, versus the S&P500 Index, indicates, the company has performed consistently better than the latter for most of the past five years. It's cumulative total return far surpasses that of the index over the entire period. Toyota isn't among the companies in the S&P500, so I don't own it. How I wish I could, and did.

As my proprietary research warns, however, cost-cutting is a relatively limited weapon in the quest for long-term, consistently superior total returns. Toyota's are already nearing an end as a competitive weapon. The rate of cost reductions is slowing, and product design flaws have recently spurred recalls of more vehicles than it sold last year.

I was very impressed with the attention to detail by the CEO. The Journal article discusses his observant manner as he walks the floor of his plants. His questioning of the traditional, long paint shop river, is what recently has led to Toyota's secret new process, which takes far less space and resources. Watanabe is ceaselessly exploring new ways to drive costs down and extend Toyota's lead in this area. To this end, he has commissioned a total re-evaluation of the production of the company's vehicles, with an audacious objective of cutting the number of parts required by 50%.

While, on one hand, Toyota is bumping up against some cost-cutting limits of current production methods, Watanabe is wisely opening up the company's managers to exploring entirely new ways of designing and producing their vehicles, thus, effectively, in microeconomics terms, putting the firm's operations on a new, longer-term, declining cost curve. They have redesigned their machines to be smaller, and their plants as well.

What amazes me about Toyota is that, while GM is catching up to them in some production efficiency measures in some plants, Toyota is already moving to tackle new production challenges that I cannot even imagine GM being ready to address. The production plant challenge is one, as is the paint line. Thus, Toyota is working on changing the very methods by which they will more efficiently pump out vehicles, while GM, and, presumably, Ford, are still working on making existing methods merely more efficient. It's clear that the two American auto giants are not even remotely in the same class as Toyota when it comes to conceiving and implementing continuous methods of improving operating efficiencies, and, thus, value-added.

Will Toyota succeed in these operational changes? Their diminishing lead in current efficiencies demonstrates how cost leadership can shrink, and, thus, lead to a loss of sustained superior performance. However, they are attempting new initiatives to retain this consistently superior total return performance. Either way, they are at risk.

And this, I believe, is one of the most enlightening elements of the Journal's Toyota story. Even a detail- and big-picture-obsessed, experienced and successful CEO, like Watanable, with a willing workforce, and strong competitive position, cannot count on continued superior total return performance. He's betting the company's continued performance every year, with each new initiative.

Sooner or later, Toyota will run into more difficulties in one of its programs for new production methods, or design flaws, that will derail its superb performance of the past few years. The truth is, with each additional year of excellent performance, their odds of another one diminish. It's simply how performance patterns are among large numbers of large corporations.

However, I will take great interest in seeing for how long this impressive auto producer can maintain its record of consistently outperforming the S&P500's total return.

What initially struck me from the Journal piece is how Toyota CEO Katsuaki Watanbe's incredible insecurity fuels his company's continued excellent performance.

What initially struck me from the Journal piece is how Toyota CEO Katsuaki Watanbe's incredible insecurity fuels his company's continued excellent performance.As the nearby, Yahoo-sourced chart of Toyota's stock price, versus the S&P500 Index, indicates, the company has performed consistently better than the latter for most of the past five years. It's cumulative total return far surpasses that of the index over the entire period. Toyota isn't among the companies in the S&P500, so I don't own it. How I wish I could, and did.

As my proprietary research warns, however, cost-cutting is a relatively limited weapon in the quest for long-term, consistently superior total returns. Toyota's are already nearing an end as a competitive weapon. The rate of cost reductions is slowing, and product design flaws have recently spurred recalls of more vehicles than it sold last year.

I was very impressed with the attention to detail by the CEO. The Journal article discusses his observant manner as he walks the floor of his plants. His questioning of the traditional, long paint shop river, is what recently has led to Toyota's secret new process, which takes far less space and resources. Watanabe is ceaselessly exploring new ways to drive costs down and extend Toyota's lead in this area. To this end, he has commissioned a total re-evaluation of the production of the company's vehicles, with an audacious objective of cutting the number of parts required by 50%.

While, on one hand, Toyota is bumping up against some cost-cutting limits of current production methods, Watanabe is wisely opening up the company's managers to exploring entirely new ways of designing and producing their vehicles, thus, effectively, in microeconomics terms, putting the firm's operations on a new, longer-term, declining cost curve. They have redesigned their machines to be smaller, and their plants as well.

What amazes me about Toyota is that, while GM is catching up to them in some production efficiency measures in some plants, Toyota is already moving to tackle new production challenges that I cannot even imagine GM being ready to address. The production plant challenge is one, as is the paint line. Thus, Toyota is working on changing the very methods by which they will more efficiently pump out vehicles, while GM, and, presumably, Ford, are still working on making existing methods merely more efficient. It's clear that the two American auto giants are not even remotely in the same class as Toyota when it comes to conceiving and implementing continuous methods of improving operating efficiencies, and, thus, value-added.

Will Toyota succeed in these operational changes? Their diminishing lead in current efficiencies demonstrates how cost leadership can shrink, and, thus, lead to a loss of sustained superior performance. However, they are attempting new initiatives to retain this consistently superior total return performance. Either way, they are at risk.

And this, I believe, is one of the most enlightening elements of the Journal's Toyota story. Even a detail- and big-picture-obsessed, experienced and successful CEO, like Watanable, with a willing workforce, and strong competitive position, cannot count on continued superior total return performance. He's betting the company's continued performance every year, with each new initiative.

Sooner or later, Toyota will run into more difficulties in one of its programs for new production methods, or design flaws, that will derail its superb performance of the past few years. The truth is, with each additional year of excellent performance, their odds of another one diminish. It's simply how performance patterns are among large numbers of large corporations.

However, I will take great interest in seeing for how long this impressive auto producer can maintain its record of consistently outperforming the S&P500's total return.

Wal-Mart Employee Attacks Customer

It's true that sometimes, only one rotten apple is necessary to spoil the whole barrel. As rational adults, on one level, we know this to mean that we shouldn't judge an entire organization by the actions of a single member.

Still, with all the outrage and angst Wal-Mart has generated this year, much of it self-inflicted, this episode, occurring at a Wal-Mart store in Gainesville, Florida, is hardly what Lee Scott needed to read about on this pre-Christmas holiday weekend. My consulting friend S sent me this link to the following story.......

Woman Slashed At Gainesville Wal-Mart 12/17/2006 By Michael Maurino

WCJB TV-20 News

One local teen went to a store to go shopping and ended up taking a trip to the hospital after a fight with an employee.

Now the store employee is facing jail time after slashing her across the neck.

Gainesville Police say the 17-year-old teenage girl was visiting the Wal-Mart on Northwest 13th Street.

She had walked out of the store, but went back when she thought she left her cell phone in a shopping cart.

Detectives say she approached 18-year-old Wal-Mart employee Darius stacy, who was retreving the carts, and asked if he had the phone.

The two started arguing, and then shoving each other before Stacy pulled out a weapon.

"The employee had a box cutter and he cut the 17 year old in the throat," said GPD Sgt. Keith Kameg. "Fortunately, they were non life threatening injures."

The young woman was treated at Shands U-F for a cut that extended from her left ear to her windpipe.

Stacy is being charged with attempted murder.

Need we mention something about every employee being a 'goodwill' ambassador? It's pretty rough when you now have to worry about contact with even the cart handlers at the nation's largest retailer.

Certainly it argues for online shopping, does it not?

Still, with all the outrage and angst Wal-Mart has generated this year, much of it self-inflicted, this episode, occurring at a Wal-Mart store in Gainesville, Florida, is hardly what Lee Scott needed to read about on this pre-Christmas holiday weekend. My consulting friend S sent me this link to the following story.......

Woman Slashed At Gainesville Wal-Mart 12/17/2006 By Michael Maurino

WCJB TV-20 News

One local teen went to a store to go shopping and ended up taking a trip to the hospital after a fight with an employee.

Now the store employee is facing jail time after slashing her across the neck.

Gainesville Police say the 17-year-old teenage girl was visiting the Wal-Mart on Northwest 13th Street.

She had walked out of the store, but went back when she thought she left her cell phone in a shopping cart.

Detectives say she approached 18-year-old Wal-Mart employee Darius stacy, who was retreving the carts, and asked if he had the phone.

The two started arguing, and then shoving each other before Stacy pulled out a weapon.

"The employee had a box cutter and he cut the 17 year old in the throat," said GPD Sgt. Keith Kameg. "Fortunately, they were non life threatening injures."

The young woman was treated at Shands U-F for a cut that extended from her left ear to her windpipe.

Stacy is being charged with attempted murder.

Need we mention something about every employee being a 'goodwill' ambassador? It's pretty rough when you now have to worry about contact with even the cart handlers at the nation's largest retailer.

Certainly it argues for online shopping, does it not?

Subscribe to:

Posts (Atom)