Monday's Wall Street Journal's "Theory & Practice" column featured a concept known as "net promoter." According to columnist Scott Thurm, the concept is "advocated by consulting firm Bain & Co., market researcher Satmetrix Systems, and author Fred Reichheld." Reichheld is a director emeritus at Bain & Co.

Apparently, the essence of the concept is to assess, on a 0-10 scale, customer responses to the question,

"How likely is it that you would recommend us to a friend or colleague?"

The high values (9-10) are "promoters," middle values (7-8) are deemed "passives," while the lower values (0-6) are considered "detractors." A "net-promoter score" is determined by "subtracting detractors from promoters." Whether that is in aggegrate, then taking an average, or by some other method, is not specified in the article.

In his column, Thurm discusses an emerging debate regarding whether or not the net promoter concept is effective for predicting revenue growth and "other customer satisfaction measures."

A Neil Morgan, assistant professor of Marketing at Indiana University, is quoted as saying,

"Does this thing predict business performance (my bold) or not?....There is no evidence that it does."

Without an explicit and defensible definition of "business performance," I'd say Mr. Morgan's comment is rather obvious, wouldn't you? The article goes on to state that Reichheld claimed, in a book, that, "on average, a 12-point increase in a company's net-promoter score doubles its growth rate." Apparently, Bain has now backed away from the claim. Not a good sign, eh?

Among the measure's supporters is, we are told, no less than Jeff Immelt, the continually-underperforming CEO of GE. This alone would make me suspect of the concept. Foundering large companies are not the best place to look for testimonials on a new management concept. When combined with the Bain backpedaling, I'd take this concept's value as a quantitative, or explanatory variable, with a grain of salt.

What I find curious is why nobody has thought to study the relationship between promoter scores, net-promoter scores, and total returns. I'd have to know more about the time dimension over which one can apply the promoter scores before associating it with a company's consistency of superior total return over time, but the question interests me greatly.

As a marketer by training and initial business experience, I find the basic idea interesting, and potentially useful. However, even after Googling the term "net promoter concept," and reading through this Bain webpage, I am at a loss as to know precisely how one "subtracts" the promoter scores from the detractor scores. Are they averaged? Normalized? Over what sample size? Time period?

The Phelon Group, mentioned in the Journal column, describes its own proprietary approach to operationalizing the concept here.

To simply measure a sort of 'recommended buy/rebuy' rate, at the extremes, where really passionate advocates or detractors will operate, makes intuitive sense. But, to quantify the effect, I would think you'd need to relate it, once you understand how to actually work with the measure, to a company's overall success in creating shareholder value over time, i.e., consistently superior total returns. It seems, though, at this point in time, that the mechanics and interpretations of the basic measure still constitute what might be termed an "art form."

Regardless of which method one uses to operationalize this concept, I would reserve judgment on its being anything more than another passing fad, until I see some solid research relating it to a company's ability to consistently earn superior total returns for its shareholders.

Friday, December 08, 2006

Thursday, December 07, 2006

Yahoo's Reorganization: Rearranging the Deck(er?) Chairs

Today's Wall Street Journal contains an article reporting on the Yahoo reorganization announced yesterday. For what it's worth, the story didn't make any of the three major columns on page one. Nor the top half of the stories listed in the center columns "What's News." Nor any editorial regarding the major shake-up.

Late last month, I wrote a piece commenting on the recently-publicized internal strife regarding Yahoo's lackluster performance. Back in August, I wrote this one, which highlighted the firm's strategic malaise. In that light, I would have to say that this reorganization looks bad. Gender notwithstanding, I think it's rare that having a CFO become a major operating executive is a good thing for a growth business. Yet, this is what Semel is doing, by adding line responsibilities to CFO Susan Decker's plate. Most CFOs, if they are good at what they do, don't really have a growth or creative mindset. If they do, then what the heck are they doing in a sombre suit (or dress/skirt) as CFO?

Further, the mass exodus of top managers notwithstanding, Terry Semel, who brought you these past years of wayward performance, is still running the show. This looks very, very bad.

The best that the Journal could come up with about Decker is a Yahoo spokeswoman's remark,

"If anyone can do it, I'm sure it's Sue Decker."

Well, what else would you expect a company spokeswoman to say- "We're not expecting much, but she's already here, so, what the heck?"

Rather, the WSJ piece is decidedly guarded on its review of Decker's career. As I contended last year, regarding GM and Ford, and, on an ongoing basis, GE, I smell the whiff of 'careful what you write about this person, she may soon be CEO of a large, if mediocre, online corporation from whom we'll want advertising, and to whom we'll want access.' The report is full of pulled punches about Decker's lack of any past operating success, much less experience. And that she is, basically, a one-time equity analyst cum corporate finance functionary.

In her new position, Ms. Decker will be responsible for Yahoo's "main revenue-generating activities, including its sales of online advertising for Yahoo and partner sites." The move is reported to be, in some observers' opinions, "a test of her fitness to succeed Chief Executive Terry Semel, 63 years old, upon his retirement."

Blogger is not cooperating with my attempt to paste a Yahoo-sourced (ironic, yes?) chart of stock price performance for Yahoo, Google and the S&P500 for an extended time period. It shows that, for the five years since Semel took over the firm, it has not actually outperformed the index, thanks to a precipitous fall in the stock price back in 2001. Since Google went public, it has easily outperformed Yahoo.

Thus, one might question whether any parts of the Semel-led team are capable of fixing what is wrong with Yahoo. As the 'peanut-butter manifesto' alleged, supporting my earlier observations, the firm has a mediocre presence in many online areas, but a commanding one nowhere.

Will Susan Decker and Jeff Weiner be fixing this shortcoming?

With problems of the scope and duration that Yahoo has, it's telling that the board did not intervene to replace Semel and his team with a new, more creative crew which is not wedded to the firm's past errors.

As it stands now, this reorganization, with Semel still in place, looks like rearranging the deck chairs on the Titanic.

As always, time will tell. Glad I'm not a passenger on this voyage.....

Late last month, I wrote a piece commenting on the recently-publicized internal strife regarding Yahoo's lackluster performance. Back in August, I wrote this one, which highlighted the firm's strategic malaise. In that light, I would have to say that this reorganization looks bad. Gender notwithstanding, I think it's rare that having a CFO become a major operating executive is a good thing for a growth business. Yet, this is what Semel is doing, by adding line responsibilities to CFO Susan Decker's plate. Most CFOs, if they are good at what they do, don't really have a growth or creative mindset. If they do, then what the heck are they doing in a sombre suit (or dress/skirt) as CFO?

Further, the mass exodus of top managers notwithstanding, Terry Semel, who brought you these past years of wayward performance, is still running the show. This looks very, very bad.

The best that the Journal could come up with about Decker is a Yahoo spokeswoman's remark,

"If anyone can do it, I'm sure it's Sue Decker."

Well, what else would you expect a company spokeswoman to say- "We're not expecting much, but she's already here, so, what the heck?"

Rather, the WSJ piece is decidedly guarded on its review of Decker's career. As I contended last year, regarding GM and Ford, and, on an ongoing basis, GE, I smell the whiff of 'careful what you write about this person, she may soon be CEO of a large, if mediocre, online corporation from whom we'll want advertising, and to whom we'll want access.' The report is full of pulled punches about Decker's lack of any past operating success, much less experience. And that she is, basically, a one-time equity analyst cum corporate finance functionary.

In her new position, Ms. Decker will be responsible for Yahoo's "main revenue-generating activities, including its sales of online advertising for Yahoo and partner sites." The move is reported to be, in some observers' opinions, "a test of her fitness to succeed Chief Executive Terry Semel, 63 years old, upon his retirement."

Blogger is not cooperating with my attempt to paste a Yahoo-sourced (ironic, yes?) chart of stock price performance for Yahoo, Google and the S&P500 for an extended time period. It shows that, for the five years since Semel took over the firm, it has not actually outperformed the index, thanks to a precipitous fall in the stock price back in 2001. Since Google went public, it has easily outperformed Yahoo.

Thus, one might question whether any parts of the Semel-led team are capable of fixing what is wrong with Yahoo. As the 'peanut-butter manifesto' alleged, supporting my earlier observations, the firm has a mediocre presence in many online areas, but a commanding one nowhere.

Will Susan Decker and Jeff Weiner be fixing this shortcoming?

With problems of the scope and duration that Yahoo has, it's telling that the board did not intervene to replace Semel and his team with a new, more creative crew which is not wedded to the firm's past errors.

As it stands now, this reorganization, with Semel still in place, looks like rearranging the deck chairs on the Titanic.

As always, time will tell. Glad I'm not a passenger on this voyage.....

Wednesday, December 06, 2006

On The Utility of Publicly Available Information

Last week, the Wall Street Journal ran a feature article concerning the private research coordination business founded and managed by Mark Gerson.

It reminded me of a one-time analyst and money manager I knew years ago who broke into the business in a similar way. Though his network of contacts among retail packaged goods salesmen, he had access to what was, at that time, essentially instantaneous field sales reports. By offering his analytical services free for a few months, he secured a prized research post at a mid-sized broker.

Gerson's business does this on a larger scale, by brokering purveyors of such private intelligence, with those who would like to have it, but don't know the right people. Among his clientele on the buying side are, apparently, legions of hedge funds, who want up to date information on grass roots sales results and field performance of various products and services.

Some way into the piece, the author quotes a private investment firm's partner as saying,

"What's in the public domain is worthless in terms of making money."

Strong words, indeed. And, as it turns out, wrong.

My own experience, using only Compustat data, is that an effectively constructed equity strategy can consistently outperform the S&P500 without using 'private' data. The equity strategy that I have built, refined and managed over many years has consistently outperformed the index, using only Compustat-sourced data. A look at some of the information on the companion website to this blog will give you some idea of what I mean.

My guess is, the investment firm partner who was quoted in the article focuses on very short time periods, and is primarily involved in trading, as opposed to investing. It never fails to amaze me that so many institutional 'investors' feel they must have 'non-public' information, in order to outperform the market.

Rarely, it seems, do investment managers consider building more potent selection processes, which incorporate understandings of the investors' behaviors, as filtered through market outcomes. Perhaps because, as author and fund manager James O'Shaughnessy points out, so few people are disciplined, the concept of consistently using an approach which is carefully developed to take investors' behaviors into account is simply unworkable. Their animal passions and emotions take over, negating whatever value there is in allowing a well-developed selection and management strategy to operate as intended.

It has continally surprised me that one can outperform a major market index simply by carefully, consistently observing and processing regularly-recurring public data. You'd think that anything so widely available would necessarily have no value, as the quote's author seems to think.

However, the reality seems to be that, with so much data about companies and markets available, knowing just 'which' data may provide key insights is less obvious than you may think. And knowing how to evaluate, or analyze it, appears to be more arcane than you might think, as well.

It reminded me of a one-time analyst and money manager I knew years ago who broke into the business in a similar way. Though his network of contacts among retail packaged goods salesmen, he had access to what was, at that time, essentially instantaneous field sales reports. By offering his analytical services free for a few months, he secured a prized research post at a mid-sized broker.

Gerson's business does this on a larger scale, by brokering purveyors of such private intelligence, with those who would like to have it, but don't know the right people. Among his clientele on the buying side are, apparently, legions of hedge funds, who want up to date information on grass roots sales results and field performance of various products and services.

Some way into the piece, the author quotes a private investment firm's partner as saying,

"What's in the public domain is worthless in terms of making money."

Strong words, indeed. And, as it turns out, wrong.

My own experience, using only Compustat data, is that an effectively constructed equity strategy can consistently outperform the S&P500 without using 'private' data. The equity strategy that I have built, refined and managed over many years has consistently outperformed the index, using only Compustat-sourced data. A look at some of the information on the companion website to this blog will give you some idea of what I mean.

My guess is, the investment firm partner who was quoted in the article focuses on very short time periods, and is primarily involved in trading, as opposed to investing. It never fails to amaze me that so many institutional 'investors' feel they must have 'non-public' information, in order to outperform the market.

Rarely, it seems, do investment managers consider building more potent selection processes, which incorporate understandings of the investors' behaviors, as filtered through market outcomes. Perhaps because, as author and fund manager James O'Shaughnessy points out, so few people are disciplined, the concept of consistently using an approach which is carefully developed to take investors' behaviors into account is simply unworkable. Their animal passions and emotions take over, negating whatever value there is in allowing a well-developed selection and management strategy to operate as intended.

It has continally surprised me that one can outperform a major market index simply by carefully, consistently observing and processing regularly-recurring public data. You'd think that anything so widely available would necessarily have no value, as the quote's author seems to think.

However, the reality seems to be that, with so much data about companies and markets available, knowing just 'which' data may provide key insights is less obvious than you may think. And knowing how to evaluate, or analyze it, appears to be more arcane than you might think, as well.

Tuesday, December 05, 2006

Kerkorian On Diversification

In this weekend's article on Kirk Kerkorian, the Wall Street Journal quoted him on the topic of diversification as saying,

"Diversification is for people who aren't sure about what they are doing."

This caught my attention, because my portfolio periodically becomes concentrated in companies in certain sectors, causing consternation among potential investors.

For example, several years ago, as the housing market was in a healthy growth mode, I held a significant percentage of the portfolio in several home builders and financing institutions. While discussing the strategy with several representatives of investing institutions, I was criticized for this concentration. My explanation that was unlikely to earn above-market returns simply through diversification fell on deaf ears. As Kerkorian observes, these people, not being investors themselves, but merely analysts, were more interested in risk avoidance than actually earning returns.

A similar situation exists when hedge funds engage in long/short allocations. That is, they may only be 70% long, and 30% short, in order to, they believe, mitigate risks of extreme losses. I have had discussions with people at such funds, who have told me that any all-long or all-short positions add no value over that of a mutual fund. To them, apparently, the value of a 'hedge' fund is in the hedging.

In reality, though, the proof is in the performance. If one is confident that a market environment is supportive of an all-long position for one's strategy, then one should be long. In that respect, I feel that Kerkorian's view is correct. Managers often hedge because they are simply unsure whether to be long, or short.

I think that sometimes, people can make a situation far more complicated than it need be. Kerkorian's remark reminds us that it's not always necessary to diversify. There are times when you have a specific objective, knowledge of a situation, and are able to reap profits because of your concentrated efforts, rather than diluting them via diversification.

"Diversification is for people who aren't sure about what they are doing."

This caught my attention, because my portfolio periodically becomes concentrated in companies in certain sectors, causing consternation among potential investors.

For example, several years ago, as the housing market was in a healthy growth mode, I held a significant percentage of the portfolio in several home builders and financing institutions. While discussing the strategy with several representatives of investing institutions, I was criticized for this concentration. My explanation that was unlikely to earn above-market returns simply through diversification fell on deaf ears. As Kerkorian observes, these people, not being investors themselves, but merely analysts, were more interested in risk avoidance than actually earning returns.

A similar situation exists when hedge funds engage in long/short allocations. That is, they may only be 70% long, and 30% short, in order to, they believe, mitigate risks of extreme losses. I have had discussions with people at such funds, who have told me that any all-long or all-short positions add no value over that of a mutual fund. To them, apparently, the value of a 'hedge' fund is in the hedging.

In reality, though, the proof is in the performance. If one is confident that a market environment is supportive of an all-long position for one's strategy, then one should be long. In that respect, I feel that Kerkorian's view is correct. Managers often hedge because they are simply unsure whether to be long, or short.

I think that sometimes, people can make a situation far more complicated than it need be. Kerkorian's remark reminds us that it's not always necessary to diversify. There are times when you have a specific objective, knowledge of a situation, and are able to reap profits because of your concentrated efforts, rather than diluting them via diversification.

Sunday, December 03, 2006

Kirk Kerkorian Dumps GM: Wagoner Wins, Shareholders Lose

Friday's exit by Kirk Kerkorian from GM stock should really worry and frustrate shareholders. It isn't often that an investor of such pedigree becomes so disenchanted with management that he simply walks away from his investment.

I was particularly struck by a quote in one of the Wall Street Journal's articles. It had GM director Armando Codina asking,

"Who does this guy from Las Vegas think he is, telling us what to do?"

This is simply incredible. Perhaps a more important question is,

This is simply incredible. Perhaps a more important question is,

"Who does Armando Codina think he is, and what does he think he's accomplished as a GM director to create value for the shareholders he represents?"

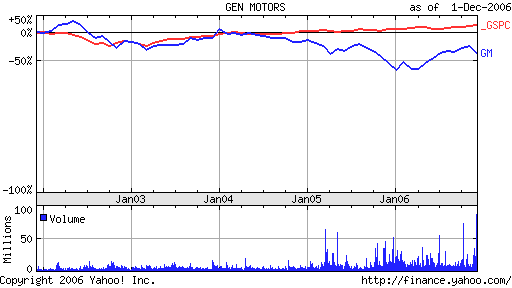

As the nearby Yahoo-sourced five-year price chart for GM and the S&P500 shows (click on the chart to view a larger version), GM was going nowhere for years before Kerkorian showed an interest in the firm. The only significant uptick the company's stock has shown was after the billionaire showed signs of sustained interest in contributing to GM's long-term "turnaround."

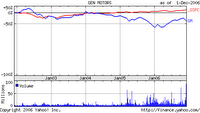

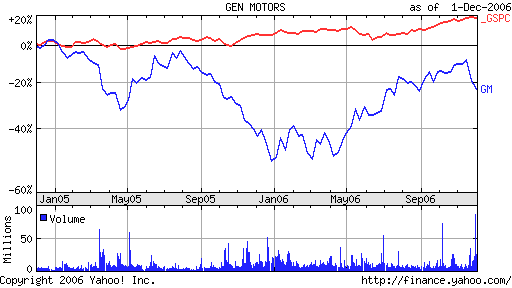

If I were a GM shareholder, I'd be bolting too, now. The stock was down significantly as Kerkorian pulled the last of his money out of the troubled auto maker. This six-month price chart shows how the stock lost twenty percentage points of gain in November, ending the month even with the index for its six-month performance.

If I were a GM shareholder, I'd be bolting too, now. The stock was down significantly as Kerkorian pulled the last of his money out of the troubled auto maker. This six-month price chart shows how the stock lost twenty percentage points of gain in November, ending the month even with the index for its six-month performance.

To answer Codina's question, though, Kerkorian, and his sometime-lieutenant, Jerry York, significantly contributed to the rescue of Chrysler by restructuring it and selling it to Daimler-Benz, profiting roughly $3B in the process. So, just on past performance, one would tend to bet on Kerkorian over Wagoner and his board.

Over the last two years, the company's stock price has behaved like a roller coaster. Rather than listen to York, who was given a seat on the GM board, and Kerkorian, Wagoner played a game of "chicken" with the savvy investor. Now, the shareholders have lost. An investor with a legendary touch for making money, and a genuine interest in the company, and its sector, is gone.

Over the last two years, the company's stock price has behaved like a roller coaster. Rather than listen to York, who was given a seat on the GM board, and Kerkorian, Wagoner played a game of "chicken" with the savvy investor. Now, the shareholders have lost. An investor with a legendary touch for making money, and a genuine interest in the company, and its sector, is gone.

To me, Kerkorian has behaved as a sort of modern-day J.P. Morgan. I mean that in the best sense, as a compliment. He has seen industry restructuring potential where the current CEOs have seen only discomforting change. By considering broad-scale integration of GM and Nissan/Renault, Kerkorian offered shareholders a chance to have a stake in an auto maker which would have had the management talent and market share size to survive, and maybe prosper, in a long-term slugging match with Toyota.

Now, all shareholders have is Wagoner's tired, conventional attempts to stave off disaster. Last week, ironically, the company completed the sale of its controlling interest in its financing arm, GMAC, thus selling the last of the family jewels. With this cash, and the loss of the continuing profit stream from the finance unit, GM has more than mortgaged its future- it simply sold it to for continued short-term survival.

According to various media pundits, Kerkorian may return when GM has suffered sufficient losses for the directors to come to their collective senses. But, given their rebuff of York's suggestions this past fall, one wonders if there will be enough time and money left, whenever that moment comes, for even Kerkorian & Co. to wring value out of what will be a then much-weakened GM.

For now, though, Rick Wagoner is in possession of the field, having seen off both Carlos Ghosn's and Kirk Kerkorian's attempts to help GM shareholders survive the next few years of difficulty.

I was particularly struck by a quote in one of the Wall Street Journal's articles. It had GM director Armando Codina asking,

"Who does this guy from Las Vegas think he is, telling us what to do?"

This is simply incredible. Perhaps a more important question is,

This is simply incredible. Perhaps a more important question is,"Who does Armando Codina think he is, and what does he think he's accomplished as a GM director to create value for the shareholders he represents?"

As the nearby Yahoo-sourced five-year price chart for GM and the S&P500 shows (click on the chart to view a larger version), GM was going nowhere for years before Kerkorian showed an interest in the firm. The only significant uptick the company's stock has shown was after the billionaire showed signs of sustained interest in contributing to GM's long-term "turnaround."

If I were a GM shareholder, I'd be bolting too, now. The stock was down significantly as Kerkorian pulled the last of his money out of the troubled auto maker. This six-month price chart shows how the stock lost twenty percentage points of gain in November, ending the month even with the index for its six-month performance.

If I were a GM shareholder, I'd be bolting too, now. The stock was down significantly as Kerkorian pulled the last of his money out of the troubled auto maker. This six-month price chart shows how the stock lost twenty percentage points of gain in November, ending the month even with the index for its six-month performance.To answer Codina's question, though, Kerkorian, and his sometime-lieutenant, Jerry York, significantly contributed to the rescue of Chrysler by restructuring it and selling it to Daimler-Benz, profiting roughly $3B in the process. So, just on past performance, one would tend to bet on Kerkorian over Wagoner and his board.

Over the last two years, the company's stock price has behaved like a roller coaster. Rather than listen to York, who was given a seat on the GM board, and Kerkorian, Wagoner played a game of "chicken" with the savvy investor. Now, the shareholders have lost. An investor with a legendary touch for making money, and a genuine interest in the company, and its sector, is gone.

Over the last two years, the company's stock price has behaved like a roller coaster. Rather than listen to York, who was given a seat on the GM board, and Kerkorian, Wagoner played a game of "chicken" with the savvy investor. Now, the shareholders have lost. An investor with a legendary touch for making money, and a genuine interest in the company, and its sector, is gone.To me, Kerkorian has behaved as a sort of modern-day J.P. Morgan. I mean that in the best sense, as a compliment. He has seen industry restructuring potential where the current CEOs have seen only discomforting change. By considering broad-scale integration of GM and Nissan/Renault, Kerkorian offered shareholders a chance to have a stake in an auto maker which would have had the management talent and market share size to survive, and maybe prosper, in a long-term slugging match with Toyota.

Now, all shareholders have is Wagoner's tired, conventional attempts to stave off disaster. Last week, ironically, the company completed the sale of its controlling interest in its financing arm, GMAC, thus selling the last of the family jewels. With this cash, and the loss of the continuing profit stream from the finance unit, GM has more than mortgaged its future- it simply sold it to for continued short-term survival.

According to various media pundits, Kerkorian may return when GM has suffered sufficient losses for the directors to come to their collective senses. But, given their rebuff of York's suggestions this past fall, one wonders if there will be enough time and money left, whenever that moment comes, for even Kerkorian & Co. to wring value out of what will be a then much-weakened GM.

For now, though, Rick Wagoner is in possession of the field, having seen off both Carlos Ghosn's and Kirk Kerkorian's attempts to help GM shareholders survive the next few years of difficulty.

Subscribe to:

Posts (Atom)