I read in Friday's Wall Street Journal that Bill Gates announced his retirement from Microsoft effective in two year's time. Ray Ozzie is to become "chief software architect," apparently effectively immediately.

As I have written before in this column, here, and here, I think this will be a good move, but at least two years too late. Ozzie had impeccable software design credentials before he came to Microsoft. Actually, better than Gates'. One technology veteran, whose name I do not recall, was cited as having credited Gates with inventing the "software in a box" business, but said Bill never really understood or came to terms with the 'free online software' approach that is currently gutting Microsoft's business model. Yes, it's time for Chairman Bill to go play with his billions and leave the serious business of rescuing Microsoft to more open-minded adults.

Rather than, as I suggested last fall, have Ozzie take a $20MM check down the road and start up a new company for Microsoft, Gates is stepping out of the way at the parent instead. Trouble is, the culture is still what it is, and Ozzie may have challenges changing it for the better. And Gates will be around the company for two more years.

Corporate history is replete with examples of how resistant to change companies are when the retiring leader remains "around." The best example I recall is Harry J. Gray, of United Technologies, hampering Rand Araskog after the so-called "transition" of leadership from the former to the latter. I'm sure there are other examples.

About the best that can be said of this change, for Microsoft shareholders, is that at least Gates is going to subject them to no more than two additional years of value destruction before making way for better, more objective and value-creating management. If the shareholders are lucky, Ray Ozzie won't have left in the meantime due to clashes with Ballmer or other long-time Microsoft veterans..

Saturday, June 17, 2006

"Efficient Markets" from the Wall Street Journal

This week saw the Wall Street Journal publish two pieces under the theme "efficient markets." Once again, I am disappointed with what they will fill 2/3 of their op-ed page. Each piece has some glaring faults, in my opinion.

The first, appearing Tuesday, was written by the retired head of George Mason University's law school, one Henry Manne. He makes a good conclusion, despite most of his article having little to do with it. Essentially, Manne draws a distinction between viewing market prices for a stock as primarily affected by the last, "marginal" investor/trader, and viewing them as the averaged guesses of a large number of buyers and sellers. He cites an intriguing-sounding book in this regard. So intriguing, I'll probably go to Amazon to buy the book, and forget Manne's name after next week.

In any case, Manne uses this contrast to argue for legalizing all "insider trading" which is not specifically prohibited by contracts, i.e., mergers and acquistions activity, or other confidential activities. What he proposes is that company officers not prohibited to trade because of confidential deal knowledge, be allowed to trade based upon their legal, but special, knowledge of their company. I have agreed with this point of view for decades.

Where Manne seems to wander into difficult terrain is in his critique of behavioral finance. After generally acknowledging it as a field, he vaguely dismisses most of its findings as 'prove in time to be less anomalous than was first thought,' but gives no particulars. He then castigates the field for having no general theory of why markets operate as they do. He then states that, this being the case, "some close approximation of the efficient market theory is still the most accurate and useful model of the stock market that we have."

I guess this is where I suggest that maybe a former law school Dean is the wrong guy to engage to write a moving treatise on the differences between behavioral finance proponents and efficient markets supporters. I find Manne's logic to be simply wrong. Nobody of whom I know has mandated that the field of behavioral finance must spring into being whole and possessing a full depth of decades of research on the order of that existing for efficient markets.

In fact, as Thomas Kuhn propounded several decades ago, in his work on the structure of scientific revolution, new schools of thought usually begin by nibbling away at the errors at the margins of theories of the reigning school. Only with time and resources does the newer theoretical school of thought build its own full theories to explain complete workings of systems.

Just because behavioral finance is now becoming more well-known and possessing of deeper research, does not mean we have to continue to accept the flawed reasoning of efficient markets theorists.

In my opinion, Manne could have begun his article with his citing of the book, "The Wisdom of Crowds, by James Surowecki, and it would have been more succinct and better reasoned.

The second part of this short series appeared in Wednesday's WSJ, again on the op-ed page. This article was authored by Jeremy J. Siegel, a Finance professor from one of my alma mater's, the University of Pennsylvania. His topic is the imminent rise of non-cap-weighted indices for financial asset management.

I won't go into the details of Siegel's arguments here, except to state that he believes it will soon be possible to use fundamental measures, such as sales or dividends, to weight indices for use in financial asset management. Siegel pounds away at one theme in particular- that these new indices would allow for higher average returns, and less volatility, than the various current cap-weighted indices, such as the S&P500, Russell, or Nasdaq.

There are, however, to problems with Siegel's positions. First, it is partially disclosed that he has been busily working to create just these types of 'new' indices with a private firm, WisdomTree Asset Management. So, in reality, this op-ed piece seems to be a thinly-disguised piece of public relations and "placed" advertising.

But the more substantive error Siegel makes is in arguing that the measurement function for a "successful," or "useful," index, is that is exhibit high returns with low volatility. It seems to me that he is confusing a market index with an investment strategy.

Indices such as the S&P500 are composed for a specific reason: to emulate the allocation of resources in the US economy, by sector. The S&P500 is actively managed in its membership by Standard & Poors, a McGraw-Hill unit, in order to provide a group of publicly-traded companies whose business activity and weighting are reasonably representative of the activity of the US economy. When you buy this index, you are, in effect, buying the performance of the US economy, broadly described. That's all it is. It's not supposed to have a target return or volatility.

It's the same with the Russell and Nasdaq, for their particular representations. The objectives are to represent some specific underlying economic activity, not to tailor an index to the point that it becomes an active investment strategy all on its own.

That said, I am disappointed that these two flawed pieces found there way, with such fanfare, onto the Journal's pages this week. One author writes badly-reasoned prose about a field that isn't actually his area of expertise, while another author completely misses the point of his subject and, instead, lobbies for his current business enterprise to be used to replace current market indices.

If this is an example of the WSJ's best efforts at financial market education and theoretical advancement, perhaps we now have a better understanding of why the markets are so dominated by such frenetic, emotional short-term trading activity. Market participants are unlikely to find much in the way of helpful insight in the pages of our nation's major business daily newspaper.

The first, appearing Tuesday, was written by the retired head of George Mason University's law school, one Henry Manne. He makes a good conclusion, despite most of his article having little to do with it. Essentially, Manne draws a distinction between viewing market prices for a stock as primarily affected by the last, "marginal" investor/trader, and viewing them as the averaged guesses of a large number of buyers and sellers. He cites an intriguing-sounding book in this regard. So intriguing, I'll probably go to Amazon to buy the book, and forget Manne's name after next week.

In any case, Manne uses this contrast to argue for legalizing all "insider trading" which is not specifically prohibited by contracts, i.e., mergers and acquistions activity, or other confidential activities. What he proposes is that company officers not prohibited to trade because of confidential deal knowledge, be allowed to trade based upon their legal, but special, knowledge of their company. I have agreed with this point of view for decades.

Where Manne seems to wander into difficult terrain is in his critique of behavioral finance. After generally acknowledging it as a field, he vaguely dismisses most of its findings as 'prove in time to be less anomalous than was first thought,' but gives no particulars. He then castigates the field for having no general theory of why markets operate as they do. He then states that, this being the case, "some close approximation of the efficient market theory is still the most accurate and useful model of the stock market that we have."

I guess this is where I suggest that maybe a former law school Dean is the wrong guy to engage to write a moving treatise on the differences between behavioral finance proponents and efficient markets supporters. I find Manne's logic to be simply wrong. Nobody of whom I know has mandated that the field of behavioral finance must spring into being whole and possessing a full depth of decades of research on the order of that existing for efficient markets.

In fact, as Thomas Kuhn propounded several decades ago, in his work on the structure of scientific revolution, new schools of thought usually begin by nibbling away at the errors at the margins of theories of the reigning school. Only with time and resources does the newer theoretical school of thought build its own full theories to explain complete workings of systems.

Just because behavioral finance is now becoming more well-known and possessing of deeper research, does not mean we have to continue to accept the flawed reasoning of efficient markets theorists.

In my opinion, Manne could have begun his article with his citing of the book, "The Wisdom of Crowds, by James Surowecki, and it would have been more succinct and better reasoned.

The second part of this short series appeared in Wednesday's WSJ, again on the op-ed page. This article was authored by Jeremy J. Siegel, a Finance professor from one of my alma mater's, the University of Pennsylvania. His topic is the imminent rise of non-cap-weighted indices for financial asset management.

I won't go into the details of Siegel's arguments here, except to state that he believes it will soon be possible to use fundamental measures, such as sales or dividends, to weight indices for use in financial asset management. Siegel pounds away at one theme in particular- that these new indices would allow for higher average returns, and less volatility, than the various current cap-weighted indices, such as the S&P500, Russell, or Nasdaq.

There are, however, to problems with Siegel's positions. First, it is partially disclosed that he has been busily working to create just these types of 'new' indices with a private firm, WisdomTree Asset Management. So, in reality, this op-ed piece seems to be a thinly-disguised piece of public relations and "placed" advertising.

But the more substantive error Siegel makes is in arguing that the measurement function for a "successful," or "useful," index, is that is exhibit high returns with low volatility. It seems to me that he is confusing a market index with an investment strategy.

Indices such as the S&P500 are composed for a specific reason: to emulate the allocation of resources in the US economy, by sector. The S&P500 is actively managed in its membership by Standard & Poors, a McGraw-Hill unit, in order to provide a group of publicly-traded companies whose business activity and weighting are reasonably representative of the activity of the US economy. When you buy this index, you are, in effect, buying the performance of the US economy, broadly described. That's all it is. It's not supposed to have a target return or volatility.

It's the same with the Russell and Nasdaq, for their particular representations. The objectives are to represent some specific underlying economic activity, not to tailor an index to the point that it becomes an active investment strategy all on its own.

That said, I am disappointed that these two flawed pieces found there way, with such fanfare, onto the Journal's pages this week. One author writes badly-reasoned prose about a field that isn't actually his area of expertise, while another author completely misses the point of his subject and, instead, lobbies for his current business enterprise to be used to replace current market indices.

If this is an example of the WSJ's best efforts at financial market education and theoretical advancement, perhaps we now have a better understanding of why the markets are so dominated by such frenetic, emotional short-term trading activity. Market participants are unlikely to find much in the way of helpful insight in the pages of our nation's major business daily newspaper.

Thursday, June 15, 2006

China's Burgeoning Car Market: Can It Save GM?

Tuesday's Wall Street Journal featured a long article discussing China's explosively growing demand for automobiles. Many statistics were cited, but, suffice to say, it would seem that China is among, if not the most, fast-growing countries for auto sales.

Midway through the article, it is mentioned that GM won a "coveted deal for a joint venture" to produce autos back in 1997. That was nine years ago.

My consulting friend, S, and I were chatting about this incredible market opportunity for car manufacturers and marketers in China.

Doesn't it seem odd that GM, which is mired in such difficulties in the American car market, doesn't appear to be doing more to dominate China's auto industry? Or at least take advantage of a new, fast-growth market in order to establish some strong brand positions?

The article recounted the many car producers who are far from world-class manufacturers. These in include a cell phone manufacturer and the city of Bejing. It was striking how casually producers enter the Chinese auto market. There are apparently virtually no barriers to entry. From the picture painted by the piece, one is led to believe that there is very little concentration of market share, nor standards for what passes as a marketable car in China.

I should stipulate here that I do not have detailed knowledge of GM's market position in China, nor the various market shares among leading vendors. However, as my friend S pointed out, this market opportunity is so large, it doesn't take a lot of complicated planning by the wizards at GM in Detroit to figure out that it would be a good idea to try to become the market leader in the fastest-growing car market on the planet, in, by the way, the world's most populous country.

When the article went on to enumerate the economic challenges of the growth of automobile ownership in China- gasoline consumption, infrastructure, environmental safeguards, air quality, gasoline quality and refinery capabilities- it seemed to me that there would, or should, be a role in the Chinese automotive sector for an experienced car manufacturer with valuable knowledge which could help make the Chinese auto sector more efficient, productive, and environmentally friendly.

Could GM not bargain its capabilities at introducing various safety, emission controls, and modern auto design and manufacturing methods, for more access to the Chinese car market, and more control over its venture(s)? When you think of what GM should be good at, these sorts of attributes come to mind, as the result of manufacturing cars in a mature market for decades. Even GM's lack of effective car design in the US wouldn't appear to matter too much in the Chinese market, given how many small-scale vendors are apparently pumping out cars of a rather commodity-like nature.

If GM can't add value to a relatively primitive market like China's burgeoning car market, what can it do? If it can't make a compelling case for adding value for the Chinese automotive sector, maybe its weakness in the US is symptomatic of a truly global dilemma for the ailing car company.

It just seemed odd to me that a major article about the Chinese auto industry, in the major

US daily business newspaper, barely mentioned the world's largest car company. Or anything about how GM plans to take advantage of this rare opportunity to exploit a very large and very fast-growing market for its products.

This really doesn't seem like rocket science, or a planning challenge that the GM execs in Detroit would have to spend much time to formulate. In the best case, they could even create a new, subsidiary in China which they could eventually spin off to existing shareholders, thereby transferring the value-added elements of the current company from its troubled US domicile to another entity.

If GM's knowledge and people are still valuable, they should be able to add value in a new market, like China, even more easily than the mature, highly competitive American car market in which they currently are struggling.

Midway through the article, it is mentioned that GM won a "coveted deal for a joint venture" to produce autos back in 1997. That was nine years ago.

My consulting friend, S, and I were chatting about this incredible market opportunity for car manufacturers and marketers in China.

Doesn't it seem odd that GM, which is mired in such difficulties in the American car market, doesn't appear to be doing more to dominate China's auto industry? Or at least take advantage of a new, fast-growth market in order to establish some strong brand positions?

The article recounted the many car producers who are far from world-class manufacturers. These in include a cell phone manufacturer and the city of Bejing. It was striking how casually producers enter the Chinese auto market. There are apparently virtually no barriers to entry. From the picture painted by the piece, one is led to believe that there is very little concentration of market share, nor standards for what passes as a marketable car in China.

I should stipulate here that I do not have detailed knowledge of GM's market position in China, nor the various market shares among leading vendors. However, as my friend S pointed out, this market opportunity is so large, it doesn't take a lot of complicated planning by the wizards at GM in Detroit to figure out that it would be a good idea to try to become the market leader in the fastest-growing car market on the planet, in, by the way, the world's most populous country.

When the article went on to enumerate the economic challenges of the growth of automobile ownership in China- gasoline consumption, infrastructure, environmental safeguards, air quality, gasoline quality and refinery capabilities- it seemed to me that there would, or should, be a role in the Chinese automotive sector for an experienced car manufacturer with valuable knowledge which could help make the Chinese auto sector more efficient, productive, and environmentally friendly.

Could GM not bargain its capabilities at introducing various safety, emission controls, and modern auto design and manufacturing methods, for more access to the Chinese car market, and more control over its venture(s)? When you think of what GM should be good at, these sorts of attributes come to mind, as the result of manufacturing cars in a mature market for decades. Even GM's lack of effective car design in the US wouldn't appear to matter too much in the Chinese market, given how many small-scale vendors are apparently pumping out cars of a rather commodity-like nature.

If GM can't add value to a relatively primitive market like China's burgeoning car market, what can it do? If it can't make a compelling case for adding value for the Chinese automotive sector, maybe its weakness in the US is symptomatic of a truly global dilemma for the ailing car company.

It just seemed odd to me that a major article about the Chinese auto industry, in the major

US daily business newspaper, barely mentioned the world's largest car company. Or anything about how GM plans to take advantage of this rare opportunity to exploit a very large and very fast-growing market for its products.

This really doesn't seem like rocket science, or a planning challenge that the GM execs in Detroit would have to spend much time to formulate. In the best case, they could even create a new, subsidiary in China which they could eventually spin off to existing shareholders, thereby transferring the value-added elements of the current company from its troubled US domicile to another entity.

If GM's knowledge and people are still valuable, they should be able to add value in a new market, like China, even more easily than the mature, highly competitive American car market in which they currently are struggling.

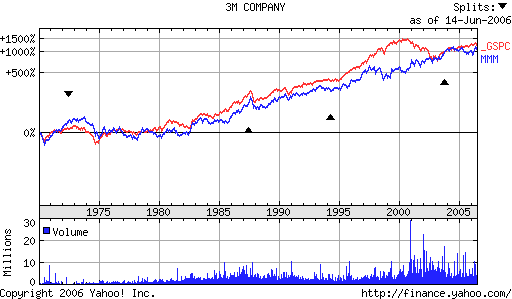

3M & McNerney

Yesterday's Wall Street Journal contained an interview with Jim McNerney, former Jack Welch lieutenant, former 3M CEO, and recently-recruited Boeing CEO.

Yesterday's Wall Street Journal contained an interview with Jim McNerney, former Jack Welch lieutenant, former 3M CEO, and recently-recruited Boeing CEO.The interview depicted McNerney as a level-headed, self-effacing, sensible leader.

However, in several passages, he referred to his 3M stint. So I was curious to see what his track record was there. Upon Googling McNerney and 3M, I see that he joined them as their first outsider CEO in December of 2000. According to an article from the time, he said he was going to focus on growing 3M.

What's interesting to me is the pattern of 3M's stock price from about the time McNerney took the helm. Until then, looking back via the Yahoo-sourced chart from 1970 to the present, 3M had pretty much tracked the S&P500 in a lockstep fashion. As the index soared in the bubble years of the late '90s, 3M's trajectory remained more modest, and continued as such after the bubble's deflation in 2001.

As of 2002, however, the two lines crossed. This means that, after some 30+ years, an investment in 3M, aside from dividends, had basically matched the S&P, but done no better. In the three years that followed, two under McNerney, the company began to depart from its index-like performance pattern.

The company's stock price began to exhibit unevenness, with declines and stagnation mixed with a brief updraft in 2003. Then the trajectory fell as the index began to regain strength.

All in all, an ironic track record for McNerney. It appears that under his leadership, 3M's stock price path remained pretty consistent, suggesting that investors didn't really see much difference with McNerney running the company. The only significant changes were bad ones- the dips in price in this decade.

What is not evident in the McNerney era of 3M is a break with its own past stock price path. It failed to noticeably ignite sufficient investor confidence or interest to move its stock price trajectory above the long term path it has been on for 30 years. That is, until recently when it has uncharacteristically flattened.

Does this portend anything for Boeing? From where does McNerney's credibility come, if this is his recent post-GE track record? Surely Boeing's recent stock price performance doesn't yet reflect McNerney's actions. For the record, it hasn't really changed, either, in several years.

I know of nothing negative about Jim McNerney. The comments attributed to him in the WSJ piece seem promising. However, that's about all there seems to be on file to suggest he will lead Boeing where it has not been before this. If 3M is any indicator, I'm not sure I expect Boeing to show any signs of unusually better performance than before McNerney arrived.

I wonder on what basis the WSJ seems so positively disposed toward Boeing and McNerney, given this lack of evidence of his prior accomplishments at 3M.

Tuesday, June 13, 2006

Old Media in The New Internet Media World

Monday's Wall Street Journal carried an interesting in-depth piece about a television station in Grand Rapids, Michigan, struggling to cope with the effects of the internet on its business model and future performance.

I wrote about this a few months ago here. In that post, I discussed the larger issue of the broadcast networks' responses to internet-based entertainment.

Now, I see by this WSJ piece, that the changes are hitting home at the local station level already. According to the article, the television station's advertising revenues and viewership are shrinking, and it is scrambling to find ways of stocking a webpage with advertising-funded content.

As I ponder the end-game of this situation, I can't help but see a parallel to the troubles and solutions of daily newspapers a decade or more ago. Papers began to share printing plants, and, essentially, become differently positioned products freelancing off of the same production assets. It would not surprise me if local television stations, including the major city stations, do the same.

The article focused on the core expense item, local news gathering. Can something like this really pay for more than one television station in a market, when the major networks can't even make it pay nationally and globally anymore? Doubtful.

Instead, I'd expect that, over the next few years, competing local broadcast stations will pool their facilities and news gathering, perhaps simply merging into one station per local market. If not the latter, then at least sharing all possible resources, save on-air staff, content selection, and idiosyncratic local programming.

What caught me a bit off-guard as I read the article is how quickly the nascent internet entertainment wave is already eroding some of the grassroots businesses in old media. My consultant friend, S, may be surprised to learn how quickly a trend she feels is years off in affecting major media behavior and consumption, is already reshaping local broadcast media in the hinterlands.

We are already seeing the beginning of old media's forced changes in the face of the rise of the new, internet-enabled digital media world.

Yet another example of Schumpeterian dynamics at work without any overt organizing entity to guide it, save technological change and consumer behavioral responses.

I wrote about this a few months ago here. In that post, I discussed the larger issue of the broadcast networks' responses to internet-based entertainment.

Now, I see by this WSJ piece, that the changes are hitting home at the local station level already. According to the article, the television station's advertising revenues and viewership are shrinking, and it is scrambling to find ways of stocking a webpage with advertising-funded content.

As I ponder the end-game of this situation, I can't help but see a parallel to the troubles and solutions of daily newspapers a decade or more ago. Papers began to share printing plants, and, essentially, become differently positioned products freelancing off of the same production assets. It would not surprise me if local television stations, including the major city stations, do the same.

The article focused on the core expense item, local news gathering. Can something like this really pay for more than one television station in a market, when the major networks can't even make it pay nationally and globally anymore? Doubtful.

Instead, I'd expect that, over the next few years, competing local broadcast stations will pool their facilities and news gathering, perhaps simply merging into one station per local market. If not the latter, then at least sharing all possible resources, save on-air staff, content selection, and idiosyncratic local programming.

What caught me a bit off-guard as I read the article is how quickly the nascent internet entertainment wave is already eroding some of the grassroots businesses in old media. My consultant friend, S, may be surprised to learn how quickly a trend she feels is years off in affecting major media behavior and consumption, is already reshaping local broadcast media in the hinterlands.

We are already seeing the beginning of old media's forced changes in the face of the rise of the new, internet-enabled digital media world.

Yet another example of Schumpeterian dynamics at work without any overt organizing entity to guide it, save technological change and consumer behavioral responses.

Monday, June 12, 2006

Stock Buybacks

The Wall Street Journal ran a front page piece today discussing large cap companies' recent trend of busily buying back stock, and that this has been misleading investors as to the actual health of the business.

I confess to have been initially confused by this. Surely nobody seriously focused just on EPS, so that a reduction in equity which would arithmetically boost the ratio is seen as performance improvement? But, I guess the WSJ is, in effect, telling us that most analysts and investors are too inept to spot this.

More to the point, though, who cares about EPS? Growth is found up on the revenue line of the income statement. EPS is such a manufactured concept that I'm surprised, especially post-Enron, that anybody would consider the measure so crucial.

I don't really care much whether companies are buying back their stock or not, ceteris paribas. If they pay too much, I presume that investors will depress the stock's price even more by selling their shares. If it's a wise move, the price and total return should rise. However, it seems to me that the more important issue is whether companies are growing revenue in a consistently superior manner.

Focusing only on balance sheet antics seems to me to be a bit misplaced. My proprietary research has found that, for growth companies, balance sheet structure, per se, is not so important as maintaining revenue growth. If a company has to resort to stock buybacks to manufacture EPS growth, and relies on investors and analysts to not notice, then it's probably already in a bad position.

Certainly, buying back stock does signal that the company hasn't adequate prospects for the capital. Perhaps the shares are priced so that the buybacks are a profitable move for the remaining shareholders.

However, it continues to amaze me that the WSJ can be serious in believing that many analysts and investors rely on EPS data, and would fail to realize whether or not a company is manipulating the measure via stock repurchases.

Looks like I'm not the only one who believes that most analysts and institutional investors constitute a mediocre crowd that mindlessly pushes near-term stock prices around with little understanding of longer-term context.

I confess to have been initially confused by this. Surely nobody seriously focused just on EPS, so that a reduction in equity which would arithmetically boost the ratio is seen as performance improvement? But, I guess the WSJ is, in effect, telling us that most analysts and investors are too inept to spot this.

More to the point, though, who cares about EPS? Growth is found up on the revenue line of the income statement. EPS is such a manufactured concept that I'm surprised, especially post-Enron, that anybody would consider the measure so crucial.

I don't really care much whether companies are buying back their stock or not, ceteris paribas. If they pay too much, I presume that investors will depress the stock's price even more by selling their shares. If it's a wise move, the price and total return should rise. However, it seems to me that the more important issue is whether companies are growing revenue in a consistently superior manner.

Focusing only on balance sheet antics seems to me to be a bit misplaced. My proprietary research has found that, for growth companies, balance sheet structure, per se, is not so important as maintaining revenue growth. If a company has to resort to stock buybacks to manufacture EPS growth, and relies on investors and analysts to not notice, then it's probably already in a bad position.

Certainly, buying back stock does signal that the company hasn't adequate prospects for the capital. Perhaps the shares are priced so that the buybacks are a profitable move for the remaining shareholders.

However, it continues to amaze me that the WSJ can be serious in believing that many analysts and investors rely on EPS data, and would fail to realize whether or not a company is manipulating the measure via stock repurchases.

Looks like I'm not the only one who believes that most analysts and institutional investors constitute a mediocre crowd that mindlessly pushes near-term stock prices around with little understanding of longer-term context.

Sunday, June 11, 2006

Ben Bernanke and His Critics

The past two weeks have provided numerous pundits and corporate economists, not to mention various 'economics reporters,' to opine on Ben Bernanke and his Fed. Especially the FOMC.

I find this somewhat amusing. After allowing for a free press, and the general value of public discourse and exchange of ideas, I believe the current flow of opinions marks most of the sources as of limited acumen or experience.

Bernanke and his colleagues have very sensibly articulated two things. First, they are data-driven in their interest rate decisions for the US economy. Second, in today's circumstances, the current 2% inflation rate is at the upper end of their comfort zone.

You don't have to be a genius to understand their message. You could, with a little experience, quickly realize that Bernanke & Co. understand the long term damage that inflation will do to the US financial markets and economy. Thus, they are acting to slow the rise of inflation now. And they are competently using the data available to modern central bankers to do so. Further, they are behaving as a coordinated, smoothly-functioning team.

If anything, most of the pundits, aside from people like Brian Wesbury and John Rutledge, seem to be incapable of simply understanding current Fed behavior.

The way I look at it is thusly. There are roughly 100 million working Americans. I don't know the exact number, but this is close enough for purposes of my example. Of these people, only one can be chosen to be Fed Chairman. That means there must be at least 40 academic, corporate, and financial services economists who believe they, too, are in the "first rank" of their profession. Toss in a few consultants, some investment fund economists, and maybe you get to 60 people. Add another 5-10 media critics, and you are near 75.

But there's only one Chairman. And he's Ben Bernanke. The other 75 people are not. They may care about Bernanke's behavior and comments, but I really doubt he cares all that much about theirs. Nor should you.

This may be worth remembering in the months and years ahead. Bernanke and the Fed, to use a famous phrase, "stand on the shoulders of giants." Paul Volcker's and Alan Greenspan's Federal Reserves were perhaps the two best monetary policy leaders and administrations our country has had. The bar was pretty high when Bernanke was confirmed as Fed Chairman.

Rather than spend a lot of time worrying about the comments of 70+ also-ran economists, pundits and media reporters, I'm going to continue to focus on Bernanke's, and other Fed Presidents,' words and actions. Perhaps you should as well. It may make for more clarity and less wasted time and effort deciphering the comments of the people who didn't get Bernanke's job.

I find this somewhat amusing. After allowing for a free press, and the general value of public discourse and exchange of ideas, I believe the current flow of opinions marks most of the sources as of limited acumen or experience.

Bernanke and his colleagues have very sensibly articulated two things. First, they are data-driven in their interest rate decisions for the US economy. Second, in today's circumstances, the current 2% inflation rate is at the upper end of their comfort zone.

You don't have to be a genius to understand their message. You could, with a little experience, quickly realize that Bernanke & Co. understand the long term damage that inflation will do to the US financial markets and economy. Thus, they are acting to slow the rise of inflation now. And they are competently using the data available to modern central bankers to do so. Further, they are behaving as a coordinated, smoothly-functioning team.

If anything, most of the pundits, aside from people like Brian Wesbury and John Rutledge, seem to be incapable of simply understanding current Fed behavior.

The way I look at it is thusly. There are roughly 100 million working Americans. I don't know the exact number, but this is close enough for purposes of my example. Of these people, only one can be chosen to be Fed Chairman. That means there must be at least 40 academic, corporate, and financial services economists who believe they, too, are in the "first rank" of their profession. Toss in a few consultants, some investment fund economists, and maybe you get to 60 people. Add another 5-10 media critics, and you are near 75.

But there's only one Chairman. And he's Ben Bernanke. The other 75 people are not. They may care about Bernanke's behavior and comments, but I really doubt he cares all that much about theirs. Nor should you.

This may be worth remembering in the months and years ahead. Bernanke and the Fed, to use a famous phrase, "stand on the shoulders of giants." Paul Volcker's and Alan Greenspan's Federal Reserves were perhaps the two best monetary policy leaders and administrations our country has had. The bar was pretty high when Bernanke was confirmed as Fed Chairman.

Rather than spend a lot of time worrying about the comments of 70+ also-ran economists, pundits and media reporters, I'm going to continue to focus on Bernanke's, and other Fed Presidents,' words and actions. Perhaps you should as well. It may make for more clarity and less wasted time and effort deciphering the comments of the people who didn't get Bernanke's job.

Subscribe to:

Posts (Atom)