At lunch with my partner last week, we discussed why we have a long-term approach, in a market of frequent trading. We hold portfolios for months, rather than trade monthly, let alone weekly or daily. And our analysis takes into account several years of performance, in order to find consistently superior performers to buy and hold.

This market demonstrates why. Volatility is very high over short periods of time. Given the various forces and factors influencing investors- Fed rate hikes, oil and natural gas supply, Mideast oil supply worries, and, now, North Korean aggression- market prices in various equity sectors gyrate swiftly.

In my proprietary research, I found that many 3-year phenomenons are not 4 year successes. While the average returns for the market is remarkably stable over various timeframes, the standard deviations of those returns are markedly higher for relatively short time periods- less than 4 years.

In fact, some returns which are not even beyond one standard deviation from the market average return at 2 years will be well beyond that measure at 4 years. This means it is a much less rare event over a short timeframe, and a much more rare event over the longer timeframe.

Thus, the loss rate would be high for equity selections, based upon extraordinary 2-year returns. Seasoning the selections for 2, or even 1, more year, knocks out quite a few of them.

What it boils down to, from my research, is that the best way to select for consistently superior performing companies in the near future, is to find which ones have already been doing it in the past. From various prior posts on this blog, it should be evident that I do not hold out much hope for the broad mass of average employees, managers, CEOs and companies to change their behaviors and suddenly become above-average. It is much less risky to find companies which already display consistently superior performance, and simply expect a little more of it over the coming months.

Saturday, July 08, 2006

Friday, July 07, 2006

Kerkorian's GM Alliance: Almost Time for a Victory Lap

Two articles in this week's Wall Street Journal, plus extensive coverage on CNBC, have laid out what Kirk Kerkorian has planned for GM. He's aiming to engineer GM's entrance into the Carlos Goshn-run alliance of Renault and Nissan.

Holman Jenkins wrote very succinctly about exactly what is going on here, in his regular weekly WSJ column. In effect, he said, Kerkorian is prepared to offer GM to Goshn, to finally get Goshn to run the place, since he couldn't lure Goshn to GM outright.

With the added talk of GM CEO Rick Wagoner's departure, should this occur, it demonstrates that there is a more serious approach to fixing GM. Wagoner is written up as the champion of a 'slow and steady' turnaround. Goshn has credentials for having actually succeeded in a rapid, well-motivated restructuring of his car company alliance. Rather than creep along with half-measures, Goshn confronted and acknowledged the severity of his situation, and moved adroitly and quickly to save his firm from collapse.

I wrote here, here, and here, back in the fall of last year, about GM's serious likelihood of losing its corporate life, and/or its independence. I see that I gave the company until the end of the decade, whereas I thought I had predicted this end within 24 months.

In either case, while it's too early to take my victory lap now, for being right, I'll get the track shoes out and begin stretching.

Reading these prior posts I have linked above, it reminds me of how much in denial the analyst media and consulting community have been about GM's and Ford's actual peril. They all seemed to worried about angering a still-spending auto giant to do their jobs and tell the truth.

Well, now they are reporting the truth, as it happens in front of them. Rather like the brokerage firms that downgrade a stock the day after it drops 20%.

You heard a warning of the fatal condition of GM here first. Having nothing to lose, it seemed easy to me to call what I saw, and reason that GM does not have long to live as an independent auto producer. Above all else, their long-running inability to design and market cars many people will pay sufficient prices for, has doomed the company. It's simply too late for them to overcome years of bad leadership and management.

Between economic uncertainty, energy prices, and competitive pressures, GM can no longer afford even one misstep. That's just too much risk for Kerkorian to take on his substantial investment. You have to hand it to the wily old guy. He has totally outsmarted the corps of analysts and media onlookers who have been clucking at Kirk's loss of touch in the GM caper.

This past week, all I hear and read about is how Kerkorian is slyly engineering a no-premium takeover, sans proxy fight and board battle. And he's even brought allies to the table that nobody had dared consider even a month ago. Talk about insight, discipline and fortitude. Kerkorian would seem to have earned every cent he's made with his bare-knuckle investing style.

If all goes well, Kerkorian will let common sense and fiduciary duty pressure the GM board into accepting his recommendation for the three-way alliance, run by Goshn. Wagoner will depart. And my prediction about GM or Ford leaving the field of independent car makers will come true way ahead of schedule.

Holman Jenkins wrote very succinctly about exactly what is going on here, in his regular weekly WSJ column. In effect, he said, Kerkorian is prepared to offer GM to Goshn, to finally get Goshn to run the place, since he couldn't lure Goshn to GM outright.

With the added talk of GM CEO Rick Wagoner's departure, should this occur, it demonstrates that there is a more serious approach to fixing GM. Wagoner is written up as the champion of a 'slow and steady' turnaround. Goshn has credentials for having actually succeeded in a rapid, well-motivated restructuring of his car company alliance. Rather than creep along with half-measures, Goshn confronted and acknowledged the severity of his situation, and moved adroitly and quickly to save his firm from collapse.

I wrote here, here, and here, back in the fall of last year, about GM's serious likelihood of losing its corporate life, and/or its independence. I see that I gave the company until the end of the decade, whereas I thought I had predicted this end within 24 months.

In either case, while it's too early to take my victory lap now, for being right, I'll get the track shoes out and begin stretching.

Reading these prior posts I have linked above, it reminds me of how much in denial the analyst media and consulting community have been about GM's and Ford's actual peril. They all seemed to worried about angering a still-spending auto giant to do their jobs and tell the truth.

Well, now they are reporting the truth, as it happens in front of them. Rather like the brokerage firms that downgrade a stock the day after it drops 20%.

You heard a warning of the fatal condition of GM here first. Having nothing to lose, it seemed easy to me to call what I saw, and reason that GM does not have long to live as an independent auto producer. Above all else, their long-running inability to design and market cars many people will pay sufficient prices for, has doomed the company. It's simply too late for them to overcome years of bad leadership and management.

Between economic uncertainty, energy prices, and competitive pressures, GM can no longer afford even one misstep. That's just too much risk for Kerkorian to take on his substantial investment. You have to hand it to the wily old guy. He has totally outsmarted the corps of analysts and media onlookers who have been clucking at Kirk's loss of touch in the GM caper.

This past week, all I hear and read about is how Kerkorian is slyly engineering a no-premium takeover, sans proxy fight and board battle. And he's even brought allies to the table that nobody had dared consider even a month ago. Talk about insight, discipline and fortitude. Kerkorian would seem to have earned every cent he's made with his bare-knuckle investing style.

If all goes well, Kerkorian will let common sense and fiduciary duty pressure the GM board into accepting his recommendation for the three-way alliance, run by Goshn. Wagoner will depart. And my prediction about GM or Ford leaving the field of independent car makers will come true way ahead of schedule.

Thursday, July 06, 2006

Corporate Governance: Bob Nardelli's Interview on CNBC

As I write this post, I am listening to/watching Maria Bartiromo's interview with Bob Nardelli, CEO of Home Depot. Irrespective of my prior remarks about Bartiromo, she is certainly giving Nardelli a fairly "hardball" interview. To my pleasant surprise, she has asked direct questions about Nardelli's annual meeting fiasco.

As for Nardelli, his performance in the interview's opening moments is nothing short of robotic. Clearly, Home Depot hired the best public relations talent they could find to carefully script his remarks about the annual meeting. Nardelli was obviously told to "stick to the script," period. No deviations. No ad libs.

That script consisted of simply saying, to paraphrase, "We tried a new style of annual meeting. I take full responsibility. It didn't work well. We will return to our prior format next year." When Bartiromo pushed him for an answer as to why the director-less format was tried this year (and, to her credit, she actually asked, verbatim, "what were you thinking?!"), he repeated, several times, again, to paraphrase, "We are a society that likes to ask questions and blame. This is in the past. We won't do it again. We'll go back to our prior format next year." Meaning, he is not about to discuss the highly probably reason for the attempt to muzzle shareholders- his egregious pay package in the face of consistently poor shareholder returns for the 5 or so years he has run Home Depot.

As to the matter of his options, he avoided admitting the rules were changed for him, to his benefit, regarding the awarding of the options. Rather, he kept stressing that, if he doesn't get the stock price above the strike price, he receives nothing. Again, ducking the "why" and focusing on the "what if?"

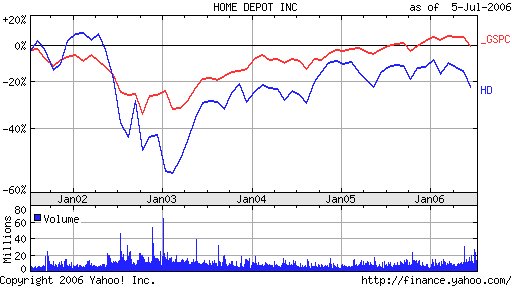

Nardelli then went on to extol his supportive board. Yes, with the compensation treatment he's gotten, what else would you expect? Further, he spoke of their patience and support for his strategy. Meaning, I guess, that he's happy they haven't noticed that, under his leadership, Home Depot's total returns have been abysmal. According to Bartiromo, the company's stock has plunged 30% during his tenure. And 20% over the last 5 years. Lowes has done much better for its shareholders over the past 5 years.

Nardelli then went on to extol his supportive board. Yes, with the compensation treatment he's gotten, what else would you expect? Further, he spoke of their patience and support for his strategy. Meaning, I guess, that he's happy they haven't noticed that, under his leadership, Home Depot's total returns have been abysmal. According to Bartiromo, the company's stock has plunged 30% during his tenure. And 20% over the last 5 years. Lowes has done much better for its shareholders over the past 5 years.

His clever attempt to dodge responsibility is to lay it on....his board of directors. According to Nardelli, since his board has continued to employ and pay him handsomely, he must be doing alright. Nevermind that, like most boards, they would be beholden to him for nomination and continued membership. Nice 'virtuous' circle for Bob and his board- not so nice for the company's owners.

In his "final remarks," as solicited by Bartiromo, Nardelli sidesteps the poor total returns, and hammers away at the fundamental financial results, and, in his opinion, the company's 'solid commitment to corporate governance.' In short, he's being paid millions of dollars, but hasn't a clue how to affect his company's performance in ways which will result in consistently superior returns for his shareholders.

It was an interesting experience to watch a very nervous CEO bob and weave his way through a minefield of negative topics without departing from his carefully rehearsed script. He simply denied that Home Depot has problems which he is capable of solving. That is, something outside of his control is responsible for all their woes.

If I were a Home Depot shareholder, I'd want a new CEO, effective immediately. If the CEO doesn't see himself as responsible for the mediocre returns of the company he leads, and has no ideas on how to affect that performance, how can the company go wrong replacing him with someone who will try to boost the company's total return performance?

As for Nardelli, his performance in the interview's opening moments is nothing short of robotic. Clearly, Home Depot hired the best public relations talent they could find to carefully script his remarks about the annual meeting. Nardelli was obviously told to "stick to the script," period. No deviations. No ad libs.

That script consisted of simply saying, to paraphrase, "We tried a new style of annual meeting. I take full responsibility. It didn't work well. We will return to our prior format next year." When Bartiromo pushed him for an answer as to why the director-less format was tried this year (and, to her credit, she actually asked, verbatim, "what were you thinking?!"), he repeated, several times, again, to paraphrase, "We are a society that likes to ask questions and blame. This is in the past. We won't do it again. We'll go back to our prior format next year." Meaning, he is not about to discuss the highly probably reason for the attempt to muzzle shareholders- his egregious pay package in the face of consistently poor shareholder returns for the 5 or so years he has run Home Depot.

As to the matter of his options, he avoided admitting the rules were changed for him, to his benefit, regarding the awarding of the options. Rather, he kept stressing that, if he doesn't get the stock price above the strike price, he receives nothing. Again, ducking the "why" and focusing on the "what if?"

Nardelli then went on to extol his supportive board. Yes, with the compensation treatment he's gotten, what else would you expect? Further, he spoke of their patience and support for his strategy. Meaning, I guess, that he's happy they haven't noticed that, under his leadership, Home Depot's total returns have been abysmal. According to Bartiromo, the company's stock has plunged 30% during his tenure. And 20% over the last 5 years. Lowes has done much better for its shareholders over the past 5 years.

Nardelli then went on to extol his supportive board. Yes, with the compensation treatment he's gotten, what else would you expect? Further, he spoke of their patience and support for his strategy. Meaning, I guess, that he's happy they haven't noticed that, under his leadership, Home Depot's total returns have been abysmal. According to Bartiromo, the company's stock has plunged 30% during his tenure. And 20% over the last 5 years. Lowes has done much better for its shareholders over the past 5 years.His clever attempt to dodge responsibility is to lay it on....his board of directors. According to Nardelli, since his board has continued to employ and pay him handsomely, he must be doing alright. Nevermind that, like most boards, they would be beholden to him for nomination and continued membership. Nice 'virtuous' circle for Bob and his board- not so nice for the company's owners.

In his "final remarks," as solicited by Bartiromo, Nardelli sidesteps the poor total returns, and hammers away at the fundamental financial results, and, in his opinion, the company's 'solid commitment to corporate governance.' In short, he's being paid millions of dollars, but hasn't a clue how to affect his company's performance in ways which will result in consistently superior returns for his shareholders.

It was an interesting experience to watch a very nervous CEO bob and weave his way through a minefield of negative topics without departing from his carefully rehearsed script. He simply denied that Home Depot has problems which he is capable of solving. That is, something outside of his control is responsible for all their woes.

If I were a Home Depot shareholder, I'd want a new CEO, effective immediately. If the CEO doesn't see himself as responsible for the mediocre returns of the company he leads, and has no ideas on how to affect that performance, how can the company go wrong replacing him with someone who will try to boost the company's total return performance?

Time Warner and AOL Give Up on Marketing Management

Time Warner's latest plans for its AOL subsidiary are curious for their abandonment of marketing management principles. As I understand the plan, they are considering giving the entire AOL package, including email, free, to anyone with a high speed connection, just like yahoo, msn, and google.

On one hand, this may seem like a recognition that AOL really offers little of value for which people will pay, when the aforementioned alternatives are available.

However, AOL does earn revenue from users, despite the alternatives. Some people probably have both- an AOL account for which they pay, and use as an ISP, as well as free email accounts with one or more of the other providers.

Is it really smart to paint all of your customers with the same brush, and offer any of them who have their own access a 100% discount on the service? Are there not any user segments who will remain with AOL on a paying basis? Since they have that $2B of annual revenue already, why prematurely and voluntarily refund much of it? Why not raise prices on the most primitive, dial-up users, and maintain prices on those who, for whatever reason, still don't move their high-speed accessed accounts elsewhere?

Thinking back to my prior post, about Wal-Mart's foray into financial services, it seems that Time Warner is taking the opposite tack. Whereas Wal-Mart focuses on how to segment its customers, and better serve them through that understanding, Time Warner seems to be going the opposite way. They just lump most of their customer base into one bucket, and give their service to those people. Whomever they are. AOL isn't even talking about, say, developing customer profiles to use in making offers of reduced priced services to those most likely to leave AOL.

I think this reinforces the view that AOL is mismanaged, and Time Warner is compounding the problem with another layer of inept management on top of the online unit.

Carl Icahn, please call home......

On one hand, this may seem like a recognition that AOL really offers little of value for which people will pay, when the aforementioned alternatives are available.

However, AOL does earn revenue from users, despite the alternatives. Some people probably have both- an AOL account for which they pay, and use as an ISP, as well as free email accounts with one or more of the other providers.

Is it really smart to paint all of your customers with the same brush, and offer any of them who have their own access a 100% discount on the service? Are there not any user segments who will remain with AOL on a paying basis? Since they have that $2B of annual revenue already, why prematurely and voluntarily refund much of it? Why not raise prices on the most primitive, dial-up users, and maintain prices on those who, for whatever reason, still don't move their high-speed accessed accounts elsewhere?

Thinking back to my prior post, about Wal-Mart's foray into financial services, it seems that Time Warner is taking the opposite tack. Whereas Wal-Mart focuses on how to segment its customers, and better serve them through that understanding, Time Warner seems to be going the opposite way. They just lump most of their customer base into one bucket, and give their service to those people. Whomever they are. AOL isn't even talking about, say, developing customer profiles to use in making offers of reduced priced services to those most likely to leave AOL.

I think this reinforces the view that AOL is mismanaged, and Time Warner is compounding the problem with another layer of inept management on top of the online unit.

Carl Icahn, please call home......

Wal-Mart's Big Financial Services Dreams

Today's Wall Street Journal contains a story about Wal-Mart's planned big push into low-end financial services. We are talking here about payroll check cashing, wiring money, and bill paying.

From reading the article, it looks like Wal-Mart, with its size and diversified business lines, will be able to offer these services at a significant discount to the prices typically charged by those vendors who prey on low-income financial services customers. Perhaps the best example is payroll check cashing. Your typical local 'service' provider will charge a user 2-3% of the face value of the check. Wal-Mart charges a maximum of $3/check. Do the math, and for a blue-collar worker who earns $20,000/year and is paid something like $650, net, every two weeks, the average current check-cashing fee is nearly $16. So Wal-Mart will be providing enormous value to low-income consumers, who also happen to be its major target market. The company noted that it also currently processes 1.5-2MM money-services transactions per week.

On first glance, I thought Wal-Mart might get tarred for this business expansion. You can just imagine some consumer advocates picketing the big-box giant, charging that it is merely jumping in to get its share of vigorish from its financially struggling customer base.

But that doesn't seem to be the case at all here. Wal-Mart's money orders cost $.46, compared with $1.30 at the US post office. The company appears to be delivering substantial value to its customers with this suite of services.

However, that said, I don't think it's going to do an awfully lot of good for Wal-Mart over the long haul. In response to charges by a spokesman for the Massachusetts Bankers Association that "Wal-Mart wants people to cash their checks in their stores so they can then make impulse purchases in the store," the company replied that only 'about 14% of people who cash checks at the store make purchases at the same time,' according to the WSJ article. That would work out to about one collateral purchase trip for every 7-8 financial service visits. In effect, 6 times per year.

And, by the way, kudos to the bankers in Massachusetts for managing to come off explicitly as a group of bloodsuckers. By saying it's ok to charge egregious fees on check cashing for poor people, but heaven forbid those people save on the fees and spend some of that extra money on real goods they can take home with them, this group appears to want a monopoly on taking advantage of the least-well off in our society. At least Wal-Mart has demonstrated that, by intervening, they will actually give these poor people real benefits that they can't get from today's banking sector.

So, essentially, what we have is the Schumpterian phenomenon of Wal-Mart weighing in to gut value-added dollars in the low-end financial services sector, in order to transfer some of that value to its customers, thereby strengthening the company's position in that segment. I don't think Wal-Mart will profit, per se, from this move. It is mostly defensive.

In fact, it kind of makes you wonder what happened to Wal-Mart's purported move, last year, upmarket. Isn't this financial service expansion at the low end going to blur that repositioning?

It seems kind of ironic to me, by the way, how things have come full circle. Back in 1974, in my very first marketing class, I learned that Sears was then earning more gross dollars of revenue on the interest in charged on customer credit card balances, than it earned on merchandise margins. Of course, in the intervening 32 years, that has been radically changed. Retailers lost the entire captive financial services business to GE and the banking sector. Now, a large, cost-effective retailer comes back in to underprice the financial service sector on low-end services, in order to build more customer loyalty and, probably, gain some extra margin/square foot of floor space.

From reading the article, it looks like Wal-Mart, with its size and diversified business lines, will be able to offer these services at a significant discount to the prices typically charged by those vendors who prey on low-income financial services customers. Perhaps the best example is payroll check cashing. Your typical local 'service' provider will charge a user 2-3% of the face value of the check. Wal-Mart charges a maximum of $3/check. Do the math, and for a blue-collar worker who earns $20,000/year and is paid something like $650, net, every two weeks, the average current check-cashing fee is nearly $16. So Wal-Mart will be providing enormous value to low-income consumers, who also happen to be its major target market. The company noted that it also currently processes 1.5-2MM money-services transactions per week.

On first glance, I thought Wal-Mart might get tarred for this business expansion. You can just imagine some consumer advocates picketing the big-box giant, charging that it is merely jumping in to get its share of vigorish from its financially struggling customer base.

But that doesn't seem to be the case at all here. Wal-Mart's money orders cost $.46, compared with $1.30 at the US post office. The company appears to be delivering substantial value to its customers with this suite of services.

However, that said, I don't think it's going to do an awfully lot of good for Wal-Mart over the long haul. In response to charges by a spokesman for the Massachusetts Bankers Association that "Wal-Mart wants people to cash their checks in their stores so they can then make impulse purchases in the store," the company replied that only 'about 14% of people who cash checks at the store make purchases at the same time,' according to the WSJ article. That would work out to about one collateral purchase trip for every 7-8 financial service visits. In effect, 6 times per year.

And, by the way, kudos to the bankers in Massachusetts for managing to come off explicitly as a group of bloodsuckers. By saying it's ok to charge egregious fees on check cashing for poor people, but heaven forbid those people save on the fees and spend some of that extra money on real goods they can take home with them, this group appears to want a monopoly on taking advantage of the least-well off in our society. At least Wal-Mart has demonstrated that, by intervening, they will actually give these poor people real benefits that they can't get from today's banking sector.

So, essentially, what we have is the Schumpterian phenomenon of Wal-Mart weighing in to gut value-added dollars in the low-end financial services sector, in order to transfer some of that value to its customers, thereby strengthening the company's position in that segment. I don't think Wal-Mart will profit, per se, from this move. It is mostly defensive.

In fact, it kind of makes you wonder what happened to Wal-Mart's purported move, last year, upmarket. Isn't this financial service expansion at the low end going to blur that repositioning?

It seems kind of ironic to me, by the way, how things have come full circle. Back in 1974, in my very first marketing class, I learned that Sears was then earning more gross dollars of revenue on the interest in charged on customer credit card balances, than it earned on merchandise margins. Of course, in the intervening 32 years, that has been radically changed. Retailers lost the entire captive financial services business to GE and the banking sector. Now, a large, cost-effective retailer comes back in to underprice the financial service sector on low-end services, in order to build more customer loyalty and, probably, gain some extra margin/square foot of floor space.

More on Corporate Governance: Executive Compensation Continues to Rise

The Wall Street Journal recently used the occasion of Pfizer's annual meeting to run yet another piece about exorbitant CEO compensation packages. Carol Hymowitz wrote a very nice piece detailing the realities of this problem.

When asked to defend Pfizer CEO Hank McKinnell's compensation, Dana Mead, head of the board's compsenation committee, did so by saying, '....Mr. McKinnell's pay was based on market forces and reflected his responsibility overseeing 110,000 employees."

The article notes that "disgruntled shareholders even tried to unseat Mr. Mead and another director this past April but failed."

What is irksome to me is that Mr. Mead didn't say something like, "Mr. McKinnell has the responsibility to earn above-average total returns for you shareholders. In hopes of attracting talented leaders to be our company's CEO, and make that happen, we need to offer a competitive compensation package. If Mr. McKinnell proves unable to meet this responsibility, he will be replaced with someone in whom we, your board members, feel is better-equipped to carry out this responsibility."

Ms. Hymowitz quotes Lucian Bebchuk, a Harvard University law professor, who notes that the board is beholden to the CEO for their membership and, thus, pretty much have to repay him/her with bloated compensation packages, and that "they don't have an incentive to change those arrangements."

Well, that really says it all, doesn't it? You have a board charged with CEO oversight, but who nominates the board? The CEO. Wonderful! I guess having no board is marginally more corrupt, but, judging by modern CEO compensation and corporate total return performances, not by much.

Though the article closes with comments on the competition for good CEOs as the reason for excessive compensation packages, I have my doubts about that. Look at corporate performance, and you'll see that very few CEOs seem to be able to achieve consistently superior returns for their shareholders. It should be fairly easy to design a CEO compensation package with the predominant proportion of it structured as variable, and payable upon attainment of consistently superior returns for the shareholders. That way, shareholders only pay for the performance. As I have written elsewhere on this blog, why would you want a CEO who doesn't think s/he can do this in the first place?

When asked to defend Pfizer CEO Hank McKinnell's compensation, Dana Mead, head of the board's compsenation committee, did so by saying, '....Mr. McKinnell's pay was based on market forces and reflected his responsibility overseeing 110,000 employees."

The article notes that "disgruntled shareholders even tried to unseat Mr. Mead and another director this past April but failed."

What is irksome to me is that Mr. Mead didn't say something like, "Mr. McKinnell has the responsibility to earn above-average total returns for you shareholders. In hopes of attracting talented leaders to be our company's CEO, and make that happen, we need to offer a competitive compensation package. If Mr. McKinnell proves unable to meet this responsibility, he will be replaced with someone in whom we, your board members, feel is better-equipped to carry out this responsibility."

Ms. Hymowitz quotes Lucian Bebchuk, a Harvard University law professor, who notes that the board is beholden to the CEO for their membership and, thus, pretty much have to repay him/her with bloated compensation packages, and that "they don't have an incentive to change those arrangements."

Well, that really says it all, doesn't it? You have a board charged with CEO oversight, but who nominates the board? The CEO. Wonderful! I guess having no board is marginally more corrupt, but, judging by modern CEO compensation and corporate total return performances, not by much.

Though the article closes with comments on the competition for good CEOs as the reason for excessive compensation packages, I have my doubts about that. Look at corporate performance, and you'll see that very few CEOs seem to be able to achieve consistently superior returns for their shareholders. It should be fairly easy to design a CEO compensation package with the predominant proportion of it structured as variable, and payable upon attainment of consistently superior returns for the shareholders. That way, shareholders only pay for the performance. As I have written elsewhere on this blog, why would you want a CEO who doesn't think s/he can do this in the first place?

Sunday, July 02, 2006

Ford & GM: Recent Developments

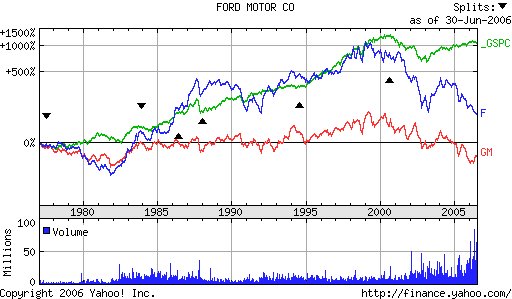

Ford and GM's recent developments were the subject of a short piece in this week's Wall Street Journal. The author of the piece only went back to January of this year to issue his opinion. His verdict was that GM is in better shape for a "turnaround" because of outside pressure from Kerkorian, while Ford's two-class stock structure kept its value from rising due to the founding family's insulation from common investors. His conclusion is that Ford is less market-sensitive, due to the Ford family's near-controlling 40% voting stake in the firm.

I find this a touch myopic, as the longterm Yahoo chart above shows. Comparing the S&P500, GM and Ford since 1979, it puts the lie to the notion that Ford has typically been slow to respond to market forces, due to the Ford family's control of the firm. Sure, in 2006, GM has displayed a better shareholder return than that of Ford. No question about that. Just not being in Chapter 11 yet is probably a big boost for GM.

However, if you look carefully at the chart above, it continues to echo what I discussed in a recent post about these two firms. While Ford's voting structure may shield it somewhat from market forces, it still has outperformed GM over the past quarter century. And by a rather handsome margin, as GM has been negative, while Ford looks to have returned something in the neighborhood (interpolating on the chart above) of 100%. The S&P returned roughly 1000% over the period.

That Ford had some significant "up" periods, from the early 1980s to 2000, suggests that they were, in fact, quite sensitive to shareholder returns. GM, by contrast, rarely broke out of a flat return curve, save for a few years in the late 1990s.

My point is that, due to an unnecessarily short analytical time horizon, the WSJ has summarily judged Ford to be too insular to save now. While GM, through the mixed blessing of attracting Kirk Kerkorian, and his lieutenant, Jerry York's advice to find a global partner, has temporarily surged ahead of the former in total return terms.

I don't necessarily believe Bill Ford is turning, or will turn around Ford. His "way forward" seems "way too optimistic," in my opinion. If only because the management team that got you to where Ford is now, is unlikely to take you somewhere else, as a shareholder. But the company is sensitive to market pressures all on its own.

I don't think GM is more "investor sensitive." Instead, it has to deal with a veteran value shopper, in Kerkorian. As the WSJ, as well as CNBC, articulated, what's good for GM shareholders, the prospect of a partial rescue in the form of some global tie-up with the likes of Nissan, is probably not good for CEO Wagoner. If anything, Wagoner put GM where it is today through his learned insensitivity to market forces, as a result of a long tenure at the stumbling auto giant.

Yes, GM may well have marginally brighter prospects for its shareholders. But don't attribute GM's idiosyncratic fortune to Ford's share voting structure. Ford is in trouble due to inept management that has tried to grapple with global pressures on an aged, badly-led competitor. Not due to an unwillingness to acknowledge the problem.

YouTube Comes Out of the Garage

YouTube must be nearing a significant milestone of some sort. The Wall Street Journal mentioned it in two different pieces in the last two weeks.

One piece covered a multitude of approaches being developed to provide video from the web to the home. YouTube doesn't address the last few feet, from the cable to the TV. But it is far and away the most visited video website, according to the WSJ's article.

What is remarkable about YouTube is that you can see it visibly following in the footsteps of Microsoft, eBay, Yahoo and Google. It was fashioned as a personal solution to a problem- sharing large video files between friends and acquaintances.

It's now become larger, gotten VC funding ($3.5MM from Sequoia), hired a Yahoo veteran to build their sales team, and begun to explore longer-term profitability models linked to their core service.

Along the way, commenting on these points, and the huge traffic YouTube boasts ( 3 million videos viewed daily, as of Dec. 15, 2005), the Journal pointed out that the two founders, literally in the apocryphal garage, had out-innovated a host of existing, large media companies ( e.g., see my recent post on moribund Time Warner). Now, several large media corporations are rumored to be sniffing around YouTube, looking to acquire it.

It's truly gratifying to see this type of company develop as it has. For me, it maintains and nourishes my faith in enterprises which begin with keen consumer behavioral insights and a savvy, gritty sense of implementation. Rather than oozing forth from the likes of Disney or Time Warner, this type of high-energy, edgy operation springs up from virtually "nowhere." Mainstream media firms would probably bog down over the copyright issues that YouTube has from user-posted content that is inappropriately published, resulting in their legal departments becoming profit centers due to bizarre time and cost-allocation methods. Instead, YouTube deals with these matter with alacrity, gently letting its popularity and 'cool' image persuade some of the larger copyright holders to look for ways to work together, rather than try to stomp YouTube out of existence.

I have no idea where these two guys and their firm will end up. But it's a lot of fun, and instructional, to watch them rip through the electronic media world, successfully meeting needs and attracting customers, while overpaid suits in the suites of a variety of larger competitors sit and stare at their coming downfall. I have to believe that Joseph Schumpeter would be extremely proud and not at all surprised to see YouTube rocketing across the online video publishing sky, threatening established vendors across the media sector.

One piece covered a multitude of approaches being developed to provide video from the web to the home. YouTube doesn't address the last few feet, from the cable to the TV. But it is far and away the most visited video website, according to the WSJ's article.

What is remarkable about YouTube is that you can see it visibly following in the footsteps of Microsoft, eBay, Yahoo and Google. It was fashioned as a personal solution to a problem- sharing large video files between friends and acquaintances.

It's now become larger, gotten VC funding ($3.5MM from Sequoia), hired a Yahoo veteran to build their sales team, and begun to explore longer-term profitability models linked to their core service.

Along the way, commenting on these points, and the huge traffic YouTube boasts ( 3 million videos viewed daily, as of Dec. 15, 2005), the Journal pointed out that the two founders, literally in the apocryphal garage, had out-innovated a host of existing, large media companies ( e.g., see my recent post on moribund Time Warner). Now, several large media corporations are rumored to be sniffing around YouTube, looking to acquire it.

It's truly gratifying to see this type of company develop as it has. For me, it maintains and nourishes my faith in enterprises which begin with keen consumer behavioral insights and a savvy, gritty sense of implementation. Rather than oozing forth from the likes of Disney or Time Warner, this type of high-energy, edgy operation springs up from virtually "nowhere." Mainstream media firms would probably bog down over the copyright issues that YouTube has from user-posted content that is inappropriately published, resulting in their legal departments becoming profit centers due to bizarre time and cost-allocation methods. Instead, YouTube deals with these matter with alacrity, gently letting its popularity and 'cool' image persuade some of the larger copyright holders to look for ways to work together, rather than try to stomp YouTube out of existence.

I have no idea where these two guys and their firm will end up. But it's a lot of fun, and instructional, to watch them rip through the electronic media world, successfully meeting needs and attracting customers, while overpaid suits in the suites of a variety of larger competitors sit and stare at their coming downfall. I have to believe that Joseph Schumpeter would be extremely proud and not at all surprised to see YouTube rocketing across the online video publishing sky, threatening established vendors across the media sector.

Subscribe to:

Posts (Atom)