Today I have two Wall Street-oriented topics to address. One involves the recent fervor over whether the Dow will post a new all-time high. The other is about a recent article in the Wall Street Journal regarding 'catchy' ticker symbols.

My puzzlement over the Dow level revolves around the mistaken impression by so many analysts, market observers and pundits, that the precise level of a composite index matters over so long a time, to individual investors.

Among the more bone-headed, indefensible comments uttered in the last few days is that, now that the Dow may rise above its prior high, some unnamed investors, who apparently had their prior holdings frozen in time, will promptly unload all of their holdings, to finally book a gain.

Run that one by me again, please? Just because the Dow hasn't risen above its prior high of some 5-6 years ago has no relationship with how each individual equity, or even mutual funds, performed. Let alone what investors did with those positions.

Is it reasonable to believe that most investors have been hanging onto the same portfolio they owned 5 years ago? That's the only way that a new Dow high would actually unleash a flood of sell orders to finally rescue distressed equities that were underwater all of this time.

It just seems too absurdly foolish for anyone to think this way, but Mark Hanes and several others articulated just that view in the past few days.

A composite index is, admittedly, a function of its component parts. In the case of the Dow, that's only 30 industrials. So what about, say, the other 470 that are part of the S&P500 (I haven't checked, but I'm reasonably sure the Dow is a proper subset of the S&P), let alone the other 3000+ equities with liquidity in the market these days?

That's why I think the exact level of the Dow or S&P is mostly moot. Rather, the rate of change of an index is more useful in suggesting how investors may react, as they view a steady, or unsteady, progression of monthly returns of "the market," as narrowly represented by the Dow, or, more broadly, by the S&P500.

The other financial topic which caught my eye this week appeared in yesterday's WSJ. Entitled, "Does Stock by Any Other Name Smell as Sweet," it cited 'research' purporting that certain stock tickers, simply by virtue of their 'name,' cause, or are associated with, higher average returns, than other stock tickers.

The tickers in question, such as YUM, HOG, BID, and EYE, are thought to trigger more awareness in investors' minds. According to the article, researchers Adam Aiter and Daniel Oppenheimer claim to have found that pronounceable tickers which were bought and held on their first day of trading earned $85.35 more, on a $1,000 portfolio, than other tickers. Further, Pomona College's Gary Smith alleges that portfolios formed from "clever" tickers, from 1984 to 2004, had a return of 23.6%, against 12.3% for a 'hypothetical index of all NYSE and Nasdaq stocks.'

In neither case does the article mention average returns, or standard deviations, or the significance level of the stated performance differences.

What's more, both 'studies' suffer from a more glaring error. By using only one predictive variable, and measuring the difference in returns, or stock prices, they implicitly assign all performance differences, or their variances, to the stock ticker 'pronounceability' or 'cleverness' variable.

Does anyone truly believe this? Would you drop all of your other equity strategies right now, and invest in one of these two?

More reasonable would be a study in which the authors included a set of commonly-used predictive variables, and the stock ticker variable. Then the variance in performance of stocks, or portfolios, could be allocated to each predictive variable, or the predictive variables themselves could be factor analyzed, to assess shared association.

Either, or both, of these approaches would yield more believable, defensible, and useful conclusions to the question of whether the 'cuteness' of a stock ticker actually adds to its return potential.

It's disappointing to me that the Journal even printed this piece, let alone without much in the way of critical commentary on them. It did include one remark by an obscure finance professor from the University of Utah, who did at least suggest controlling for, rather than actually assessing the predictive power of, other predictive variables.

After all that, the article concludes by noting that the researchers themselves do not "recommend that people make trading decisions based on our findings."

What, then, was the point of this piece? Just entertainment? That would seem to be the Personal Section, would it not?

Have a great weekend!

Friday, September 29, 2006

Thursday, September 28, 2006

Today's Dow Frenzy

Dow closed 33.74 points shy of a record yesterday.

Now, every financial media personality is crowing that a new Dow high is within reach. As if that really matters.

CNBC's resident (endlessly) talking head, Bob Pisani, went over the top, explaining that this new high is crucial for investor confidence.

Well, I think he's only very partially right. This year is already seeing a positive Dow and S&P. And, by the way, it's the S&P which has the largest fund presence, so that is the index which would really matter. But it is not anywhere near as close to an all-time high as the Dow is.

It's not clear that a new high, whether on a close, or intra-day, really matters as much as steady, quarterly positive returns for the index.

But, leaving these behavioral questions aside, I see that, as usual, the on-air media is back to personifying "the market." I wrote about this last June, here.

This morning, CNBC rolled out the moss-backed Art Cashen, a floor-based executive of one of the Street's brokerage firms, and caught NYSE CEO John Thain in passing, to solicit comments calculated to heighten the drama of whether or not a new intra-day Dow high would be made.

If anything demonstrates to what degree media coverage of the capital markets is more about entertainment than reasoned assistance to investors, today's sorry spectacle would be it.

More Automotive Developments: Toyota, GM and Nissan

The automotive sector is once again in the news this week.

A Wall Street Journal article earlier this week reported on the self-parking Lexus LS460. Toyota, its developer, demonstrated this amazing technology in a parking garage 'within sight of Ford's Dearborn headquarters'.

The story made, in my opinion, several key points.

One was the story of the crystal headlight glass. Evoking the attention to detail that was involved in the legendary development, over 20 years ago, of the original Sony Walkman portable cassette player, the car's chief engineer painstakingly redesigned the headlights to more accurately resemble fine crystal. To do so, he actually had a crystal headlight made, then sent this to the supplier in order to be sure the latter had the exact "look" desired, from which to manufacture the production-grade headlights for actual assembly.

Second, Toyota is now enjoying, and employing, the accruing benefits of success, including internal funding for growth. The article mentions many measures of Toyota's recent success: profits, size, hiring plans, etc. Suffice to say, their attention to consumer tastes, desires, and the fulfillment of those, has driven it past Ford and GM in terms of profitability and recent growth rates.

It should have. That's how markets are supposed to work.

The Journal story's ending comment is noteworthy. It comments on Toyota's continuing 'inferiority complex.'

To quote the piece, "Unlike baseball pennant races, contests for sales and dominance in the (auto) industry never end."

That's entirely right. Joseph Schumpeter taught us that "the race" never ends- anywhere, anytime. Thus my search for consistently superior performance, which, in a well-run, well-positioned company, can be the resulting hallmark of this healthy inferiority complex of Toyota's.

Next, we have yesterday's and today's coverage of the Paris alliance talks between Carlos Ghosn of Nissan, and Rick Wagoner of GM.

Between the WSJ piece yesterday, and this morning's continuing coverage on CNBC, it's evident that, for better or for worse, Rick Wagoner is rolling the dice now, with all of GM's shareholders' money on the line.

Personally, I find it laughable that anyone can call this year, based upon such brief and one-off events, a "turnaround" for GM. The chart on the left is what traders, analysts, and CNBC talking heads are all excited about right now. Over the past three and six months, GM's stock price is easily outperforming that of the S&P500.

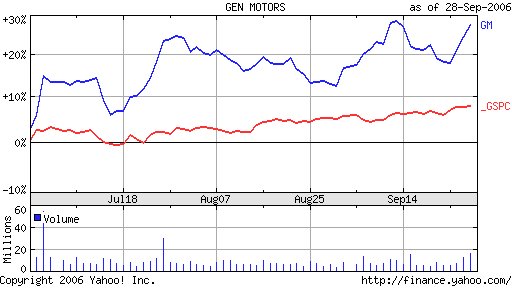

Personally, I find it laughable that anyone can call this year, based upon such brief and one-off events, a "turnaround" for GM. The chart on the left is what traders, analysts, and CNBC talking heads are all excited about right now. Over the past three and six months, GM's stock price is easily outperforming that of the S&P500.

This, we are told, is the result of investors believing that GM is now in turnaround mode, and will return to automotive dominance imminently.

This, we are told, is the result of investors believing that GM is now in turnaround mode, and will return to automotive dominance imminently.

Not so fast....

Here's what the charts look like for the past one and two years. Completely different, aren't they? GM is flat for the past twelve months, and down for the past two years.

Here's what the charts look like for the past one and two years. Completely different, aren't they? GM is flat for the past twelve months, and down for the past two years.

Now I read, and hear, that GM's CEO is feeling so confident of his brief, one-time trick of shedding some labor costs, that he's decided to demand tribute from Carlos Ghosn and Nissan/Renault, should the two form an alliance. According to the Journal, GM wants a "multibillion-dollar payment" from Nissan and Renault.

Wagoner is really a clever guy- give him that. He doesn't want this alliance. It was forced upon him by Jerry York and Kirk Kerkorian, his newest and most irksome board member and shareowner. How to evade the alliance? Loudly proclaim that a non-sales, non-customer-based, one-time financial cost reduction is, in reality, the much-heralded "turnaround," and then use that "fact" in order to make an unacceptable demand as a condition of any alliance with Nissan and Renault.

Wagoner is really a clever guy- give him that. He doesn't want this alliance. It was forced upon him by Jerry York and Kirk Kerkorian, his newest and most irksome board member and shareowner. How to evade the alliance? Loudly proclaim that a non-sales, non-customer-based, one-time financial cost reduction is, in reality, the much-heralded "turnaround," and then use that "fact" in order to make an unacceptable demand as a condition of any alliance with Nissan and Renault.

Yesterday's Wall Street Journal front-page piece, and this morning's coverage of the situation by CNBC, both cast doubt on the likelihood of any alliance being consummated. The most recent word is that the two parties have agreed to go away and reconsider terms, etc, for the weeks remaining in their 90-day alliance evaluation period which ends on October 15.

So Rick Wagoner is now "all in" with his shareholders' money. The Nissan/Renault alliance probably marks the last refueling stop on GM's uncertain road to recovery. If Wagoner successfully derails the alliance, then his shareholders better pray he has more up his sleeve than more job and cost cuts. And maybe Wagoner better check his own liability insurance for coverage from gigantic shareholder lawsuits for fiduciary breach.

Back to Toyota, though. Because that company figures in the GM alliance talks, too. According to Ghosn, Toyota is the company to beat, and he wants this alliance in order to have a decent chance of surviving that juggernaut's impending rise to global automotive dominance. Being a game of momentum and scale, Ghosn realizes that his companies have to be able to stay the course with enough capacity and design capability to match the Japanese giant, stride for stride, going forward.

Clearly, Ghosn isn't sure he has enough resources to do it presently. But GM may be demanding too high a price, and for an alliance that Ghosn doesn't even seem, based on his comments this summer, will even work effectively.

Once again, we see Schumpeter's theories in action. Wagoner is playing in his little Detroit fishbowl, and just wants Nissan/Renault, and Ghosn, to go away. Maybe to Dearborn, maybe back to Tennessee. Yet, GM can't really demonstrate a full-fledged, customer-based resurgence in its own fortunes at this time, nor, really, a very highly-probable scenario in the near future, either.

Ghosn, on the other hand, is running scared. Which is a good thing. He's competent, tough, and now, scared. Just like Toyota, his main adversary for the coming, pre-Chinese automotive sector rise, decade. That kind of healthy fear transforms companies into nimble, fleet customer-needs-serving, consistently superior total return performers. Not always, but it helps.

So now we have the lay of the land, in the microcosm of two of this week's automotive sector stories. Toyota demonstrates why it's the company to fear in the sector. Nissan's Ghosn demonstrates why he's the best bet for challenging Toyota globally. GM's Wagoner demonstrates that he's more interested in being left alone, to the potential detriment of his shareholders. And Ford is desperately hoping that maybe Ghosn will come back to call on them, and let them at least fight on the number two team, rather than alone, against Toyota.

A Wall Street Journal article earlier this week reported on the self-parking Lexus LS460. Toyota, its developer, demonstrated this amazing technology in a parking garage 'within sight of Ford's Dearborn headquarters'.

The story made, in my opinion, several key points.

One was the story of the crystal headlight glass. Evoking the attention to detail that was involved in the legendary development, over 20 years ago, of the original Sony Walkman portable cassette player, the car's chief engineer painstakingly redesigned the headlights to more accurately resemble fine crystal. To do so, he actually had a crystal headlight made, then sent this to the supplier in order to be sure the latter had the exact "look" desired, from which to manufacture the production-grade headlights for actual assembly.

Second, Toyota is now enjoying, and employing, the accruing benefits of success, including internal funding for growth. The article mentions many measures of Toyota's recent success: profits, size, hiring plans, etc. Suffice to say, their attention to consumer tastes, desires, and the fulfillment of those, has driven it past Ford and GM in terms of profitability and recent growth rates.

It should have. That's how markets are supposed to work.

The Journal story's ending comment is noteworthy. It comments on Toyota's continuing 'inferiority complex.'

To quote the piece, "Unlike baseball pennant races, contests for sales and dominance in the (auto) industry never end."

That's entirely right. Joseph Schumpeter taught us that "the race" never ends- anywhere, anytime. Thus my search for consistently superior performance, which, in a well-run, well-positioned company, can be the resulting hallmark of this healthy inferiority complex of Toyota's.

Next, we have yesterday's and today's coverage of the Paris alliance talks between Carlos Ghosn of Nissan, and Rick Wagoner of GM.

Between the WSJ piece yesterday, and this morning's continuing coverage on CNBC, it's evident that, for better or for worse, Rick Wagoner is rolling the dice now, with all of GM's shareholders' money on the line.

Personally, I find it laughable that anyone can call this year, based upon such brief and one-off events, a "turnaround" for GM. The chart on the left is what traders, analysts, and CNBC talking heads are all excited about right now. Over the past three and six months, GM's stock price is easily outperforming that of the S&P500.

Personally, I find it laughable that anyone can call this year, based upon such brief and one-off events, a "turnaround" for GM. The chart on the left is what traders, analysts, and CNBC talking heads are all excited about right now. Over the past three and six months, GM's stock price is easily outperforming that of the S&P500. This, we are told, is the result of investors believing that GM is now in turnaround mode, and will return to automotive dominance imminently.

This, we are told, is the result of investors believing that GM is now in turnaround mode, and will return to automotive dominance imminently.Not so fast....

Here's what the charts look like for the past one and two years. Completely different, aren't they? GM is flat for the past twelve months, and down for the past two years.

Here's what the charts look like for the past one and two years. Completely different, aren't they? GM is flat for the past twelve months, and down for the past two years.Now I read, and hear, that GM's CEO is feeling so confident of his brief, one-time trick of shedding some labor costs, that he's decided to demand tribute from Carlos Ghosn and Nissan/Renault, should the two form an alliance. According to the Journal, GM wants a "multibillion-dollar payment" from Nissan and Renault.

Wagoner is really a clever guy- give him that. He doesn't want this alliance. It was forced upon him by Jerry York and Kirk Kerkorian, his newest and most irksome board member and shareowner. How to evade the alliance? Loudly proclaim that a non-sales, non-customer-based, one-time financial cost reduction is, in reality, the much-heralded "turnaround," and then use that "fact" in order to make an unacceptable demand as a condition of any alliance with Nissan and Renault.

Wagoner is really a clever guy- give him that. He doesn't want this alliance. It was forced upon him by Jerry York and Kirk Kerkorian, his newest and most irksome board member and shareowner. How to evade the alliance? Loudly proclaim that a non-sales, non-customer-based, one-time financial cost reduction is, in reality, the much-heralded "turnaround," and then use that "fact" in order to make an unacceptable demand as a condition of any alliance with Nissan and Renault.Yesterday's Wall Street Journal front-page piece, and this morning's coverage of the situation by CNBC, both cast doubt on the likelihood of any alliance being consummated. The most recent word is that the two parties have agreed to go away and reconsider terms, etc, for the weeks remaining in their 90-day alliance evaluation period which ends on October 15.

So Rick Wagoner is now "all in" with his shareholders' money. The Nissan/Renault alliance probably marks the last refueling stop on GM's uncertain road to recovery. If Wagoner successfully derails the alliance, then his shareholders better pray he has more up his sleeve than more job and cost cuts. And maybe Wagoner better check his own liability insurance for coverage from gigantic shareholder lawsuits for fiduciary breach.

Back to Toyota, though. Because that company figures in the GM alliance talks, too. According to Ghosn, Toyota is the company to beat, and he wants this alliance in order to have a decent chance of surviving that juggernaut's impending rise to global automotive dominance. Being a game of momentum and scale, Ghosn realizes that his companies have to be able to stay the course with enough capacity and design capability to match the Japanese giant, stride for stride, going forward.

Clearly, Ghosn isn't sure he has enough resources to do it presently. But GM may be demanding too high a price, and for an alliance that Ghosn doesn't even seem, based on his comments this summer, will even work effectively.

Once again, we see Schumpeter's theories in action. Wagoner is playing in his little Detroit fishbowl, and just wants Nissan/Renault, and Ghosn, to go away. Maybe to Dearborn, maybe back to Tennessee. Yet, GM can't really demonstrate a full-fledged, customer-based resurgence in its own fortunes at this time, nor, really, a very highly-probable scenario in the near future, either.

Ghosn, on the other hand, is running scared. Which is a good thing. He's competent, tough, and now, scared. Just like Toyota, his main adversary for the coming, pre-Chinese automotive sector rise, decade. That kind of healthy fear transforms companies into nimble, fleet customer-needs-serving, consistently superior total return performers. Not always, but it helps.

So now we have the lay of the land, in the microcosm of two of this week's automotive sector stories. Toyota demonstrates why it's the company to fear in the sector. Nissan's Ghosn demonstrates why he's the best bet for challenging Toyota globally. GM's Wagoner demonstrates that he's more interested in being left alone, to the potential detriment of his shareholders. And Ford is desperately hoping that maybe Ghosn will come back to call on them, and let them at least fight on the number two team, rather than alone, against Toyota.

Wednesday, September 27, 2006

More on Media from the Goldman Conference: Old vs. New

Last week’s Goldman Sach’s media investors’ conference was the subject of a recent Charles Schwab daily market email, to which I subscribe.

In part, it read,

“Investors could be forgiven for wondering if they had stepped into the wrong conference on Tuesday. Old media executives talked up digital strategies even as YAHOO warned of an unforeseen advertising shortfall. It appeared that old and new media companies had swapped roles for a day. While many blue chips slipped on Tuesday, a handful of media stocks rose after top executives at WALT DISNEY CO., VIACOM INC. and TIME WARNER INC. declared at the conference commitments to exploit the Internet to serve viewers anywhere, on any device. Meanwhile, Yahoo Inc. watched its shares fall after disclosing that two key advertising segments, autos and financial services, were weaker than expected. The panic selling of Yahoo appeared to do little to shake the resolve of media executives, some of whom once considered the Internet little more than an interesting sideshow. What's up for one-time Internet-skeptic NEWS CORP. next year? "To continue to drive into the digital transformation," Chief Executive Rupert Murdoch told investors. Murdoch's own stock on Wall Street has surged after buying one of the fastest growing Internet properties, MySpace.com, last year. Disney CEO Bob Iger took the opportunity to reveal it had sold $1 million of movie downloads on APPLE COMPUTER INC.'s iTunes in just a week.”

It does seem ironic that the “old” media companies are scrambling pell-mell to secure outlets for their aging content libraries, while the “new” media Yahoo was visibly weakened during the conference.

However, I don’t think Yahoo’s experience holds any import for the clutch of old media firms. As I have written here recently, Yahoo is probably the weakest of the “new” media firms, if you can rightly call it that. It doesn’t really offer content, what it does offer is mostly for free, and it isn’t really distribution, either.

Rather, what does not surprise me is that TimeWarner, Disney, Viacom and News Corp are frantically trying to sell or lease their video and audio content before it becomes eclipsed by the potential all-online production and distribution model.

Consider the prospect, in the current online environment, of some hot TV producers and rising new stars on YouTube going directly to consumers online with new films. It’s not as far-fetched as it may at first seem. Right now, on YouTube, one can view smart, interesting videos with great production values, running to more than 10 minutes. From there, it’s not a huge step into feature-length films. All it will take is some promotion on a YouTube channel, a URL, provision to take payments using PayPal, and broadcast and theaters have become disintermediated. A few years of this, and the content libraries of those old media titans will begin to be barren of recent goods, and only have aging stock gathering cyberdust.

Of all the old media names, I would hypothesize TimeWarner may be in the most precarious situation, this week’s analysts’ upgrades notwithstanding. As an owner of significant distribution and content assets, nobody trusts it. Other distributors can’t be assured of continued access to TW content. Other content providers worry that they will be locked out of, or given inferior access/terms, on TW’s cable systems. No company has managed consistently superior total return performance as an integrated media distribution and content firm yet. I doubt TimeWarner’s going to be the exception.

Add to this Apple’s impending release of iTV, about which I wrote here, and the downfall of old media becomes more likely. With an easy method of downloading new, online-marketed content from URL to PC, then, wirelessly to the Apple-provided, or one of its competitor’s, servers, and then via wires to consumers’ living room TVs, broadcast’s weakness becomes more glaring.

It’s really…well…entertaining, to watch the media sector change almost quarterly, as old media hurries to extract some value for its content, while new media distribution races ahead by allowing anyone to produce and market content, bypassing traditional media.

Dare I write, “stay tuned?”

In part, it read,

“Investors could be forgiven for wondering if they had stepped into the wrong conference on Tuesday. Old media executives talked up digital strategies even as YAHOO warned of an unforeseen advertising shortfall. It appeared that old and new media companies had swapped roles for a day. While many blue chips slipped on Tuesday, a handful of media stocks rose after top executives at WALT DISNEY CO., VIACOM INC. and TIME WARNER INC. declared at the conference commitments to exploit the Internet to serve viewers anywhere, on any device. Meanwhile, Yahoo Inc. watched its shares fall after disclosing that two key advertising segments, autos and financial services, were weaker than expected. The panic selling of Yahoo appeared to do little to shake the resolve of media executives, some of whom once considered the Internet little more than an interesting sideshow. What's up for one-time Internet-skeptic NEWS CORP. next year? "To continue to drive into the digital transformation," Chief Executive Rupert Murdoch told investors. Murdoch's own stock on Wall Street has surged after buying one of the fastest growing Internet properties, MySpace.com, last year. Disney CEO Bob Iger took the opportunity to reveal it had sold $1 million of movie downloads on APPLE COMPUTER INC.'s iTunes in just a week.”

It does seem ironic that the “old” media companies are scrambling pell-mell to secure outlets for their aging content libraries, while the “new” media Yahoo was visibly weakened during the conference.

However, I don’t think Yahoo’s experience holds any import for the clutch of old media firms. As I have written here recently, Yahoo is probably the weakest of the “new” media firms, if you can rightly call it that. It doesn’t really offer content, what it does offer is mostly for free, and it isn’t really distribution, either.

Rather, what does not surprise me is that TimeWarner, Disney, Viacom and News Corp are frantically trying to sell or lease their video and audio content before it becomes eclipsed by the potential all-online production and distribution model.

Consider the prospect, in the current online environment, of some hot TV producers and rising new stars on YouTube going directly to consumers online with new films. It’s not as far-fetched as it may at first seem. Right now, on YouTube, one can view smart, interesting videos with great production values, running to more than 10 minutes. From there, it’s not a huge step into feature-length films. All it will take is some promotion on a YouTube channel, a URL, provision to take payments using PayPal, and broadcast and theaters have become disintermediated. A few years of this, and the content libraries of those old media titans will begin to be barren of recent goods, and only have aging stock gathering cyberdust.

Of all the old media names, I would hypothesize TimeWarner may be in the most precarious situation, this week’s analysts’ upgrades notwithstanding. As an owner of significant distribution and content assets, nobody trusts it. Other distributors can’t be assured of continued access to TW content. Other content providers worry that they will be locked out of, or given inferior access/terms, on TW’s cable systems. No company has managed consistently superior total return performance as an integrated media distribution and content firm yet. I doubt TimeWarner’s going to be the exception.

Add to this Apple’s impending release of iTV, about which I wrote here, and the downfall of old media becomes more likely. With an easy method of downloading new, online-marketed content from URL to PC, then, wirelessly to the Apple-provided, or one of its competitor’s, servers, and then via wires to consumers’ living room TVs, broadcast’s weakness becomes more glaring.

It’s really…well…entertaining, to watch the media sector change almost quarterly, as old media hurries to extract some value for its content, while new media distribution races ahead by allowing anyone to produce and market content, bypassing traditional media.

Dare I write, “stay tuned?”

Tuesday, September 26, 2006

Immelt's Five Year Anniversary As GE CEO

On September 11th, The Wall Street Journal ran a celebratory piece on Jeff Immelt's five-year anniversary as GE's CEO.

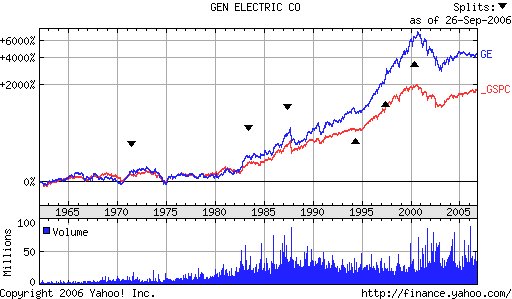

The Yahoo-sourced chart on the left depicts how Immelt's reign compares with those of prior CEOs of the company (Phillippe, Borch, Jones, Welch) going back to the early 1960s.

It's fair to say that long timeline charts such as this one can downplay earlier rough spots, since the end periods tend to have magnified appearances. For instance, the late-80s drop in stock price, coinciding with the 'crash' of 1987, is significant for its time, but pales in comparison to the absolute drop of the last few years.

That being the case, here's a five-year view of the same information, corresponding to Immelt's tenure as CEO.

That being the case, here's a five-year view of the same information, corresponding to Immelt's tenure as CEO.It seems to me that the WSJ is giving Immelt, and GE, the kid glove treatment. Maybe it's because of the fear of loss of GE's advertising revenues, and access to future stories.

However, looking at this Yahoo chart, it's difficult to understand how an industrial conglomerate can have underperformed the S&P500 through these particular last five years, and not be seen as needing to be led by someone else, or simply broken up.

Ask yourself this question:

If GE did not exist today, would someone create it as it currently exists?

I think the answer would almost certainly be, "no." What possible value would investors see in a TV network and movie studio buying: a jet engine business, a locomotive business, a financial services business, and power generation systems businesses, to name a few. There's absolutely no business synergies whatsoever that are unique to these businesses.

As I wrote here early last month, there is no longer any apparent value to the constituent business units of GE being assembled as GE.

Rather than observe the data I did in my earlier piece, the Journal contained quotes like this one, from Immelt's lieutenant, Bob Wright, vice chairman and head of GE's entertainment sector,

"He's in a good dynamic for a guy who has a lot of weight on his shoulders."

Does anybody reading this understand that sentence? Maybe Wright meant this,

"He's making a heckuva lot of money for a guy who has a lot of weight on his shoulders from not delivering for his shareholders."

Toward the end of the article, we perhaps get a clue as to why Immelt's GE is foundering so badly. The Journal relates that Immelt "urges employees to make bigger bets without fearing for their jobs if they fail." "Make it personal," the piece quotes GE's CEO as saying.

So now we have the 'kinder, gentler,' GE in evidence. Maybe Immelt figures, if he is kind to his employees, and forgives lack of performance, or consistently poor investment judgment, his board will do the same for him. Seems to be working, right?

In the end, all of Immelt's changes are not affecting the company's total returns. He can globalize the behemoth, ask his managers to take more risks, and even shuffle businesses in and out of the GE portfolio.

But in the end, over five years, Immelt simply has failed to lead GE to consistently superior performance, while raking in a royal compensation, as I noted here, back in March. In that post, I observed that Immelt has already received at least $21MM in cash compensation for failing to create consistently superior total returns for his shareholders. There's no way he needs to take the risks evidently necessary to make GE's long-term performance superior to the S&P's.

Furthermore, why give up this multi-million dollar gravy train and break the company up?

In this era of concern over "corporate governance," I'm frankly disappointed that the Wall Street Journal gave Immelt such an easy pass while reviewing his first five years at the helm of GE.

A year ago, I wrote, prior to almost any well-known pundit or industry analyst, that Ford and GM were in major trouble. Especially Ford. Back then, I opined that maybe the old media and investment banking giants weren't being candid, because the slowly-dying auto giants still paid a lot of bills for companies in those sectors.

I wonder if the same thing is occurring now, with GE. The truth would be very, perhaps too, costly to the media and financial service sectors, wouldn't it?

Monday, September 25, 2006

Retail Notes

I read two interesting pieces recently in the Wall Street Journal regarding retail commerce.

On Thursday, the paper's Marketplace section reported how widely flat-panel TV retailing has spread. Companies as diverse as Office Depot, Home Depot, Costco and Kohl's have jumped into the fray. Until now, conventional local TV retailers, and big box electronics outlets like Circuit City and BestBuy have been responsible for much of the sales volume of flat-panel TVs.

As prices for the new TVs fall, and larger models hit price points below $2,000, low-price retailers such as Wal-Mart and Costco are becoming a larger part of the retailing market.

It's not surprising that so many retailers are drawn to an almost-sure thing- the rise in popularity, as prices fall, of flat-panel television. Of course, if these companies do realize tremendous sales growth from the products, then, at some point, they face a dilemma in replacing that sales growth, or lapsing back into slower-growth modes. And that type of pattern typically keeps companies from earning consistently superior total returns over a number of years.

With so many retailers entering this product/market, it suggests that the production capacities for these TVs, probably in the Far East, must be very large. It doesn't require a lot of thought to envision some pretty vicious retail price competition, as a flood of flat-panel models pour into the US market in the next few years.

On another retail topic, today's Journal catalogued a number of states and municipalities which are passing, or have passed, anti-Wal-Mart legislation.

The Journal piece quotes Boston's Mayor, Thomas Menino, as saying,

"They don't pay wages that are sufficient. Their benefit structure is poor. I don't need employers like that in our city."

Interesting that a public official feels comfortable prohibiting citizens from choosing to work for Wal-Mart, or the company for risking its own capital in opening a store in the Boston area. So much for individual liberty in terms of choosing employment options in Boston.

However, a company that has engendered this type of reaction across the country can't be in great shape. Many municipalities seem to be restricting or prohibiting Wal-Mart's entry in order to protect their locally-owned businesses.

As I wrote here, and here, recently, Wal-Mart is already tampering with the branding and positioning strategies which brought it such success over the past two decades.

These cases of governmental hostility to the company's expansion plans would seem to add more challenges to Wal-Mart's already-full plate. According to the Journal's piece, the company's sales growth has slowed below double-digits recently, after decades in the that range. Same-store sales growth is a third of what it was in 1990.

The company is targeting urban areas, finally, for its next growth spurt. But it doesn't look like that's going to be happening.

Which corresponds with what I wrote here last fall. I just don't see the company continuing its past successes in terms of both fundamental growth and consistently superior total returns for its shareholders.

On Thursday, the paper's Marketplace section reported how widely flat-panel TV retailing has spread. Companies as diverse as Office Depot, Home Depot, Costco and Kohl's have jumped into the fray. Until now, conventional local TV retailers, and big box electronics outlets like Circuit City and BestBuy have been responsible for much of the sales volume of flat-panel TVs.

As prices for the new TVs fall, and larger models hit price points below $2,000, low-price retailers such as Wal-Mart and Costco are becoming a larger part of the retailing market.

It's not surprising that so many retailers are drawn to an almost-sure thing- the rise in popularity, as prices fall, of flat-panel television. Of course, if these companies do realize tremendous sales growth from the products, then, at some point, they face a dilemma in replacing that sales growth, or lapsing back into slower-growth modes. And that type of pattern typically keeps companies from earning consistently superior total returns over a number of years.

With so many retailers entering this product/market, it suggests that the production capacities for these TVs, probably in the Far East, must be very large. It doesn't require a lot of thought to envision some pretty vicious retail price competition, as a flood of flat-panel models pour into the US market in the next few years.

On another retail topic, today's Journal catalogued a number of states and municipalities which are passing, or have passed, anti-Wal-Mart legislation.

The Journal piece quotes Boston's Mayor, Thomas Menino, as saying,

"They don't pay wages that are sufficient. Their benefit structure is poor. I don't need employers like that in our city."

Interesting that a public official feels comfortable prohibiting citizens from choosing to work for Wal-Mart, or the company for risking its own capital in opening a store in the Boston area. So much for individual liberty in terms of choosing employment options in Boston.

However, a company that has engendered this type of reaction across the country can't be in great shape. Many municipalities seem to be restricting or prohibiting Wal-Mart's entry in order to protect their locally-owned businesses.

As I wrote here, and here, recently, Wal-Mart is already tampering with the branding and positioning strategies which brought it such success over the past two decades.

These cases of governmental hostility to the company's expansion plans would seem to add more challenges to Wal-Mart's already-full plate. According to the Journal's piece, the company's sales growth has slowed below double-digits recently, after decades in the that range. Same-store sales growth is a third of what it was in 1990.

The company is targeting urban areas, finally, for its next growth spurt. But it doesn't look like that's going to be happening.

Which corresponds with what I wrote here last fall. I just don't see the company continuing its past successes in terms of both fundamental growth and consistently superior total returns for its shareholders.

US Corporate Recruiting of MBAs: The WSJ's Survey

Last week's Wall Street Journal survey of corporate recruiters ranked the University of Michigan as the nation's #1 graduate school of business. In fact, the highest rank for one of the traditionally better-known schools was #7, for the University of Pennsylvania's Wharton School.

In a way, I believe it explains some of what we see in corporate America.The recruiters, according to the article accompanying the rankings, value 'communication and interpersonal skills,' 'ability to work within a team,' and 'personal ethics and integrity' all above more task-related dimensions like 'analytical and problem-solving skills,' and 'strategic thinking.'

It conjures up in my mind a group of nice, well-dressed, friendly but unimaginative young MBAs all gathered around a large conference table, 'teamworking' some issue for their new employer.

Perhaps the average returns of US business doesn't get 'better' because so many companies are so pragmatic when it comes to hiring management 'talent.' If they hire MBAs for teamwork and communication, maybe they miss getting problems solved, spotting opportunities for innovative products and services, or making the right strategic moves.

To me, this survey's results firmly indicate that the MBA has finally become a trade degree, along the lines of an electrician's or plumber's license. Not a toolkit for business value creation.

My partner discussed the survey results with his son, and they agreed that, given the choice between attending Michigan or, Penn, Chicago, MIT, etc, they'd both pass on Michigan for one of the other business schools with faculties more associated with the development and publication of new business thinking.

While I am not surprised with the survey's results, I believe it confirms a continuing use of business schools by companies as a rudimentary training ground for mundane business management needs, rather than a source of potential leadership and fresh thinking.

What I would be more interested in, from the survey's results, is which companies recruit more heavily at the more classically-highly-ranked schools, such as Wharton, Harvard, Yale, Sloan, Chicago, etc. Is there a difference in companies' long-term total return performance which is in any way explained or associated with the schools from which they primarily draw their new management hires?

Could we develop a profile of how the customers of some graduate schools of businesses are different than those of others? In a word, segment the customers of these schools?

Have the schools themselves done so, and, if so, what have they found?

Now, that would really interest me. Perhaps the WSJ should do this in the future, to provide some more interesting insights on what the trends in selection criteria imply for company performance over the long term. Summary statistics are nice, but the segment-specific insights would be very revealing.

In a way, I believe it explains some of what we see in corporate America.The recruiters, according to the article accompanying the rankings, value 'communication and interpersonal skills,' 'ability to work within a team,' and 'personal ethics and integrity' all above more task-related dimensions like 'analytical and problem-solving skills,' and 'strategic thinking.'

It conjures up in my mind a group of nice, well-dressed, friendly but unimaginative young MBAs all gathered around a large conference table, 'teamworking' some issue for their new employer.

Perhaps the average returns of US business doesn't get 'better' because so many companies are so pragmatic when it comes to hiring management 'talent.' If they hire MBAs for teamwork and communication, maybe they miss getting problems solved, spotting opportunities for innovative products and services, or making the right strategic moves.

To me, this survey's results firmly indicate that the MBA has finally become a trade degree, along the lines of an electrician's or plumber's license. Not a toolkit for business value creation.

My partner discussed the survey results with his son, and they agreed that, given the choice between attending Michigan or, Penn, Chicago, MIT, etc, they'd both pass on Michigan for one of the other business schools with faculties more associated with the development and publication of new business thinking.

While I am not surprised with the survey's results, I believe it confirms a continuing use of business schools by companies as a rudimentary training ground for mundane business management needs, rather than a source of potential leadership and fresh thinking.

What I would be more interested in, from the survey's results, is which companies recruit more heavily at the more classically-highly-ranked schools, such as Wharton, Harvard, Yale, Sloan, Chicago, etc. Is there a difference in companies' long-term total return performance which is in any way explained or associated with the schools from which they primarily draw their new management hires?

Could we develop a profile of how the customers of some graduate schools of businesses are different than those of others? In a word, segment the customers of these schools?

Have the schools themselves done so, and, if so, what have they found?

Now, that would really interest me. Perhaps the WSJ should do this in the future, to provide some more interesting insights on what the trends in selection criteria imply for company performance over the long term. Summary statistics are nice, but the segment-specific insights would be very revealing.

Subscribe to:

Posts (Atom)