skip to main |

skip to sidebar

Wednesday's Wall Street Journal carried an article on Hormel's attempt to "Add Upscale Foods Without Alienating Lovers of Its Spam." In short, to broaden its product line and stoke growth without screwing up its brand identity.

What struck me about this was a quote by Hormel's lawyer-turned-CEO, Jeffrey Ettinger,

"Hormel stands for canned ham, bacon and more traditional products. We don't want to harm these items with the target consumers."

Well, score one for Mr. Ettinger getting half of the concept of branding right. Unfortunately, the article begins by describing the company's failed attempt to market ethnic foods of restaurant quality.

The piece also lists the components of Spam, and how it is actually made. I won't go into the details here- if you're interested in them, wait a couple hours after eating, then go read the Journal article. Suffice to say, it is hard to see how a company which has staked its brand on a product like that can actually believe anyone would also buy haute cuisine from the same kitchens.

As I wrote here in September of last year, about Les Wexner's Limited Brands strategy, Hormel could simply create a new brand identity for these upscale offerings. For example, Frito-Lay acquired Stacy's Pita Chips last year, as described here. The announcement states,

"Stacy's, which will continue to be based in Randolph, MA, with more than 100 employees, is planned to operate as a separate unit and report to Frito-Lay North America chairman and chief executive officer Irene Rosenfeld."

I Googled Stacy's Pita Chips and had to search through two screens to learn who the acquirer was. I was aware some large food company had acquired it, but could recall which one. It is nowhere to be seen on the Stacy's packages.

Why can't Hormel do likewise?

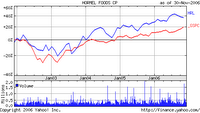

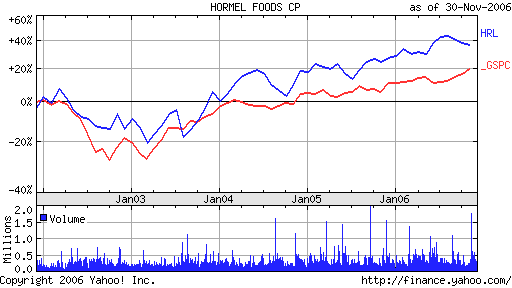

As the nearby Yahoo-sourced, five-year price chart of Hormel and the S&P500 shows (click on the chart to view a larger version), the company has actually done rather well over the period. Most of its outperformance seems to have come from its sagging far less than the index when the technology bubble burst at the beginning of this decade. However, it has at least kept pace with the S&P, which is no mean feat.I think the WSJ piece illustrates the pitfalls of listening to CEOs on media venues such as CNBC, and presuming each of them knows what he is doing. Ettinger has had the job only one year, with no external candidates being considered. Taking Hormel into more 'natural' processed food niches would not seem to be a brand-enhancing strategy. Witness Wal-Mart's floundering with its new upscale fashion merchandising strategy this year.Instead, Hormel should probably stick to more brand extensions for Spam, as it has been doing. The company seems to know this consumer segment of older males well, so mining it further is more likely to bring profitable sales than going after young ethnic mothers.Why is the fundamental concept of branding seemingly so difficult for companies tounderstandd? Why do CEOs and group managers attempt to make a successful brand straddle multiple segments which have differing buyer values? How do managers who do this wind up as CEOs?Now there's a question for those interested in shareholder democracy and corporate governance.

As the nearby Yahoo-sourced, five-year price chart of Hormel and the S&P500 shows (click on the chart to view a larger version), the company has actually done rather well over the period. Most of its outperformance seems to have come from its sagging far less than the index when the technology bubble burst at the beginning of this decade. However, it has at least kept pace with the S&P, which is no mean feat.I think the WSJ piece illustrates the pitfalls of listening to CEOs on media venues such as CNBC, and presuming each of them knows what he is doing. Ettinger has had the job only one year, with no external candidates being considered. Taking Hormel into more 'natural' processed food niches would not seem to be a brand-enhancing strategy. Witness Wal-Mart's floundering with its new upscale fashion merchandising strategy this year.Instead, Hormel should probably stick to more brand extensions for Spam, as it has been doing. The company seems to know this consumer segment of older males well, so mining it further is more likely to bring profitable sales than going after young ethnic mothers.Why is the fundamental concept of branding seemingly so difficult for companies tounderstandd? Why do CEOs and group managers attempt to make a successful brand straddle multiple segments which have differing buyer values? How do managers who do this wind up as CEOs?Now there's a question for those interested in shareholder democracy and corporate governance.

There seems to be a lot of media-generated hoopla this week over the increase in Bank of American's market capitalization to exceed that of CitiGroup.

The Money and Investing section of the Wall Street Journal even carried an article yesterday with a chart box headline reading, "There's a new No. 1." CNBC had a special segment featuring Jim Cramer opining on which bank to buy. The network covered the mock "choice" with great fanfare.

To me, this is a silly contest of size between two financial utilities with more similarities than differences. Size of this sort can, and was, purchased. Especially by BofA, which is, in truth, NCNB (which became NationsBank) of Charlotte, which bought the right to rebrand itself with the storied name and logo of the San Francisco takeover victim.

First, let me go on record as stating that the only measure that matters is a longish-term total return for shareholders. As a quick approximation of this, here's a Yahoo-sourced price chart (please click on the chart to see a larger version) of BofA, Citi and the S&P500 for nearly 20 years.

First, let me go on record as stating that the only measure that matters is a longish-term total return for shareholders. As a quick approximation of this, here's a Yahoo-sourced price chart (please click on the chart to see a larger version) of BofA, Citi and the S&P500 for nearly 20 years.

I thought it would be interesting to look at how similar the change in stock prices have been throughout the long period. Since 2000, there hasn't been all that much difference in the slopes of the curves for the two banks. It's clear that whatever outperformance Citi has enjoyed came in the 1998-2000 timeframe.

For clarity, though, here's the same chart, for just the last five years. BofA is clearly superior at having generated superior total returns. It confirms, in greater detail, that Citi's best performance period was more than five years ago.

For clarity, though, here's the same chart, for just the last five years. BofA is clearly superior at having generated superior total returns. It confirms, in greater detail, that Citi's best performance period was more than five years ago.

All this is somewhat interesting, but perhaps misses the point. In five years, the better performing bank of the two only returned roughly 15%, total. Plus dividends. CitiGroup is a little better than flat, and worse than the S&P.

With a performance like this, maybe something should change at Citi.

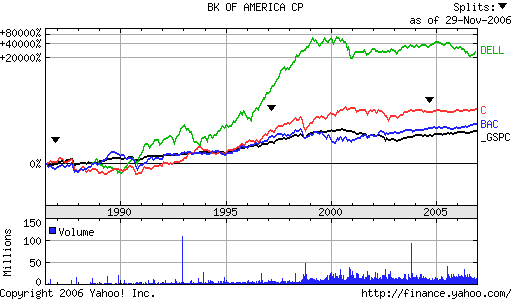

To put this in perspective, let's look at how a fallen growth stock stacks up against these two "large" banks.In this chart, I've added Dell to the earlier long-term comparison of Citi, BofA, and the S&P500.It sort of puts things in perspective for me. All this hue and cry over which bank is larger seems, for me, to rapidly fade into the background, as I see the much larger gain in stock price in Dell over the period. The two banks are literally not even in the same league. Not even after Dell plateaued six years ago.As an investor, I can't say I even care which bank has which market cap. Both have such anemic returns over the last half decade that I doubt my strategy's selection process would include either company in my equity portfolio.Yet another case of entertainment trumping news. The 'news' being, no matter which firm is larger, or how large they get, they still can't deliver consistently superior total returns for their shareholders. If one of them could? Now that would be news to me.

To put this in perspective, let's look at how a fallen growth stock stacks up against these two "large" banks.In this chart, I've added Dell to the earlier long-term comparison of Citi, BofA, and the S&P500.It sort of puts things in perspective for me. All this hue and cry over which bank is larger seems, for me, to rapidly fade into the background, as I see the much larger gain in stock price in Dell over the period. The two banks are literally not even in the same league. Not even after Dell plateaued six years ago.As an investor, I can't say I even care which bank has which market cap. Both have such anemic returns over the last half decade that I doubt my strategy's selection process would include either company in my equity portfolio.Yet another case of entertainment trumping news. The 'news' being, no matter which firm is larger, or how large they get, they still can't deliver consistently superior total returns for their shareholders. If one of them could? Now that would be news to me.

There seems to be a run on the New York Times group, or parts thereof, by retired or 'removed' CEOs.

First Jack Welch & Co. want to pry the Boston Globe away from the company.

Now we learn that AIG former-CEO Hank Greenberg is building a position in the parent company.

What gives with these ex-CEOs going after the NYTimes?

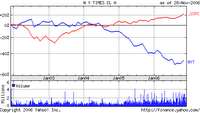

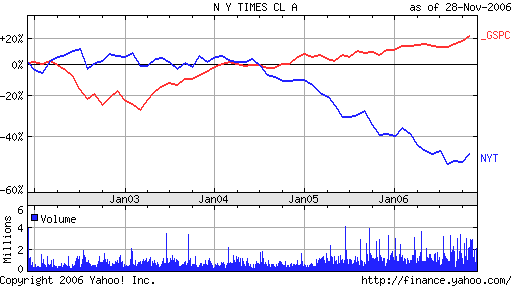

I've pasted a Yahoo-sourced price chart of the NYT vs. the S&P500 Index for the past five years (click on the chart to view the enlarged version). It isn't pretty. The newpaper group is down more than 40% over the period, while the index has risen roughly 20%, for a 60 percentage point difference.

Revenues are shrinking, as are profits. Over the five year period, revenues have oscillated, but finished essentially flat, while profits did about the same. Except for a recent, severe dip.So, why the sudden interest by Greenberg and Welch in these basket case newspapers? Has nobody told them what Google, eBay and Yahoo are doing to the classified ad business of newspapers, as well as general print advertising? Are they unaware that many people receive their news online now, rather than reading a daily paper?What would have to happen to turn these papers around? What is it Welch and Greenberg bring to the table that is missing from current management, or anyone else?I am genuinely curious about why the sudden rush to either buy or dismember the NY Times group. Is it all charity and philanthrophy, to save the jobs of pressmen and beat reporters? Or do Greenberg and Welch see profits where nobody else does?

Yesterday's Wall Street Journal featured a special section on home entertainment. The lead piece focused on Apple's dominance of digital music distribution.According to the article, iPod/iTunes holds a 71% share of the market, while EMusic is second, with only 10%.I can't recall that last time I bought a full-priced CD in a retail store. The last time I bought large numbers of CDs was over six years ago, from the now defunct website, CDNow. That's how much Apple has changed the experience of buying, and playing music.The main point of the Journal's piece on digital music was that none of the also-rans to Apple are trying to take it on directly. Through various approaches involving monthly fees, limited play of free copies of songs, most competitors hope to attract users willing to adopt a different music purchase and/or listening system.Only Microsoft's Zune is configured to be just like the Apple iPods. That is, the pricing and general content acquisition models are similar. However, the Zune is much bulkier than the iPods, looking as if it had been rushed out prematurely for this Christmas season. The article quotes an analyst as believing that Microsoft is the only company capable of taking on Apple directly with a nearly-identical system for music distribution and playing.Looking at the 'music leasing' model of several iPod competitors, I wonder how many of those users feel like I do, and want to own their content? I've never personally been interested in paying to lease music I like for a few months. So, realistically, with such high market penetration by Apple already, I doubt any of them have much long-term potential to earn consistently superior returns with their strategies.As for Microsoft, I see their Zune offering as similar, in a corporate sense, to their XBox division. Microsoft is slowly creating standalone product groups to create new hardware which will pull software along with it. As such, these new groups could just as easily have had different logos and corporate names, even if funded by Microsoft.This is very close to my earlier recommendations for just such a split among the company's disparate units.However, since they remain as Microsoft groups, I can't help but wonder if their potential to earn total returns is lost among the still-huge revenue streams from conventional PC software sales. For all the hype about new directions at Microsoft, and new blood, their corporate form pretty much guarantees that most new initiatives won't be sufficiently large to move the share price, and, thus, total return, needle.Apple by contrast, has a 70% total return just from July. Their nimbleness and focus on growth-oriented product markets is resulting in a much better experience for their shareholders.From what I read in the WSJ yesterday concerning digital music, I don't see any competitors dethroning Apple any time soon. So many consumers have already bought and stored music in the firm's proprietary format, that I just don't expect they will have compelling reasons to switch brands in the near future.

The Saturday/Sunday edition of the Wall Street Journal is typically rather lightweight in content. My partner is of the opinion that much of the edition is filler that wouldn't make the weekday paper.

However, this weekend's "Breaking Views/Insights on Investing" discussed the recent Blackstone private takeover of Equity Office Properties from the perspective of bubble investing.

I admit to having forgotten how the Federated/Campeau fiasco drove then-independent First Boston into the arms of Credit Suisse. The American investment bank had funded Campeau's takeover of Federated stores with a bridge loan which it held, anticipating syndicating the loan among other institutions. First Boston proved unable to do this, and, thus, took the loss as Federated went bankrupt in 1990.

Sixteen years is a long time. Now, Blackstone Group is paying $36B in the largest private equity takeover of all time. According to the WSJ piece, Goldman Sachs and Bank of America are risking some $3.5B of their shareholder's capital by holding a block of the deals equity.

I'm not familiar with the economics of the underlying transaction. Perhaps Blackstone feels that commercial property has bottomed, and now is the time to buy. Or perhaps it just feels that the outlook for commercial property rents and appreciation are more attractive than the market does. Either way, it's a very large move.

Leaving two publicly-held banks, Goldman and BofA, with 10% of the deal's financing of which to dispose, seems peculiarly risky. This is the sort of thing, as the Journal article reminds us, that goes bad in an instant, with no way to recoup the losses. The reason the authors give for this funding move is simply that the fee income from funding this deal is enormous.

That this is an attractive alternative for the two firms suggests the extent to which they now feel they must take capital risks in order to generate income.

And, of course, it probably won't take much of a shadow of uncertainty to cloud the deal's fortunes such that the 'equity block' that these two companies hold declines by far more than the amount of the fees they're booking.

As always, time will tell.......

The recent USAirways bid for Delta has sparked quite a bit of business media comment. Holman Jenkins wrote a good piece on Wednesday in the Wall Street Journal.

Essentially, he notes that US Airways CEO Doug Parker's proposed acquisition "might have been inspired by the old joke about two hunters trying to outrun a bear."

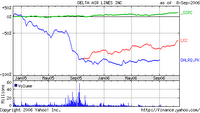

Just so. As the Yahoo-sourced chart of US Airways', Delta's, and the S&P500's prices for the past two years (click on chart to see an enlarged version) illustrates, It is not a merger of two strong competitors.

Delta is in bankruptcy. US Airways is somewhat difficult to track prior to a year or so ago, when, thru a merger, the price trail was more or less obliterated, as America West took US Airways' name.However, in the past year, US Airways has clearly outperformed the S&P, while Delta languishes. Contrary to the pundits who declare that most desirable airline mergers combine non-overlapping airlines, this one promises to help remove excess capacity in similar markets. Which, of course, should firm up pricing for US Airways. Additionally, as Jenkins noted in his piece, it leaves the merged airline with slots at Kennedy and O'Hare, where new entrants have difficulty obtaining gates.So much for the value of the merger.However, the larger issue, to me, is competition in an industry in which so much of the business model is either shared and in common with competitors, or easily obtainable, thus lowering barriers to entry.Specifically, all airlines must, of necessity, use the same airports. Thus, they rely on shared airport management, the FAA, baggage systems, and, in some cases, reservation systems. Anyone with money can start and airline and lease planes from the usual suspects, including GE Capital.Thus, little is left in the control of an airline's management to actually make a sustained difference to customers, for which the latter will pay revenues that drive a consistently superior total return in the market.I've pondered this sector for some time, as Southwest Air is, to my knowledge, the only airline ever to be selected, using my quantitative, disciplined process, for my equity portfolio.This proposed merger does not alter my view. I think in the current market structure, a focus on building a regional strength, with low costs due to common equipment, for maximum use of crews and low training and maintenance costs, are key. The hub and spoke system probably means there are regional physical barriers to airline growth, if the company wishes to enjoy any significant period of consistently superior total returns.Moving beyond that typically sees an airline struggle with expensive logistical issues and traffic feeder/load factor issues.It could well be, thanks to the structure of this sector, that its players are simply unlikely to earn many years of consistently superior total returns.

As the nearby Yahoo-sourced, five-year price chart of Hormel and the S&P500 shows (click on the chart to view a larger version), the company has actually done rather well over the period. Most of its outperformance seems to have come from its sagging far less than the index when the technology bubble burst at the beginning of this decade. However, it has at least kept pace with the S&P, which is no mean feat.

As the nearby Yahoo-sourced, five-year price chart of Hormel and the S&P500 shows (click on the chart to view a larger version), the company has actually done rather well over the period. Most of its outperformance seems to have come from its sagging far less than the index when the technology bubble burst at the beginning of this decade. However, it has at least kept pace with the S&P, which is no mean feat.

{kind=link}