Lest you think corporate America has become too hard on employees....too unforgiving and impatient......consider its treatment of one Charles Prince. I'm referring to CitiGroup CEO/Chairman Chuck Prince, of course.

In this post, late last month, I discussed CitiGroup's situation vis a vis BofA. Many media pundits were all a-twitter that the latter was about, and apparently did, overtake the former in terms of market value.

However, as I pointed out in that piece, the important measure to observe is consistent total return. In the charts contained in that post, you will see how Prince has steered CitiGroup into a dead-calm pool of a virtually flat, that is to say, zero, total return for his tenure as the firm's CEO and Chairman.

Now, such dismal performance might, you would think, merit dismissal. How many line VPs or SVPs of a major money-center bank would still be in their jobs, if they failed, for three straight years, to achieve their objectives? While their competitors outperformed them?

Not many, I'd wager. But, it's different for CEOs. First, they get paid a lot more, regardless of their inadequate performance for years at a time.

Mr. Prince's FY2005 compensation is detailed here, courtesy of Forbes Magazine. According to Forbes, with confirming information from Reuters, here, Prince was paid roughly $13MM in 'direct,' cash-like compensation last year, and an additional $10MM in various options and longer-term compensation.

Second, CEOs get a lot more time to perform. Prince has been CEO at CitiGroup for three years, and COO for two years prior to that. Word was, after the company's recent analysts meeting this week, that Prince has 'only another year' to 'fix things.'

Wow, that's pressure, eh? Only four years, at something north of $13MM cash compensation per year, to mismanage one of the nation's largest banks.

Where does the line form to replace him, come next January?

The way I figure it, with Prince's lack of operating background, and four-year record of failure, the requirements for the job should be pretty minimal. Nearly anyone, apparently, can satisfy Citi's board as competent to lead the banking firm.

Wouldn't you volunteer to risk your career in order to get a shot at $50-100MM in total compensation over four years, knowing termination after year four is the penalty?

Life at the top is tough, friends.....very, very tough indeed.

NOT!

Friday, December 15, 2006

Thursday, December 14, 2006

David Geffen's Bad News for Hank Greenberg, Jack Welch & Co. : It's Not About The Money

Two weeks ago, I wrote this post regarding Hank Greenberg's activity in pursuit of the New York Times Company. In that piece, I noted Jack Welch's pursuit, with a group of other investors, of the Boston Globe.

Now comes some bad news from a seriously creative, wealthy businessman. In last Friday's Wall Street Journal's article about him, Geffen admitted to wanting to build "a pre-eminent newspaper."

Further, he is quoted in the article as saying,

"It's difficult starting a business from scratch....The next thing I do, I want to buy rather than start from scratch....As a guy who is committed to, certainly by the time I die, giving everything I have a way, that gives me an awful lot of latitude about what I can and can't do."

According to Forbes' 2005 survey, Mr. Geffen is ranked #117 on the list of the world's richest people, with a net worth of approximately $4.4B. Hank Greenberg was #170, with an estimated net worth of $3.2B. That may now overstate Greenberg's net worth, as his resignation from AIG in mid-2005 may have resulted in his loss of significant assets. Jack Welch was #376, with an estimated net worth of $680MM, as of the Forbes 2001 survey, but is no longer on the list in 2005. Perhaps the result of his expensive, very public divorce from his second wife earlier in this decade.

Viewed from this perspective, Geffen has the deepest pockets, with Greenberg coming next. While Welch and his syndicate can doubtless borrow to buy the Boston Globe from the New York Times, Greenberg's interest in the parent may complicate, or may simplify, their pursuit of the ailing newspaper.

It's perhaps noteworthy that Geffen, somewhat an impressario of artistic talent, created the largest economic fortune of the three. Less of a classic businessman than the other two, his objective of building a "pre-eminent" newspaper should probably be chilling news to Greenberg and Welch. Geffen clearly has no compunction about pouring as much of his net worth into the effort as necessary.

I doubt Welch is that altruistic. Given Greenberg's maneuvering vis a vis his financial interests in AIG, I think he's more like Welch than he is like Geffen. For either of these former corporate types, with their smaller kitties, to engage in new-era newspaper-building combat with Geffen might well lead to their financial ruin.

Geffen's comments can't be good news for Welch. What will the lenders at (JP Morgan) Chase, to whom Welch has gone for financing, now think about bankrolling the least-well-funded entrant in a game in which the best-funded player has already announced he's willing to lose it all to reach his objective? Given Geffen's rather iconoclastic approaches to his work, he may well have some innovative ideas for reviving newspapers that the other two ex-CEOs can't even imagine.

This will be an interesting area to watch in 2007.

Now comes some bad news from a seriously creative, wealthy businessman. In last Friday's Wall Street Journal's article about him, Geffen admitted to wanting to build "a pre-eminent newspaper."

Further, he is quoted in the article as saying,

"It's difficult starting a business from scratch....The next thing I do, I want to buy rather than start from scratch....As a guy who is committed to, certainly by the time I die, giving everything I have a way, that gives me an awful lot of latitude about what I can and can't do."

According to Forbes' 2005 survey, Mr. Geffen is ranked #117 on the list of the world's richest people, with a net worth of approximately $4.4B. Hank Greenberg was #170, with an estimated net worth of $3.2B. That may now overstate Greenberg's net worth, as his resignation from AIG in mid-2005 may have resulted in his loss of significant assets. Jack Welch was #376, with an estimated net worth of $680MM, as of the Forbes 2001 survey, but is no longer on the list in 2005. Perhaps the result of his expensive, very public divorce from his second wife earlier in this decade.

Viewed from this perspective, Geffen has the deepest pockets, with Greenberg coming next. While Welch and his syndicate can doubtless borrow to buy the Boston Globe from the New York Times, Greenberg's interest in the parent may complicate, or may simplify, their pursuit of the ailing newspaper.

It's perhaps noteworthy that Geffen, somewhat an impressario of artistic talent, created the largest economic fortune of the three. Less of a classic businessman than the other two, his objective of building a "pre-eminent" newspaper should probably be chilling news to Greenberg and Welch. Geffen clearly has no compunction about pouring as much of his net worth into the effort as necessary.

I doubt Welch is that altruistic. Given Greenberg's maneuvering vis a vis his financial interests in AIG, I think he's more like Welch than he is like Geffen. For either of these former corporate types, with their smaller kitties, to engage in new-era newspaper-building combat with Geffen might well lead to their financial ruin.

Geffen's comments can't be good news for Welch. What will the lenders at (JP Morgan) Chase, to whom Welch has gone for financing, now think about bankrolling the least-well-funded entrant in a game in which the best-funded player has already announced he's willing to lose it all to reach his objective? Given Geffen's rather iconoclastic approaches to his work, he may well have some innovative ideas for reviving newspapers that the other two ex-CEOs can't even imagine.

This will be an interesting area to watch in 2007.

Wednesday, December 13, 2006

GE's Immelt: Still Underperforming and Still Making Excuses

The video of this morning's appearance by GE Chairman and CEO Jeff Immelt on CNBC can be viewed here .

It runs about 8+ minutes. However, of particular interest to me was the segment at roughly minute 4:30 into the interview. This is where Joe Kernen of CNBC's Squawk Box program, asks Immelt, his ultimate boss, about why GE, as a conglomerate, is valuable.

Immelt rather brazenly says that GE exists 'because the market lets it exist,' or something like that. You can hear the exact quote for yourself at the video link. In defending the conglomeration, Immelt mentions, "performance" and 'common culture, goals....'

Then, to deflect attention from his own failure as CEO to beat the S&P, he now espouses '10-15-20 year' timeframes for the company, insisting that this is how "we view the company."

In other words, Immelt in effect pleads,

'let's all hail the golden past era of Jack Welch, and please overlook the sub-S&P500 performance over the entire tenure of my CEO- and Chairmanship of GE.'

To see what GE's total return performance has been under Immelt, take a look at the table in this blog post which I wrote earlier today.

Then Immelt plays the 'oughta, shoulda' game. He says that GE stock "should" go up with oil. Darn those stupid investors, eh? Why can't they price his stock right. It's soooo embarrassing!

As if this theatre isn't comic enough, you have to step back and see what CNBC is asking veteran reporters Becky Quick and Joe Kernen to do. They must, with straight faces, lob softballs at their Chairman in a live interview.

Am I the only person who thinks this is ludicrous and demeaning to Quick and Kernen? Does anyone seriously believe either veteran, capable, sane CNBC/GE online anchor will risk her/his career by being candid and hardnosed with their employer's Chairman and CEO on live network TV?

Does anyone seriously believe either will engage in the following hypothetical Q&A?

Quick: Hey, Jeff.....about our total return since you took over from Jack Welch. Why haven't you been able to beat the S&P500 in 4 out of 5 years? And why has our stock underperformed for the period during which you've been CEO?

Immelt: Good point, Becky. I'm recommending to the board today that they fire me and find someone to run the firm who can actually outperform the returns that my shareholders could get from simply buying a passively-managed S&P500 index fund. I can't, in good conscience, recommend that anybody assume the risk inherent in holding GE as a specific equity, when I've failed to return to shareholders what they could get with such an index fund holding.

Kernen: Hey, Jeff.....about this conglomerate we fondly call "GE." With the annual revenues and asset sizes of our disparate and unrelated businesses, don't you think the corporate function is essentially exacting a non-value-adding tax to pay your enormous salary, benefits and bonuses? Wouldn't investors benefit from spinning GE into its five separate businesses, each with its own listed stock, free of the financial yoke of your corporate functions?

Immelt: I'm glad you pointed that out, Joe. Yes, I think you are right. On second thought, I'll recommend to the board that they dismiss me as soon as I've split the firm into its trimmer, more enterprising separate components. I think I've demonstrated, over the five years I've been CEO, that my staff and I have actually destroyed value, not added any, for shareholders. Please help to stop me before I grab even more shareholder value for myself by underperforming the S&P and getting paid many tens of millions of dollars for it.

Quick: Wow, Jeff. Thanks for that breaking news on GE splitting itself up. You heard it first, here, on CNBC. America's Business News Network.

Immelt: Thank you, Becky and Joe. I'm just glad I can finally confess to being unable to create any consistently superior total returns for my shareholders after five years of being paid tens of millions of dollars to attempt the task. Now, I can retire and join Jack Welch in bidding for an old newspaper up Boston way. Nobody expects it to earn good returns for the shareholders, and it'll be a private equity buyout, so there won't really even be a publicly-available total return to worry about- so I think I'll be well-suited to that......

Well, I can dream, can't I? CNBC is more about entertainment than truth or news. This hypothetical exchange will never occur. However, you can vist my prior posts here, here, and here, to read more material supporting the comments in the hypothetical Q&A above.

As I've written before, though, if such an exchange did occur, now.....that would be news. Not to mention real hardball financial business reporting.

It runs about 8+ minutes. However, of particular interest to me was the segment at roughly minute 4:30 into the interview. This is where Joe Kernen of CNBC's Squawk Box program, asks Immelt, his ultimate boss, about why GE, as a conglomerate, is valuable.

Immelt rather brazenly says that GE exists 'because the market lets it exist,' or something like that. You can hear the exact quote for yourself at the video link. In defending the conglomeration, Immelt mentions, "performance" and 'common culture, goals....'

Then, to deflect attention from his own failure as CEO to beat the S&P, he now espouses '10-15-20 year' timeframes for the company, insisting that this is how "we view the company."

In other words, Immelt in effect pleads,

'let's all hail the golden past era of Jack Welch, and please overlook the sub-S&P500 performance over the entire tenure of my CEO- and Chairmanship of GE.'

To see what GE's total return performance has been under Immelt, take a look at the table in this blog post which I wrote earlier today.

Then Immelt plays the 'oughta, shoulda' game. He says that GE stock "should" go up with oil. Darn those stupid investors, eh? Why can't they price his stock right. It's soooo embarrassing!

As if this theatre isn't comic enough, you have to step back and see what CNBC is asking veteran reporters Becky Quick and Joe Kernen to do. They must, with straight faces, lob softballs at their Chairman in a live interview.

Am I the only person who thinks this is ludicrous and demeaning to Quick and Kernen? Does anyone seriously believe either veteran, capable, sane CNBC/GE online anchor will risk her/his career by being candid and hardnosed with their employer's Chairman and CEO on live network TV?

Does anyone seriously believe either will engage in the following hypothetical Q&A?

Quick: Hey, Jeff.....about our total return since you took over from Jack Welch. Why haven't you been able to beat the S&P500 in 4 out of 5 years? And why has our stock underperformed for the period during which you've been CEO?

Immelt: Good point, Becky. I'm recommending to the board today that they fire me and find someone to run the firm who can actually outperform the returns that my shareholders could get from simply buying a passively-managed S&P500 index fund. I can't, in good conscience, recommend that anybody assume the risk inherent in holding GE as a specific equity, when I've failed to return to shareholders what they could get with such an index fund holding.

Kernen: Hey, Jeff.....about this conglomerate we fondly call "GE." With the annual revenues and asset sizes of our disparate and unrelated businesses, don't you think the corporate function is essentially exacting a non-value-adding tax to pay your enormous salary, benefits and bonuses? Wouldn't investors benefit from spinning GE into its five separate businesses, each with its own listed stock, free of the financial yoke of your corporate functions?

Immelt: I'm glad you pointed that out, Joe. Yes, I think you are right. On second thought, I'll recommend to the board that they dismiss me as soon as I've split the firm into its trimmer, more enterprising separate components. I think I've demonstrated, over the five years I've been CEO, that my staff and I have actually destroyed value, not added any, for shareholders. Please help to stop me before I grab even more shareholder value for myself by underperforming the S&P and getting paid many tens of millions of dollars for it.

Quick: Wow, Jeff. Thanks for that breaking news on GE splitting itself up. You heard it first, here, on CNBC. America's Business News Network.

Immelt: Thank you, Becky and Joe. I'm just glad I can finally confess to being unable to create any consistently superior total returns for my shareholders after five years of being paid tens of millions of dollars to attempt the task. Now, I can retire and join Jack Welch in bidding for an old newspaper up Boston way. Nobody expects it to earn good returns for the shareholders, and it'll be a private equity buyout, so there won't really even be a publicly-available total return to worry about- so I think I'll be well-suited to that......

Well, I can dream, can't I? CNBC is more about entertainment than truth or news. This hypothetical exchange will never occur. However, you can vist my prior posts here, here, and here, to read more material supporting the comments in the hypothetical Q&A above.

As I've written before, though, if such an exchange did occur, now.....that would be news. Not to mention real hardball financial business reporting.

McGraw-Hill Makes PRA's Portfolio Selection List

I'm pleased to note that McGraw-Hill is in my (Performance Research Associates) equity portfolio selections this month. As I wrote here, recently, I found that the company's total return performance would merit inclusion, but, ironically, I thought it's occasional bursts of accelerating revenue growth would make it too inconsistent for my portfolio.

It just goes to show that you should trust the numbers, not subjective judgment. When my December selections were completed, McGraw-Hill was among the low-growth component of the portfolio.

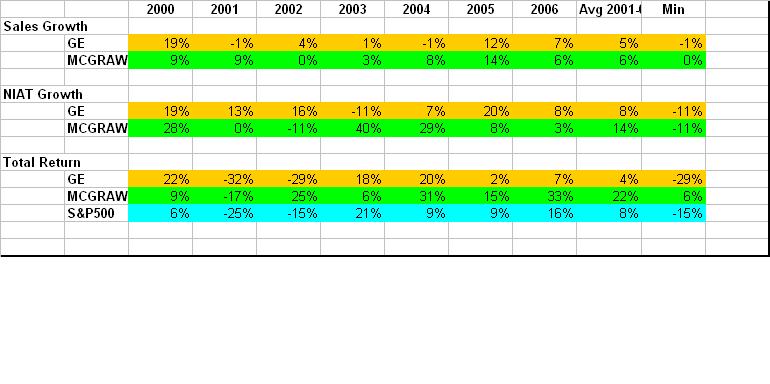

I remain impressed with Terry McGraw's feat. I've repasted my analysis of McGraw-Hill and GE from last month nearby (please click on the table to see a larger version), to provide the reader with recent revenue and NIAT growth, and total return data, for the former.

I remain impressed with Terry McGraw's feat. I've repasted my analysis of McGraw-Hill and GE from last month nearby (please click on the table to see a larger version), to provide the reader with recent revenue and NIAT growth, and total return data, for the former.

Managing to wring such consistent revenue and profit growth out of this collection of rather modest businesses is noteworthy.

It just goes to show that you should trust the numbers, not subjective judgment. When my December selections were completed, McGraw-Hill was among the low-growth component of the portfolio.

I remain impressed with Terry McGraw's feat. I've repasted my analysis of McGraw-Hill and GE from last month nearby (please click on the table to see a larger version), to provide the reader with recent revenue and NIAT growth, and total return data, for the former.

I remain impressed with Terry McGraw's feat. I've repasted my analysis of McGraw-Hill and GE from last month nearby (please click on the table to see a larger version), to provide the reader with recent revenue and NIAT growth, and total return data, for the former.Managing to wring such consistent revenue and profit growth out of this collection of rather modest businesses is noteworthy.

Tuesday, December 12, 2006

Wal-Mart's Latest Gaffe: Julie Roehm's Dismissal

Yesterday's Wall Street Journal carried a feature story describing, in more detail, the events leading up to the dismissal of Julie Roehm, Wal-Mart's recently hired SVP of Marketing Communications.

Without repeating the details of that piece, nor the one preceding it over the weekend in the Journal, I'll just state that Ms. Roehm seems to be the latest victim of the giant retailer's management ineptitude.

From the article's recounting of her product development and marketing background, Ms. Roehm seems to be the genuine article, when it comes to getting results with fresh marketing communications approaches. Wal-Mart hired her to support their ill-fated entry into upscale retail merchandise earlier this year.

As my partner suggests, and I agree, it looks like Lee Scott is trying to eliminate any trace of the personnel who remind him of the mistaken strategy. Not that Roehm was its architect. She simply came in to execute according to the product strategy playbook they gave her. Julie Roehm may have helped, but, frankly, I've never felt that good promotional efforts can overcome weak product and marketing strategies.

The entire ad agency firing flap seems to be a smokescreen as well. More effort to erase all external traces of the retailer's attempted dalliance with upscale consumers.

More than anything, sadly, I think this episodes reinforces the strategic mismanagement of Wal-Mart over the past few years. The accompanying stock price chart for Wal-Mart and the S&P500, from Yahoo's site, indicates how badly the firm has stalled this past year.

More than anything, sadly, I think this episodes reinforces the strategic mismanagement of Wal-Mart over the past few years. The accompanying stock price chart for Wal-Mart and the S&P500, from Yahoo's site, indicates how badly the firm has stalled this past year.

Wal-Mart is simply striking out as it attempts to cope with the limits to its revenue and profit growth. It had a successful model, before saturating the appropriate areas of the US with its stores. Perhaps it will find more success overseas, although it recently retrenched in at least one foreign country. But I don't think the source of Wal-Mart's stock's return to a path of consistently superior total returns lies with its current product and marketing strategies.

Without repeating the details of that piece, nor the one preceding it over the weekend in the Journal, I'll just state that Ms. Roehm seems to be the latest victim of the giant retailer's management ineptitude.

From the article's recounting of her product development and marketing background, Ms. Roehm seems to be the genuine article, when it comes to getting results with fresh marketing communications approaches. Wal-Mart hired her to support their ill-fated entry into upscale retail merchandise earlier this year.

As my partner suggests, and I agree, it looks like Lee Scott is trying to eliminate any trace of the personnel who remind him of the mistaken strategy. Not that Roehm was its architect. She simply came in to execute according to the product strategy playbook they gave her. Julie Roehm may have helped, but, frankly, I've never felt that good promotional efforts can overcome weak product and marketing strategies.

The entire ad agency firing flap seems to be a smokescreen as well. More effort to erase all external traces of the retailer's attempted dalliance with upscale consumers.

More than anything, sadly, I think this episodes reinforces the strategic mismanagement of Wal-Mart over the past few years. The accompanying stock price chart for Wal-Mart and the S&P500, from Yahoo's site, indicates how badly the firm has stalled this past year.

More than anything, sadly, I think this episodes reinforces the strategic mismanagement of Wal-Mart over the past few years. The accompanying stock price chart for Wal-Mart and the S&P500, from Yahoo's site, indicates how badly the firm has stalled this past year.Wal-Mart is simply striking out as it attempts to cope with the limits to its revenue and profit growth. It had a successful model, before saturating the appropriate areas of the US with its stores. Perhaps it will find more success overseas, although it recently retrenched in at least one foreign country. But I don't think the source of Wal-Mart's stock's return to a path of consistently superior total returns lies with its current product and marketing strategies.

Fidelity's New Research Payment Approach

Friday's Wall Street Journal's Money section featured an article about how some fund managements are changing the manner in which they compensate brokers for so-called "research." In the wake of the notorious Spitzer settlement years ago, after the dot-com bust, research is now supposed to be independent beyond question.

Thus, soft dollar arrangements are becoming more heavily scrutinized. This practice involves the fund agreeing to trade with a broker in payment for 'research.' The effect may be to charge clients more for the trades, while the management gets 'free' research. Nice trick, eh?

Fidelity Investments is mentioned at the end of the piece as departing significantly from all other firms in fixing this situation. They have begun to sign deals

"in which Fidelity Management & Research- which oversees the funds- pays for research instead of fund investors. Fidelity negotiated flat rates for the research and for the commission rates on the trading- a move known as "unbundling." "

I love this. Of course, no other major fund management firms are joining this practice. It would reduce their profits by shifting the costs of 'research' to them from the customers' trading expenses.

To me, the Fidelity move makes perfect sense. Despite Spitzer's "best" efforts, research can never really be 'independent.' There is always the potential for an asset manager to somehow compensate an 'independent researcher' to provide beneficial reports on companies whose equity or debt the manager holds in funds. Moving the source of conflict of interest a little further down the food chain will never remove it entirely.

However, research properly belongs as an expense of the fund management in providing asset management services to clients. To the extent that it really has any material benefit in the first place. If it had, don't you think investment banks would have charged their other functions, and customers, for the product of the research departments?

As one of my investment banking colleagues puts it, 'why not just call it "marketing," since that's what "research" really is.' That is, it becomes a crutch which managers use to justify their selections, if they are not sufficiently confident to simply accept responsibility for them in the first place.

Still, Fidelity's move at least puts the customer first, and makes Fidelity sure it wants the research it uses, because it's paying cash for the service.

Thus, soft dollar arrangements are becoming more heavily scrutinized. This practice involves the fund agreeing to trade with a broker in payment for 'research.' The effect may be to charge clients more for the trades, while the management gets 'free' research. Nice trick, eh?

Fidelity Investments is mentioned at the end of the piece as departing significantly from all other firms in fixing this situation. They have begun to sign deals

"in which Fidelity Management & Research- which oversees the funds- pays for research instead of fund investors. Fidelity negotiated flat rates for the research and for the commission rates on the trading- a move known as "unbundling." "

I love this. Of course, no other major fund management firms are joining this practice. It would reduce their profits by shifting the costs of 'research' to them from the customers' trading expenses.

To me, the Fidelity move makes perfect sense. Despite Spitzer's "best" efforts, research can never really be 'independent.' There is always the potential for an asset manager to somehow compensate an 'independent researcher' to provide beneficial reports on companies whose equity or debt the manager holds in funds. Moving the source of conflict of interest a little further down the food chain will never remove it entirely.

However, research properly belongs as an expense of the fund management in providing asset management services to clients. To the extent that it really has any material benefit in the first place. If it had, don't you think investment banks would have charged their other functions, and customers, for the product of the research departments?

As one of my investment banking colleagues puts it, 'why not just call it "marketing," since that's what "research" really is.' That is, it becomes a crutch which managers use to justify their selections, if they are not sufficiently confident to simply accept responsibility for them in the first place.

Still, Fidelity's move at least puts the customer first, and makes Fidelity sure it wants the research it uses, because it's paying cash for the service.

Monday, December 11, 2006

Another Financial Utility? BofA & Barclays

My friend and sometimes-colleague, B, emailed me today regarding this recent post about the market values of BofA and CitiGroup.

I failed, in that post, to reiterate that B had predicted this state of events as long ago as 1996- ten years ago. In a phone conversation at the time, so vivid in my mind that I can still recall where I was sitting during it, B foresaw the merger of the major US banks into no more than three super-sized financial utilities. He predicted that they would re-integrate all of the business lines previously spun off or weakened by decades of mediocrity- mortgage banking, credit cards, investment banking, etc.

In that respect, he is the clearest-seeing and perhaps best strategic mind with which I am acquainted.

He further opined, once again correctly, that they would not fare well in terms of total returns. He has mused, and we discussed, how much better it might be for the banks to simply cede simple deposit business to some governmental agency, in order to remove the safety of that business from association with the riskiness of the modern, integrated financial utilities.

Specifically, he wrote to me this morning (because his identity is concealed, and the passage is not unduly specific, I doubt he will mind my quoting from it),

"Remember my model projected that the huge financial supermarkets would resemble large government organizations lacking innovative spirits and laden with beaureaucratic activities. Their size and lack of a usable collective gray matter harnessed to the business is rapidly assuring that this will happen. Ultimately, perhaps the behemoth banks will become government regulated utilities, with at least the benefit of not compensating their senior executives as though they were being rewarded for taking the business-required personal risks that goes with productive innovation."

Now, as if things aren't sufficiently mediocre, we have this rumor concerning BofA and Barclays merging. Talk about cultural clashes!

I'm sure the pundits and investment bankers are all salivating at the prospect of two large, non-overlapping financial institutions being wedded for enormous attendant transaction and advisory fees. To what end? Does anyone truly think that such a combination is likely to earn consistently superior returns for the integrated entity?

As I write this, I am listening to CNBC's coverage of Citigroup's ineffectual solution to its performance problems. A new COO has been named, but Chairman Chuck Prince is being left "in charge," if that is the right term for describing his tenure.

Blogger is, once again, being uncooperative in pasting in stock price charts. However, if you look at Barclays, Chase, BofA, CitiGroup, and the S&P for the past 2 and 5 years, you will see that the pack of financial supertankers move together, with Citi being the worst-performing. I note this by way of refuting what Larry Kudlow just proclaimed, which is that BofA and Chase are now 'coming on strong.' In truth, as my friend B prophesied, they all move pretty much in lockstep, because they are all pretty much identically-structured and managed companies now.

Another merger? Sure, why not. The year 2006 is going down in history as a mega-deal sort of year. Why not end it with another one?

I failed, in that post, to reiterate that B had predicted this state of events as long ago as 1996- ten years ago. In a phone conversation at the time, so vivid in my mind that I can still recall where I was sitting during it, B foresaw the merger of the major US banks into no more than three super-sized financial utilities. He predicted that they would re-integrate all of the business lines previously spun off or weakened by decades of mediocrity- mortgage banking, credit cards, investment banking, etc.

In that respect, he is the clearest-seeing and perhaps best strategic mind with which I am acquainted.

He further opined, once again correctly, that they would not fare well in terms of total returns. He has mused, and we discussed, how much better it might be for the banks to simply cede simple deposit business to some governmental agency, in order to remove the safety of that business from association with the riskiness of the modern, integrated financial utilities.

Specifically, he wrote to me this morning (because his identity is concealed, and the passage is not unduly specific, I doubt he will mind my quoting from it),

"Remember my model projected that the huge financial supermarkets would resemble large government organizations lacking innovative spirits and laden with beaureaucratic activities. Their size and lack of a usable collective gray matter harnessed to the business is rapidly assuring that this will happen. Ultimately, perhaps the behemoth banks will become government regulated utilities, with at least the benefit of not compensating their senior executives as though they were being rewarded for taking the business-required personal risks that goes with productive innovation."

Now, as if things aren't sufficiently mediocre, we have this rumor concerning BofA and Barclays merging. Talk about cultural clashes!

I'm sure the pundits and investment bankers are all salivating at the prospect of two large, non-overlapping financial institutions being wedded for enormous attendant transaction and advisory fees. To what end? Does anyone truly think that such a combination is likely to earn consistently superior returns for the integrated entity?

As I write this, I am listening to CNBC's coverage of Citigroup's ineffectual solution to its performance problems. A new COO has been named, but Chairman Chuck Prince is being left "in charge," if that is the right term for describing his tenure.

Blogger is, once again, being uncooperative in pasting in stock price charts. However, if you look at Barclays, Chase, BofA, CitiGroup, and the S&P for the past 2 and 5 years, you will see that the pack of financial supertankers move together, with Citi being the worst-performing. I note this by way of refuting what Larry Kudlow just proclaimed, which is that BofA and Chase are now 'coming on strong.' In truth, as my friend B prophesied, they all move pretty much in lockstep, because they are all pretty much identically-structured and managed companies now.

Another merger? Sure, why not. The year 2006 is going down in history as a mega-deal sort of year. Why not end it with another one?

Whistle-Blowing at Fannie Mae

Last Thursday's Wall Street Journal recounted the saga of an ex-Fannie Mae manager, Thomas Inman. He believes he is a 'whistle-blower,' reporting his former employer's failure to acknowledge his findings of accounting inaccuracies.

The company, however, has a different story. Several other employees explained that Inman 'uncovered' some items which were already known. Furthermore, it appears that these other items were the focus of other teams, not the one to which Inman was tasked.

It's impossible to tell from the article who is right, Fannie Mae or Inman. However, Inman was dismissed from the company after just six months. Again, it's hard to tell who is telling the truth, or, perhaps, the truth as they see it, even from this.

What struck me about this story was how familiar it is. Haven't we all known someone in a company in which we worked who seemed to be a bit too passionate and concerned about areas with which they were only tangentially involved? People who seemed to be on a crusade about something, even if it wasn't their actual job? Maybe even losing focus on their assigned responsibilities?

That's always the case, it seems, with whistleblowers. They might be telling the truth, and publicizing something their employer would rather conceal. Then again, they might be the occasional O/C employee who simply will not listen to reason, accept reality, and focus on their own job.

It's probably Fannie Mae's problems which occurred under the shameful watch of Frank Raines, that have brought this story to the Journal's pages. Anything hinting of further coverup at the image-impaired mortgage lender now gets attention.

Still, to me, something seems odd about Inman's tale. With several other Fannie Mae employees, including the General Counsel, going on record to assert that Inman is wrong, I am inclined to doubt the ex-employee. It's not just a faceless spokesperson stonewalling questions about Inman's allegation. Some fairly detailed counterpoints were mentioned in the article.

It ought to remind us that sometimes, the lone employee crying "wolf" is, in fact, one of those we have met elsewhere, continually seeing conspiracy and fraud in other corporate functions and processes.

The company, however, has a different story. Several other employees explained that Inman 'uncovered' some items which were already known. Furthermore, it appears that these other items were the focus of other teams, not the one to which Inman was tasked.

It's impossible to tell from the article who is right, Fannie Mae or Inman. However, Inman was dismissed from the company after just six months. Again, it's hard to tell who is telling the truth, or, perhaps, the truth as they see it, even from this.

What struck me about this story was how familiar it is. Haven't we all known someone in a company in which we worked who seemed to be a bit too passionate and concerned about areas with which they were only tangentially involved? People who seemed to be on a crusade about something, even if it wasn't their actual job? Maybe even losing focus on their assigned responsibilities?

That's always the case, it seems, with whistleblowers. They might be telling the truth, and publicizing something their employer would rather conceal. Then again, they might be the occasional O/C employee who simply will not listen to reason, accept reality, and focus on their own job.

It's probably Fannie Mae's problems which occurred under the shameful watch of Frank Raines, that have brought this story to the Journal's pages. Anything hinting of further coverup at the image-impaired mortgage lender now gets attention.

Still, to me, something seems odd about Inman's tale. With several other Fannie Mae employees, including the General Counsel, going on record to assert that Inman is wrong, I am inclined to doubt the ex-employee. It's not just a faceless spokesperson stonewalling questions about Inman's allegation. Some fairly detailed counterpoints were mentioned in the article.

It ought to remind us that sometimes, the lone employee crying "wolf" is, in fact, one of those we have met elsewhere, continually seeing conspiracy and fraud in other corporate functions and processes.

Subscribe to:

Posts (Atom)