Today's Wall Street Journal featured an article in the first column on page one, concerning the newest trend in corporate motivational speakers- disabled people who survived personal trauma.

I won't go into details regarding the various people with physical or other handicaps who are making substantial amounts of money on the speaking circuit. And I don't wish to make light of their very real infirmities, disabilities, etc.

However, I'd like to focus on what the employment of these people by corporate leaders, for motivational purposes, implies.

To me, it's essentially saying to a company's workforce,

'Dear employees...we've dealt you a sorry corporate hand....live with it..no, wait, better yet, let's get someone in here with a personal tragedy which they had to overcome....now, maybe you will feel that the situation in which we pay you to be, is, in fact, your own personal life tragedy, and you'll move heaven and earth, for no more money, to make our corporate objectives feel like your own personal life struggles.'

If this were done to me, I'd be furious.

Coming from senior managment, it would further make me feel that they were, in effect, delivering this message, too,

'Never mind the options and terrific pay we, your senior management, receive as compensation. You should feel personally challenged to meet the unreasonable goals we've set for you with too-little support, mediocre strategies, and/or products and/or services with no competitive advantage. Never mind the promotion of politically-motivated colleagues above you, or the niggardly compensation increases we give you. Instead, please try to place yourself in the position of this person with a genuine, unavoidable personal handicap, learn from her or his life story, and then treat your employment situation with the same kind of gravity as this person handled her or his life.'

How cynical is that?

Hopefully, this is one of those trends, like "team building," which turn out to be just a passing fad. It seems to shift the focus for corporate performance from a realistic appraisal of a company's or business unit's situation, goals, resources, etc., to a campaign that simply instructs employees to forget all of that, and behave like the only thing that matters is personal motivation.

It reminds me of the real activities of the Soviet Army's NKVD squads in WWII. They would liberally dispense vodka to the infantry troops the night before a mass human wave attack upon German positions. Sober troops might think twice about attacking fortified lines with light infantry arms, but drunken troops could be motivated to make the ultimate sacrifice for the Motherland.

Unfortunately, corporate employment isn't combat, and it's also not a fight for one's homeland. Instead, using handicapped motivational speakers to inspire employees who have been, over the past decade, down-sized, right-sized, sigma-sixed, etc., and had their compensation squeezed as well, is misplacing the responsibility for corporate performance.

If a company is doing well, one would hope these tricks would be unnecessary. If it's doing poorly, should the CEO and his management team not analyze their strategic situation, competitive position, etc, before simply assuming the problem is insufficiently motivated shock troops?

Is it really necessary, as the WSJ piece mentions in one example, to 'inspire' internal finance managers by one handicapped person's personal story of overcoming adversity? How much adversity can there be in a finance function?

When I read this story, I was reminded of a comment made to me by my very first manager at AT&T, over twenty years ago,

"Sometimes I don't know whether to laugh or cry. But I laugh, because it hurts less than crying."

After reading this article, I found myself laughing, because it hurt less. And resolving to read Dilbert, which was motivated by this sort of corporate managerial nonsense, a lot more often.

Friday, October 13, 2006

Thursday, October 12, 2006

EBay and China Again: More Troubling Signs

The Wall Street Journal's Money and Investing section carried a piece about EBay's recent troubles in China. That is to say, it was an 'investing' story, not a 'strategy' story. However, it reminded me of a similar story about Amazon in the WSJ in August, about which I wrote a piece, here.

EBay is now in trouble in both China and Korea. Although the EBay spokesman attempts to paint a rosy picture, in this case, I think one should trust the numbers, not the PR prouncements.

For instance, according to the Journal piece, EBay's market share in China is 29%, a distant second to market leader TaoBao, with 67%. And the former's listings growth has slowed from 300% year-to-year, to a much lower 127% in the recent period.

Here's EBay's spin on the Asian situation. Regarding China, they are “very happy” with business there and are “well positioned” to succeed there over a 5-10 years period. Their spokesman, Mr. Durzy, further says that their Chinese site “is comparable- if not better than- rivals’ sites, because eBay offers communications tools such as Skype and PayPal.” Quotes are of the WSJ article.

The reason for the piece is the 30% decline in EBay's stock price this year, and longer-term decline as well.

In this case, I'd go with the market share and market price numbers. EBay is clearly in trouble in both China and Korea, and the anemic growth in those markets has affected its total returns to shareholders.

As I discussed this piece today over lunch with my partner, he asked if I had reflected this in my recent piece on female CEOs. I had not, since I was focusing that post on Carol Bartz.

However, upon further reflection of EBay's performance since it went public, and this WSJ article, I am beginning to wonder if EBay's early total return performance was not almost pre-ordained, given the environment of that era. It was a new issue, in a hot product/market space. Could it really have taken all that much to simply maintain the early momentum when online auction sites were so new?

Well, we shall soon see. Because it looks like it's crunch time for Meg Whitman and her team now.

I used ebay. I’ve never used skype. I think ebay is probably in serious trouble, because what they offer, and think matters, does not matter to customers.

EBay is now in trouble in both China and Korea. Although the EBay spokesman attempts to paint a rosy picture, in this case, I think one should trust the numbers, not the PR prouncements.

For instance, according to the Journal piece, EBay's market share in China is 29%, a distant second to market leader TaoBao, with 67%. And the former's listings growth has slowed from 300% year-to-year, to a much lower 127% in the recent period.

Here's EBay's spin on the Asian situation. Regarding China, they are “very happy” with business there and are “well positioned” to succeed there over a 5-10 years period. Their spokesman, Mr. Durzy, further says that their Chinese site “is comparable- if not better than- rivals’ sites, because eBay offers communications tools such as Skype and PayPal.” Quotes are of the WSJ article.

The reason for the piece is the 30% decline in EBay's stock price this year, and longer-term decline as well.

In this case, I'd go with the market share and market price numbers. EBay is clearly in trouble in both China and Korea, and the anemic growth in those markets has affected its total returns to shareholders.

As I discussed this piece today over lunch with my partner, he asked if I had reflected this in my recent piece on female CEOs. I had not, since I was focusing that post on Carol Bartz.

However, upon further reflection of EBay's performance since it went public, and this WSJ article, I am beginning to wonder if EBay's early total return performance was not almost pre-ordained, given the environment of that era. It was a new issue, in a hot product/market space. Could it really have taken all that much to simply maintain the early momentum when online auction sites were so new?

Well, we shall soon see. Because it looks like it's crunch time for Meg Whitman and her team now.

I used ebay. I’ve never used skype. I think ebay is probably in serious trouble, because what they offer, and think matters, does not matter to customers.

Wednesday, October 11, 2006

Female CEOs: The Unheralded Carol Bartz of Autodesk

Alan Murray of the Wall Street Journal wrote a fine article in today's edition, discussing the behaviors of HP's two most recent, most senior female officers, Carly Fiorina and Patty Dunn.

His point is that both women did their gender a disservice by ducking for cover and choosing to be victims in their individual stories of strife and loss at the computer and printer manufacturing company.

Mr. Murray is, I think, entirely correct in noting that both women protest that nothing was their fault, and that they bore no responsibility for anything that happened to them. And HP certainly has suffered for their actions, inactions, and failures while they were affiliated with it.

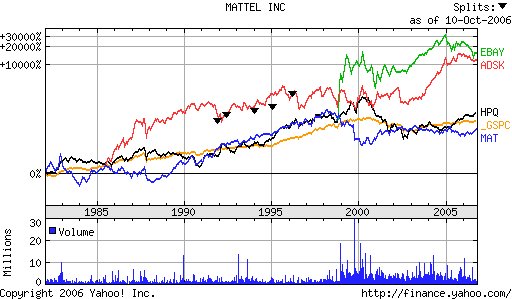

What I don't understand is why more attention isn't showered on at least two more successful and stable female CEOs: Meg Whitman of eBay, and Carol Bartz of Autodesk.

The chart at the top of this piece displays the stock price performances of four companies that have been led by women for at least several years. Jill Barad was CEO at Mattel during 1997-2000. Meg Whitman has headed eBay since 1998, while Carly Fiorina was CEO of HP during the period 1999-2005. Carol Bartz has been CEO of Autodesk since 1992, only stepping down from active leadership of the firm earlier this year.

While Barad and Fiorina destroyed value at their companies during their tenure, Whitman and Bartz have had longer tenures and presided over significant wealth creation for their shareholders. Although Whitman's eBay has slumped recently, it still has an enviable record during her tenure, roughly equaling that of Autodesk for the period in which eBay has been public.

In my opinion, however, Carol Bartz is the class of the class. She has created value consistently at Autodesk for 14 years, with the exception of some rough years in the late '90s. Even then, however, the company tended to tread water, and not lose substantial value for long time periods.

I think it does seem unfair that Bartz is not accorded the type of press that GE's Jack Welch received for his long-term performance. Blogger is not cooperating with the uploading of a price chart comparing GE and Autodesk over many years, but suffice to say, Bartz looks as good as Welch, when the two companies' performances are compared for the years in which they both were CEOs of their respective companies.

If Bartz is being ignored because of her gender, then that's even more bad news to add to Alan Murray's contentions. Not only do poorly performing female CEOs, like Jill Barad, get spotlighted, but the rare excellent performers, like Bartz, are conveniently forgotten.

Personally, I believe that good leaders of either gender are more like each other, than they are like non-leaders of their own gender. Bartz is a great CEO who happens to be a woman, not vice versa. In this case, I'd like to learn more about how Bartz ran Autodesk so well in a tough, single market business. Welch had the luxury of multiple businesses driving GE. I think we all lose a lot when successful CEOs like Carol Bartz go unstudied and unrecognized.

Tuesday, October 10, 2006

YouTube & Google

Well, it's official. Does any business pundit, media personality, or publication not have an opinion on this recent tie-up?

Probably not. So here's mine.

I think the most unique value I can add to assess Google's purchase, for $1.65B of stock, of YouTube, is to suggest that the value to Google of YouTube is a binary proposition. Either the online ad business is stable and continuing to grow, does not collapse as Net Bubble II, and YouTube is a smart move, or, we are living amidst the second internet bubble, it will "pop," and Google's purchase of a profitless online company with virtually no proprietary content, will look silly.

I doubt the result will be anything in between.

The CNBC pundits, and their guests, pretty much shake out into the two camps you'd expect.

On one hand, you have those who (correctly, I believe) see this as Google paying $1.65B to deny Microsoft, Amazon, Yahoo, News Corp, TimeWarner, Comcast, et.al., the hottest, largest video content destination in the online world at present.

Given Google's current $130B market capitalization, YouTube cost barely over 1% of their value. And latter's stock rose $4 yesterday, on the acquisition news, or roughly $1.2B. Yes, if you're waggish, you can say, "look, the damn thing almost paid for itself in one day!"

But, seriously, if we are all drinking the Kool-Aid, this deal made sense. It is Google's wise use of its almost untouchable market value to pay up for a unique online asset, and also deny it to any potential competitor. Very shrewd. Very aggressive, using one of their unique advantages, the ability to fund large acquisitions, and outspend, outmaneuver, any would-be challengers to Google's ability to blanket everything online with ads.

In a way, it meshes with my thoughts about Google from last year, as well as earlier this summer, found here. Basically, Google's leaders know they can no longer re-Google their own firm. They are simply already to large. But they do own market value. And they have made so much money, that they can literally afford to begin to spread that largesse around, forward, to new challengers who might unravel Google's carefully-sewn blanketing of the online market for ads and searches. By not being too greedy, and seeing their incredible market cap as a piggy bank sort of found in the brush, to be shared with deserving other innovators, Google may well extend and expand its market dominance for some time to come.

On the other hand, many analysts note that YouTube has no profits. It is a total hedge purchase by Google, and will never justify its price.

As I noted up in the early paragraphs of this post, I think it's an either/or sort of situation. Either Google, in general, is valuable, and, thus, by extension, so is YouTube. Or it's a blip, another AOL, and when it dissolves in one, huge online bubble-burst, YouTube will look like a foolish move.

By the way, in that regard, consider this, if you will. YouTube has fewer than 70 employees. Suppose the two founders only keep half of the $1.65B in stock, and give the rest, net of Sequoia Capital's 30%, to their employees. With $825MM left, Google's value could plummet by 99%, and the founders would still enjoy a payoff of $8.25MM, or over $4MM apiece. Is that so bad for a year's hard work and a little imagination?

However, back to the pessimistic view. Back in the late '90s, when clicks were supposed to replace bricks (and mortar), the items in question were physical goods. Online pet stores, etc, could not, in the end, sustain sufficient sales volumes to justify their market values.

Now, however, the material in question is entertainment. Digital entertainment, to be specific. It's all over the place, so finding one place where millions of people concentrate to find and view the digital video entertainment is extremely valuable.

Nevermind CNBC's Bob Griffith's inane question, something like 'couldn't I start a video website with $1.65B?' Sure he could, and so could I, and so could you.

But it wouldn't be YouTube, now, would it? It might look the same, but if people don't put up their video content, you're just not "there."

True, YouTube owns virtually none of the content it hosts. Now...wait a minute...let me think.... That reminds me of....eBay! They don't own the merchandise they intermediate, either, do they? Their best days might be over, but they, too, had a good run at the top, when online auction was a fresh business model.

I think the bottom line this time is that the acquisition of YouTube by Google, in the competitive context of today's online digital content business, is a cheap defensive tactic, and perhaps a profitable offensive strategy, as well. Old media is going to have to continue to use new media as its distribution channel onto the internet. They just don't have the mindset to invent or grow their own YouTube, Bob Griffith's opinion notwithstanding.

Probably not. So here's mine.

I think the most unique value I can add to assess Google's purchase, for $1.65B of stock, of YouTube, is to suggest that the value to Google of YouTube is a binary proposition. Either the online ad business is stable and continuing to grow, does not collapse as Net Bubble II, and YouTube is a smart move, or, we are living amidst the second internet bubble, it will "pop," and Google's purchase of a profitless online company with virtually no proprietary content, will look silly.

I doubt the result will be anything in between.

The CNBC pundits, and their guests, pretty much shake out into the two camps you'd expect.

On one hand, you have those who (correctly, I believe) see this as Google paying $1.65B to deny Microsoft, Amazon, Yahoo, News Corp, TimeWarner, Comcast, et.al., the hottest, largest video content destination in the online world at present.

Given Google's current $130B market capitalization, YouTube cost barely over 1% of their value. And latter's stock rose $4 yesterday, on the acquisition news, or roughly $1.2B. Yes, if you're waggish, you can say, "look, the damn thing almost paid for itself in one day!"

But, seriously, if we are all drinking the Kool-Aid, this deal made sense. It is Google's wise use of its almost untouchable market value to pay up for a unique online asset, and also deny it to any potential competitor. Very shrewd. Very aggressive, using one of their unique advantages, the ability to fund large acquisitions, and outspend, outmaneuver, any would-be challengers to Google's ability to blanket everything online with ads.

In a way, it meshes with my thoughts about Google from last year, as well as earlier this summer, found here. Basically, Google's leaders know they can no longer re-Google their own firm. They are simply already to large. But they do own market value. And they have made so much money, that they can literally afford to begin to spread that largesse around, forward, to new challengers who might unravel Google's carefully-sewn blanketing of the online market for ads and searches. By not being too greedy, and seeing their incredible market cap as a piggy bank sort of found in the brush, to be shared with deserving other innovators, Google may well extend and expand its market dominance for some time to come.

On the other hand, many analysts note that YouTube has no profits. It is a total hedge purchase by Google, and will never justify its price.

As I noted up in the early paragraphs of this post, I think it's an either/or sort of situation. Either Google, in general, is valuable, and, thus, by extension, so is YouTube. Or it's a blip, another AOL, and when it dissolves in one, huge online bubble-burst, YouTube will look like a foolish move.

By the way, in that regard, consider this, if you will. YouTube has fewer than 70 employees. Suppose the two founders only keep half of the $1.65B in stock, and give the rest, net of Sequoia Capital's 30%, to their employees. With $825MM left, Google's value could plummet by 99%, and the founders would still enjoy a payoff of $8.25MM, or over $4MM apiece. Is that so bad for a year's hard work and a little imagination?

However, back to the pessimistic view. Back in the late '90s, when clicks were supposed to replace bricks (and mortar), the items in question were physical goods. Online pet stores, etc, could not, in the end, sustain sufficient sales volumes to justify their market values.

Now, however, the material in question is entertainment. Digital entertainment, to be specific. It's all over the place, so finding one place where millions of people concentrate to find and view the digital video entertainment is extremely valuable.

Nevermind CNBC's Bob Griffith's inane question, something like 'couldn't I start a video website with $1.65B?' Sure he could, and so could I, and so could you.

But it wouldn't be YouTube, now, would it? It might look the same, but if people don't put up their video content, you're just not "there."

True, YouTube owns virtually none of the content it hosts. Now...wait a minute...let me think.... That reminds me of....eBay! They don't own the merchandise they intermediate, either, do they? Their best days might be over, but they, too, had a good run at the top, when online auction was a fresh business model.

I think the bottom line this time is that the acquisition of YouTube by Google, in the competitive context of today's online digital content business, is a cheap defensive tactic, and perhaps a profitable offensive strategy, as well. Old media is going to have to continue to use new media as its distribution channel onto the internet. They just don't have the mindset to invent or grow their own YouTube, Bob Griffith's opinion notwithstanding.

Monday, October 09, 2006

GM & Nissan's Failed Alliance Talks: Wagoner Wins Round 1

This weekend saw the further development of two major business news stories. One culminated this afternoon, but the other will probably run for months, if not years.

On Friday, Jerry York, Kirk Kerkorian's agent on the GM board, announced his resignation from said position. Round one has clearly gone to Wagoner, but I suspect, in the end, that it will be a pyrrhic victory.

Now that York has left GM's board, Kerkorian has withdrawn his offer/plan to raise his stake in the company. Upon learning that, investors sent GM's shares down sharply Friday afternoon.

At this point, many are speculating on Kerkorian's next moves, and the timing thereof. CNBC's official "car guy," Phil Lebeau, preaches that Kerkorian will now sit back and wait, as he and York did with Chrysler.

However, that was then. "Now" is different. I don't think so much of the American auto sector was in such dire straits back then, as it is now. Ford, and even GM, probably don't have as much time as Chrysler did, with guaranteed funding, to regain their health and competitive strength.

My own guess is that Kerkorian, who, in my memory, has not lost money on a major investment since at least 1979, will move to take over the GM board in the spring, and then move quickly. Personally, I think he and York plan to emulate the late, great, J.P. Morgan, and single-handedly restructure the remaining US auto makers into one firm, allied with Nissan/Renault.

One thing Kerkorian and York are not is sentimental. They realize that, regardless of the brand names, Ford and GM essentially still, for a little while longer, have some residual market share and loyalty on which to build. This needs to be cut loose from moronic, myopic management, and inefficient production modes, in order to be served by the better management of Nissan. I think the two takeover veterans have more than just GM in their sights. After they unseat Wagoner, they can approach Ford, regardless of whether it has joined up with Ghosn and Nissan.

I would not bet on this, yet, per se. But neither would I be at all surprised. Ford clearly has to have a partner now. Kerkorian wants Ghosn to manage GM's assets. If all three, or four, with Renault, can play, so much the better. Kerkorian and York understand that scale and depth of talent will be needed to prosper, let alone survive, competing with Toyota in the years ahead.

Friday's events did not surprise me. It just demonstrates how insecure and small-minded Rick Wagoner really is. And how dismissive he is of, and insensitive to, the needs and obligations of his shareholders. These days, that is probably a terminal mistake for a CEO to make, especially on the scale Wagoner has made it.

On Friday, Jerry York, Kirk Kerkorian's agent on the GM board, announced his resignation from said position. Round one has clearly gone to Wagoner, but I suspect, in the end, that it will be a pyrrhic victory.

Now that York has left GM's board, Kerkorian has withdrawn his offer/plan to raise his stake in the company. Upon learning that, investors sent GM's shares down sharply Friday afternoon.

At this point, many are speculating on Kerkorian's next moves, and the timing thereof. CNBC's official "car guy," Phil Lebeau, preaches that Kerkorian will now sit back and wait, as he and York did with Chrysler.

However, that was then. "Now" is different. I don't think so much of the American auto sector was in such dire straits back then, as it is now. Ford, and even GM, probably don't have as much time as Chrysler did, with guaranteed funding, to regain their health and competitive strength.

My own guess is that Kerkorian, who, in my memory, has not lost money on a major investment since at least 1979, will move to take over the GM board in the spring, and then move quickly. Personally, I think he and York plan to emulate the late, great, J.P. Morgan, and single-handedly restructure the remaining US auto makers into one firm, allied with Nissan/Renault.

One thing Kerkorian and York are not is sentimental. They realize that, regardless of the brand names, Ford and GM essentially still, for a little while longer, have some residual market share and loyalty on which to build. This needs to be cut loose from moronic, myopic management, and inefficient production modes, in order to be served by the better management of Nissan. I think the two takeover veterans have more than just GM in their sights. After they unseat Wagoner, they can approach Ford, regardless of whether it has joined up with Ghosn and Nissan.

I would not bet on this, yet, per se. But neither would I be at all surprised. Ford clearly has to have a partner now. Kerkorian wants Ghosn to manage GM's assets. If all three, or four, with Renault, can play, so much the better. Kerkorian and York understand that scale and depth of talent will be needed to prosper, let alone survive, competing with Toyota in the years ahead.

Friday's events did not surprise me. It just demonstrates how insecure and small-minded Rick Wagoner really is. And how dismissive he is of, and insensitive to, the needs and obligations of his shareholders. These days, that is probably a terminal mistake for a CEO to make, especially on the scale Wagoner has made it.

Subscribe to:

Posts (Atom)

{kind=link}