Steve Jobs on Microsoft (Extended Version)

I found this little clip on YouTube the other day, when I was testing the blogging link on that site.

Jobs' accusation of Microsoft's lack of innovative ideas and being cultural philistines doesn't seem to have changed in the years since this interview occurred.

The video clip doesn't have a date, but I'm guessing, by Jobs' look and his references, that it is sometime in the early-mid 1990s.

What I find ironic is that this clip would work today, only for the iPod vs. Microsoft's latest Apple knock-off, the imminent Zune digital music player.

True, Apple stole its Mac OS from Xerox. But what they did with it was inspired and beautiful, if expensive and lacking in troubleshooting capability. Microsoft began its tradition of workmanlike copying of Apple with its Windows OS.

Now, we have the same companies, and the same behaviors, except that this time Apple actually created the digital music download-playing systems itself.

And, of course, this time, the market shares are reversed, and probably will stay that way.

In discussing this with my partner the other day over lunch, I opined that Jobs has already left music playing behind, and is now heading for the higher, virgin ground of digital video content downloading and playing. By the time Microsoft and RealNetworks catch up, Apple will probably have captured the dominant market position, and a proprietary storage method, again.

It's just so eerie that this would all be playing out once more, with the same two companies, and same two leaders, so many years later......

Friday, September 22, 2006

Thursday, September 21, 2006

One Year Anniversary

This month marks my first anniversary writing this blog. Since my first posts, here, beginning on September 15th of 2005, I've written almost 250 pieces.

As I've made this a more routine, daily commentary, my focus has left politics, and focused nearly exclusively on business.

One of the things I've noticed is that writing a daily "column" has sharpened my own sense of the essentials in the business stories on which I comment. It's also helped me to understand how technology has become such a great leveler in recent years. With online publications, cable news, and free online video services such as YouTube, a writer like me is at no disadvantage with respect to news flow, when it comes to selecting topics and having access to information about those topics, on which to opine.

Beyond that, it's also given me many opportunities to test and reinforce my contention, initially born out of my proprietary empirical research, that there are certain hallmarks of companies and sectors that seem to lend themselves to achieving consistently superior returns for their shareholders. Since this is the focus of my companion large-cap equity investment strategy, writing a daily piece for this blog has added a visceral, approachable feel to the rather theoretical notions which originated from my research ten years ago.

If you read this blog regularly, thanks for visiting, and I hope you continue to read and enjoy my work.

As I've made this a more routine, daily commentary, my focus has left politics, and focused nearly exclusively on business.

One of the things I've noticed is that writing a daily "column" has sharpened my own sense of the essentials in the business stories on which I comment. It's also helped me to understand how technology has become such a great leveler in recent years. With online publications, cable news, and free online video services such as YouTube, a writer like me is at no disadvantage with respect to news flow, when it comes to selecting topics and having access to information about those topics, on which to opine.

Beyond that, it's also given me many opportunities to test and reinforce my contention, initially born out of my proprietary empirical research, that there are certain hallmarks of companies and sectors that seem to lend themselves to achieving consistently superior returns for their shareholders. Since this is the focus of my companion large-cap equity investment strategy, writing a daily piece for this blog has added a visceral, approachable feel to the rather theoretical notions which originated from my research ten years ago.

If you read this blog regularly, thanks for visiting, and I hope you continue to read and enjoy my work.

The Business of Entertainment Ticket Sales & Reselling

Tuesday's Wall Street Journal featured an article about the business of selling, and reselling, entertainment event tickets. Ticketmaster, a part of Barry Diller's IAC/Interactive Corp., and the market leader, is portrayed as having reversed its long-held position against reselling, and now trying to cut itself in on scalpers' profits. In fact, many states are now reconsidering, or simply not enforcing, their laws against the resale of tickets for more than $1 above the original price.

The key facet of the business which has brought it to this point is described in a quote by Ticketmaster's chairman, Terry Barnes,

"We're in an industry that prices its product worse than anybody else."

The result is frequently either unfilled stadii, or scalpers realizing healthy profits from underpriced tickets. A revealing statistic is that the estimated sales of tickets in the US secondary market was roughly $5B last year, or nearly Ticketmaster's own revenue from ticket sales.

Now, artists whose events are handled by Ticketmaster complain that more of the end user prices of tickets should belong to them, including the extra revenues from online resales, or "scalping," in general.

In the other "corner" of the competitive ring is a smaller, but significant, rival, StubHub, along with eBay's use for ticket resale auctions. Founded in 2000 by two Stanford Business School graduates, the Journal piece reports that StubHub will have $400MM in ticket sales, double that of 2005, on which it makes 25% for its own revenue.

The two major competitors, Ticketmaster and StubHub, view the "market" in radically different terms. The former sees all end-sale ticket revenues as prospectively belonging to the artist and itself, while the latter views all secondary sales as simply between consumers.

It's hard to fault StubHub. Ticketmaster admits its own pricing strategies are so inept as to leave "5% to 10%, that are priced well below their market value," and a further "over 50% of tickets go unsold." Meaning, taken together, that over half of venue tickets are improperly prices, so as to yield sub-maximal, or no, revenues.

Two similar markets come to mind- IPOs and airline seats. Of the two, IPOs have more than simply revenue maximization as an objective. Typically, the offering is meant to create widespread distribution of shares, so that foregone gains on the day of the initial offering, and later, can be somewhat characterized as a "price" paid by the issuing owners, whose equity is up for sale, in order to create a large and liquid market in the shares for the future.

It's possible that musicians and other entertainers, be they sports figures or others, have similar secondary objectives. However, according to Ticketmaster's new position, it seems like this is ebbing in importance. The company began, in 2003, to auction some tickets online, in an attempt at revenue maximization. Apparently, even this hasn't yet resulted in the successful initial sales of prime seats for desired prices.

This would seem to suggest that the artists, and Ticketmaster, should be calling Bob Crandall's old outfit, American Airlines, to consult with it on yield management for entertainment ticket sales.

On a more basic level, however, it seems that artists are trying to have their cake, and eat it, too. In the past, artists have wanted cash up front to fund them, and allegedly do what they do 'for art's sake.' Until, that is, it pays a lot. Then, it seems, they want the full end sales value of the seats for their events, without the risk of that value being less than they might get upfront via the current process.

But if they want the money, shouldn't entertainers take the risk of unsold seats? Cashflow risk? Timing of sales risk?

Why should Ticketmaster and the entertainers they represent get scalper's prices without the risks?

Painters don't get a cut of their painting's eventual high prices, if their canvases ultimately trade for much higher sums among and between collectors.

I think StubHub is correct on this one. Ticketmaster, it points out, brokers deals for artists to play venues. The ticket seller estimates what to charge for tickets, and artists get a cut. However pricing is done, it is their choice.

Would Ticketmaster, the venue, and artists all be OK with a simple online bidding process? Reserving the timing of various tickets for maximum yield? Calling on an airline for help with yield management of the scarce and perishable inventory of event tickets?

On one hand, they may realize better ticket sales by volume and percentage of seats, as well as total revenues. On the other hand, Ticketmaster's stable of entertainers may lose fans, as they are seen as directly involved and complicit in the move to a total auction market for live performance tickets, possibly moving most tickets beyond the price range of many of their fans.

Doesn't it really boil down to the opening quote by Ticketmaster's chairman? The company appears to simply be inept at a key operating function, price setting and yield management, in its major business line, selling tickets to venue seating for its entertainment clients.

The key facet of the business which has brought it to this point is described in a quote by Ticketmaster's chairman, Terry Barnes,

"We're in an industry that prices its product worse than anybody else."

The result is frequently either unfilled stadii, or scalpers realizing healthy profits from underpriced tickets. A revealing statistic is that the estimated sales of tickets in the US secondary market was roughly $5B last year, or nearly Ticketmaster's own revenue from ticket sales.

Now, artists whose events are handled by Ticketmaster complain that more of the end user prices of tickets should belong to them, including the extra revenues from online resales, or "scalping," in general.

In the other "corner" of the competitive ring is a smaller, but significant, rival, StubHub, along with eBay's use for ticket resale auctions. Founded in 2000 by two Stanford Business School graduates, the Journal piece reports that StubHub will have $400MM in ticket sales, double that of 2005, on which it makes 25% for its own revenue.

The two major competitors, Ticketmaster and StubHub, view the "market" in radically different terms. The former sees all end-sale ticket revenues as prospectively belonging to the artist and itself, while the latter views all secondary sales as simply between consumers.

It's hard to fault StubHub. Ticketmaster admits its own pricing strategies are so inept as to leave "5% to 10%, that are priced well below their market value," and a further "over 50% of tickets go unsold." Meaning, taken together, that over half of venue tickets are improperly prices, so as to yield sub-maximal, or no, revenues.

Two similar markets come to mind- IPOs and airline seats. Of the two, IPOs have more than simply revenue maximization as an objective. Typically, the offering is meant to create widespread distribution of shares, so that foregone gains on the day of the initial offering, and later, can be somewhat characterized as a "price" paid by the issuing owners, whose equity is up for sale, in order to create a large and liquid market in the shares for the future.

It's possible that musicians and other entertainers, be they sports figures or others, have similar secondary objectives. However, according to Ticketmaster's new position, it seems like this is ebbing in importance. The company began, in 2003, to auction some tickets online, in an attempt at revenue maximization. Apparently, even this hasn't yet resulted in the successful initial sales of prime seats for desired prices.

This would seem to suggest that the artists, and Ticketmaster, should be calling Bob Crandall's old outfit, American Airlines, to consult with it on yield management for entertainment ticket sales.

On a more basic level, however, it seems that artists are trying to have their cake, and eat it, too. In the past, artists have wanted cash up front to fund them, and allegedly do what they do 'for art's sake.' Until, that is, it pays a lot. Then, it seems, they want the full end sales value of the seats for their events, without the risk of that value being less than they might get upfront via the current process.

But if they want the money, shouldn't entertainers take the risk of unsold seats? Cashflow risk? Timing of sales risk?

Why should Ticketmaster and the entertainers they represent get scalper's prices without the risks?

Painters don't get a cut of their painting's eventual high prices, if their canvases ultimately trade for much higher sums among and between collectors.

I think StubHub is correct on this one. Ticketmaster, it points out, brokers deals for artists to play venues. The ticket seller estimates what to charge for tickets, and artists get a cut. However pricing is done, it is their choice.

Would Ticketmaster, the venue, and artists all be OK with a simple online bidding process? Reserving the timing of various tickets for maximum yield? Calling on an airline for help with yield management of the scarce and perishable inventory of event tickets?

On one hand, they may realize better ticket sales by volume and percentage of seats, as well as total revenues. On the other hand, Ticketmaster's stable of entertainers may lose fans, as they are seen as directly involved and complicit in the move to a total auction market for live performance tickets, possibly moving most tickets beyond the price range of many of their fans.

Doesn't it really boil down to the opening quote by Ticketmaster's chairman? The company appears to simply be inept at a key operating function, price setting and yield management, in its major business line, selling tickets to venue seating for its entertainment clients.

Wednesday, September 20, 2006

Conglomerates' Value-Added: Another Perspective

Last week's WSJ article about United Technology's new corporate ad campaign caught my attention.

The topic is an old one, going back at least as far as my own graduate business school education in the late 1970s. In that sense, nothing in the piece was really "new" That is, how does a conglomerate provide a clear presence to the market for itself? And is it even necessary?

However, times have changed since I was a grad student, in that, now, a publicly-held company's long-term success measure is usually its total return.

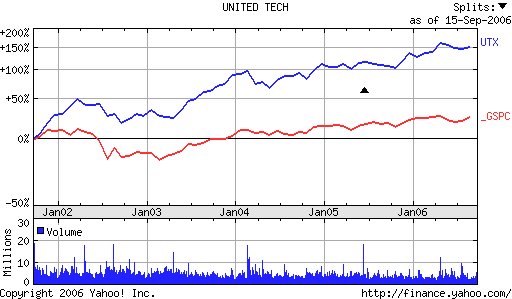

So, the first thing I did, upon reading the piece, was to call up the Yahoo five-year price chart for UTC and the S&P500. That chart is displayed on the left.

So, the first thing I did, upon reading the piece, was to call up the Yahoo five-year price chart for UTC and the S&P500. That chart is displayed on the left.

It's clear that UTC has nothing to worry about. The company's five-year performance is vastly superior to that of the index, and has had no significant downturns which lasted more than a few months.

Why waste money on corporate advertising, when the investors are getting such stupendous returns? Exactly who needs to know about UTC, the conglomerate, when the constituent businesses are delivering such surprisingly consistently superior performance?

It would seem that being a conglomerate is not, in this case, hurting UTC at all.

What is George David's, UTC CEO's, purpose in this matter? How will spending the planned $20 million affect the company's performance?

If UTC had stellar financial operating performance, but poor total returns, it might be different. But that's not the case.

And citing GE as an example of what it wants to emulate seems misguided, too. GE's returns have been abysmal under its CEO, Jeff Immelt, for five years.

Perhaps George David should save the $20MM for product development, and continue to improve his chances of continuing the difficult task of earning consistently superior total returns for his shareholders.

The topic is an old one, going back at least as far as my own graduate business school education in the late 1970s. In that sense, nothing in the piece was really "new" That is, how does a conglomerate provide a clear presence to the market for itself? And is it even necessary?

However, times have changed since I was a grad student, in that, now, a publicly-held company's long-term success measure is usually its total return.

So, the first thing I did, upon reading the piece, was to call up the Yahoo five-year price chart for UTC and the S&P500. That chart is displayed on the left.

So, the first thing I did, upon reading the piece, was to call up the Yahoo five-year price chart for UTC and the S&P500. That chart is displayed on the left.It's clear that UTC has nothing to worry about. The company's five-year performance is vastly superior to that of the index, and has had no significant downturns which lasted more than a few months.

Why waste money on corporate advertising, when the investors are getting such stupendous returns? Exactly who needs to know about UTC, the conglomerate, when the constituent businesses are delivering such surprisingly consistently superior performance?

It would seem that being a conglomerate is not, in this case, hurting UTC at all.

What is George David's, UTC CEO's, purpose in this matter? How will spending the planned $20 million affect the company's performance?

If UTC had stellar financial operating performance, but poor total returns, it might be different. But that's not the case.

And citing GE as an example of what it wants to emulate seems misguided, too. GE's returns have been abysmal under its CEO, Jeff Immelt, for five years.

Perhaps George David should save the $20MM for product development, and continue to improve his chances of continuing the difficult task of earning consistently superior total returns for his shareholders.

Tuesday, September 19, 2006

Rhapsody, iTunes, Zune and The Evolving Competitive Market for Digital Media Downloads

It seems that there is now a concerted effort by both RealNetworks and Microsoft to enter the integrated digital music device and download service market.

According to Monday's Wall Street Journal article, both companies are eyeing Apple's 75% share of a market which accounted for $1.5B in revenues for the company in just the last quarter. The firm has, according to the WSJ, sold 60 million iPods since the product line's introduction.

That must be nearly, on average, one per household in the US. Not that all sales are in the US, but as a benchmark, it's a huge installed base penetration for the device and its companion download service.

There's a really good quote in the article by Mike McGuire, an analyst with the Gartner Group,

"You've got to come to the party with something pretty special."

RealNetworks' Rhapsody service is more or less a musical rental business model. One pays a monthly subscription to keep downloaded material activated. Rhapsody will now work with SanDisk's Sansa player, the leading rival company to Apple in this market.

Microsoft is now approaching the product/market in the same manner as it did the XBox360, and with the same senior executives responsible for this new digital music/media business group. Rather than rely on outside developers, they are now mirroring Apple's total system provision of a player, the Zune, and its own net-based downloading service.

Apple has had this market largely to itself for at least five years. It's prices are very low now. Even more than a year ago, they had penetrated the lower end of the market with a $100, 512KB Shuffle. I can't see anyone undercutting them on price.

So it's difficult to see just what is left in the marketplace for Microsoft and RealNetworks to serve with significantly superior or different, value-adding functions and features.

In Microsoft's case, I'd even go so far as to suggest that this may mark their second major step toward dis-integrating the monolith that has been the Redmond software titan. As I opined to my consulting friend, S, some months ago, I think that way lies any hope of rescue and financial success for Microsoft.

From what I've read, there is no mention of the Xbox or Zune being integrated into or with other Microsoft products, notably Windows. But I don't know if wireless transfers of music is enough to dethrone Apple after a five-year headstart.

It will likely come down to a preference for the online interface experience. Or perhaps upgrading and replacing an older player with the same brand, in order to keep one's music library intact. Funny how well-designed products just naturally promote legal and profitable tying.

In the final analysis, based on what I've read so far, Apple doesn't have much to worry about in the near term. They've made their platform into a multi-media one, from simply music, in order to facilitate future growth. And adeptly sidestep competition from pure music players.

If this is the best RealNetworks and Microsoft can do, they may be in for a bad time in the digital media device and download product/market.

According to Monday's Wall Street Journal article, both companies are eyeing Apple's 75% share of a market which accounted for $1.5B in revenues for the company in just the last quarter. The firm has, according to the WSJ, sold 60 million iPods since the product line's introduction.

That must be nearly, on average, one per household in the US. Not that all sales are in the US, but as a benchmark, it's a huge installed base penetration for the device and its companion download service.

There's a really good quote in the article by Mike McGuire, an analyst with the Gartner Group,

"You've got to come to the party with something pretty special."

RealNetworks' Rhapsody service is more or less a musical rental business model. One pays a monthly subscription to keep downloaded material activated. Rhapsody will now work with SanDisk's Sansa player, the leading rival company to Apple in this market.

Microsoft is now approaching the product/market in the same manner as it did the XBox360, and with the same senior executives responsible for this new digital music/media business group. Rather than rely on outside developers, they are now mirroring Apple's total system provision of a player, the Zune, and its own net-based downloading service.

Apple has had this market largely to itself for at least five years. It's prices are very low now. Even more than a year ago, they had penetrated the lower end of the market with a $100, 512KB Shuffle. I can't see anyone undercutting them on price.

So it's difficult to see just what is left in the marketplace for Microsoft and RealNetworks to serve with significantly superior or different, value-adding functions and features.

In Microsoft's case, I'd even go so far as to suggest that this may mark their second major step toward dis-integrating the monolith that has been the Redmond software titan. As I opined to my consulting friend, S, some months ago, I think that way lies any hope of rescue and financial success for Microsoft.

From what I've read, there is no mention of the Xbox or Zune being integrated into or with other Microsoft products, notably Windows. But I don't know if wireless transfers of music is enough to dethrone Apple after a five-year headstart.

It will likely come down to a preference for the online interface experience. Or perhaps upgrading and replacing an older player with the same brand, in order to keep one's music library intact. Funny how well-designed products just naturally promote legal and profitable tying.

In the final analysis, based on what I've read so far, Apple doesn't have much to worry about in the near term. They've made their platform into a multi-media one, from simply music, in order to facilitate future growth. And adeptly sidestep competition from pure music players.

If this is the best RealNetworks and Microsoft can do, they may be in for a bad time in the digital media device and download product/market.

Monday, September 18, 2006

Energy Prices, Investors and the Economy and Markets

This has been a rather peculiar year for equity investing. Last week's Wall Street Journal, on Wednesday, featured two articles on disappointing investment performance at two very well-regarded firms- Goldman Sachs and Convexity Capital.

Our own equity strategy is doing poorly at the moment, as a result of energy prices, and investors' near term reactions to those prices.

My partner emailed me a recent NY Times piece which repeated many of the comments I've made regarding this situation. It is, to me, perplexing.

First, it's notable that so many hedge funds and veteran managers are doing poorly as well this year. It's not really a "growth" economy, so far as investors perceive it. The S&P500 Index has not had a monthly closing annual return above 6% yet this year. Many have been below 4%. Hardly a year of confident investing in a growing economy.

Which brings us to energy. The track record of energy firms which have entered our portfolio is one of consistently superior revenue growth and total returns for quite a few years. They are not simply timing bets on oil and gas prices. However, this year, more than even last year, has really caused confusion in the energy markets.

If economies are growing, then investors fear the Fed raising rates to check inflationary pressures. Pressures brought on by......energy prices! Rising rates will slow the economy. And lead to less energy usage.

If economies are slowing, investors feel energy will be in less demand, and, thus, have less value. As will, they feel, the companies producing and distributing the necessary fuels and their precursors.

It would seem that, for now, and for much of the past few months, the broad middle swathe of "average" investors, and I use the term pejoratively, feel that it is an inescapable conclusion that any probably economic outcome must lead to lower growth and lower energy prices, and, thus, lower prices for energy company equities.

To be sure, the way the S&P has bumped along near zero returns for so much of this year, and in the low single-digits the rest of the time, doesn't help. Nevermind that real economic growth has been pretty good for more than two years now. And that, per Arthur Laffer's comments recently, related in this post, we aren't seeing inflationary pressures, so much as the effects of commodity prices filtered through exchange rates.

I just don't see an economic recession among the various better pundits who forecast such things. ChIndia still seems to be growing and planning to consume copious amounts of energy. No imminent additions to supply are in sight, and demand doesn't seem to have materially slowed. True, current inventories are high for oil, gasoline and natural gas. Is this a long-term effect, or simply a snapshot in the early fall? Is it truly the basis for long-term declines in energy prices?

Granted, Chevron and Devon have announced a large new find in the deep waters of the Gulf of Mexico. As the NYTimes article my partner sent me, written by Daniel Akst reminds us,

"WhatÂ’s that you say? You think this sounds like good news rather than bad? You figure cheaper oil would boost economic growth while slashing the income of such lovable oil exporters as Iran?

Don’t kid yourself. Anything that reinforces the role of fossil fuels — particularly oil — as the industrial world’s primary energy source is bad, not good. Anything that prolongs the life of the internal combustion engine is a negative, not a positive. Anything that makes it cheaper to pump greenhouse gases into the atmosphere is cause for mourning rather than celebration.What we need is not lower oil prices but higher ones — significantly higher, enough to deter consumption and make us look seriously at alternatives........HIGHER prices have worked wonders before. Today, Americans can generate a dollar of gross domestic product using just half the energy required in 1973, that watershed year of the oil embargo and lines at gas stations. In countries where energy is more expensive, a dollar of G.D.P. requires considerably less energy still. Unlike a tax, moreover, higher prices have the advantage of applying all over the world, to everyone."

The point about the growth in US productivity with respect to oil is a fact I like to quote. However, the correspoinformationmation about countries where energy is even more expensive was welcome news to me.

It's a tumultuous time in the equity markets, and the energy markets, to be sure. Occurring at such relatively modest market returns, with questions about inflation, growth and recession in the air, all of this has a depressing effect on growth equity strategies.

I'm not completely sold on the idea that energy prices are down for the count, and their equity prices, with them. For a while, I do believe the weight of average market participants will continue to keep prices low. But it won't take much to send both commodity prices, and those of their producers, rocketing upwards again, once the broad, "average" investors, meinstitutionaltional managers, realize that supply and demand fundamentals of energy have not changed materially in the last twelve months.

Our own equity strategy is doing poorly at the moment, as a result of energy prices, and investors' near term reactions to those prices.

My partner emailed me a recent NY Times piece which repeated many of the comments I've made regarding this situation. It is, to me, perplexing.

First, it's notable that so many hedge funds and veteran managers are doing poorly as well this year. It's not really a "growth" economy, so far as investors perceive it. The S&P500 Index has not had a monthly closing annual return above 6% yet this year. Many have been below 4%. Hardly a year of confident investing in a growing economy.

Which brings us to energy. The track record of energy firms which have entered our portfolio is one of consistently superior revenue growth and total returns for quite a few years. They are not simply timing bets on oil and gas prices. However, this year, more than even last year, has really caused confusion in the energy markets.

If economies are growing, then investors fear the Fed raising rates to check inflationary pressures. Pressures brought on by......energy prices! Rising rates will slow the economy. And lead to less energy usage.

If economies are slowing, investors feel energy will be in less demand, and, thus, have less value. As will, they feel, the companies producing and distributing the necessary fuels and their precursors.

It would seem that, for now, and for much of the past few months, the broad middle swathe of "average" investors, and I use the term pejoratively, feel that it is an inescapable conclusion that any probably economic outcome must lead to lower growth and lower energy prices, and, thus, lower prices for energy company equities.

To be sure, the way the S&P has bumped along near zero returns for so much of this year, and in the low single-digits the rest of the time, doesn't help. Nevermind that real economic growth has been pretty good for more than two years now. And that, per Arthur Laffer's comments recently, related in this post, we aren't seeing inflationary pressures, so much as the effects of commodity prices filtered through exchange rates.

I just don't see an economic recession among the various better pundits who forecast such things. ChIndia still seems to be growing and planning to consume copious amounts of energy. No imminent additions to supply are in sight, and demand doesn't seem to have materially slowed. True, current inventories are high for oil, gasoline and natural gas. Is this a long-term effect, or simply a snapshot in the early fall? Is it truly the basis for long-term declines in energy prices?

Granted, Chevron and Devon have announced a large new find in the deep waters of the Gulf of Mexico. As the NYTimes article my partner sent me, written by Daniel Akst reminds us,

"WhatÂ’s that you say? You think this sounds like good news rather than bad? You figure cheaper oil would boost economic growth while slashing the income of such lovable oil exporters as Iran?

Don’t kid yourself. Anything that reinforces the role of fossil fuels — particularly oil — as the industrial world’s primary energy source is bad, not good. Anything that prolongs the life of the internal combustion engine is a negative, not a positive. Anything that makes it cheaper to pump greenhouse gases into the atmosphere is cause for mourning rather than celebration.What we need is not lower oil prices but higher ones — significantly higher, enough to deter consumption and make us look seriously at alternatives........HIGHER prices have worked wonders before. Today, Americans can generate a dollar of gross domestic product using just half the energy required in 1973, that watershed year of the oil embargo and lines at gas stations. In countries where energy is more expensive, a dollar of G.D.P. requires considerably less energy still. Unlike a tax, moreover, higher prices have the advantage of applying all over the world, to everyone."

The point about the growth in US productivity with respect to oil is a fact I like to quote. However, the correspoinformationmation about countries where energy is even more expensive was welcome news to me.

It's a tumultuous time in the equity markets, and the energy markets, to be sure. Occurring at such relatively modest market returns, with questions about inflation, growth and recession in the air, all of this has a depressing effect on growth equity strategies.

I'm not completely sold on the idea that energy prices are down for the count, and their equity prices, with them. For a while, I do believe the weight of average market participants will continue to keep prices low. But it won't take much to send both commodity prices, and those of their producers, rocketing upwards again, once the broad, "average" investors, meinstitutionaltional managers, realize that supply and demand fundamentals of energy have not changed materially in the last twelve months.

Subscribe to:

Posts (Atom)