skip to main |

skip to sidebar

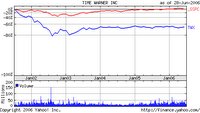

The Wall Street Journal ran another piece about TimeWarner's woes last Friday. I wrote about TWX recently here. The chart at the left displays the firm's performance, relative to the S&P500, over the last five years.Rather than repeat what I wrote there, which is pretty recent, I'd like to use the continuing coverage of TimeWarner's troubles to discuss a root cause of the trouble. That cause is a confusion among senior management of growth and size.Here's a quick primer. Growth prospects have and create value based upon their own performance. Adding or retaining growth prospects among a collection of non-growth units will hide the value created by the growth prospects. Being a large company is no longer value creating in and of itself, and certainly not in a fast-changing, technologically-affected sector like entertainment and communications.Thus, Time Warner is now being run exactly wrong. It's a testament to a bygone age in which size conferred safety from takeovers. Dick Parsons points to a few units and assures investors that, any day now, TWX will pull out of its value-destroying tailspin.The reality is this. In this day and age, small companies, like YouTube (to be covered in an imminent post) can create successfully, in a garage what large media companies cannot. Small startups can employ bright people, off-the-shelf technology and functional services (accounting, HR, sales, finance), get funding from VC's or other sources, and, ultimately, the market. In surprisingly short timeframes, they can commercialize and market products and services that a giant like Time Warner can only discuss and plan. If the latter could effectively implement the concept to begin with.Time Warner is ailing because its many mediocre divisions, staffed by mediocre salaried employees, can't innovate and grow sufficiently to match competitors. The size of this congolmerate makes delivering excellent customer value at a profit a second-order issue, behind just "running the company."According to the WSJ, TWX has lost 10% of it's market value since Icahn abandoned his attempt to get control of the board. Not surprising.In such a dynamic sector as entertainment, why would anyone expect a large, multi-divisional dinosaur to create consistently-superior shareholder returns? The very size of TWX almost guarantees that some of their units will drag performance. Shareholders would be so much better off by a split of the firm into many pieces, each delivering superior value to consumers on its own, and earning consistently superior returns for its shareholders. The weak, lagging units would, necessarily, be dealt with as the market typically does- value destroyed, bought cheaply for restructuring, and removed as a burden on the better-performing growth prospects that are now hidden within Time Warner's vast collection of media businesses.

The business media was abuzz on Monday and Tuesday of this week with news of Bill Gates' best buddy, Warren Buffett's, gift of $37B to the former's foundation.I caught part of the public relations event in which Bill, his wife, Melinda, and Warren Buffett announced the gift. Has anyone seen Bill Gates this happy and relaxed since his early days as a middling guest of Steve Jobs, when the latter was still doing battle with IBM in the mid-1980s?Last month, I saw Gates interviewed on Donny Deutsch's "The Big Idea." When Deutsch asked Gates what Bill would say to the leaders of Google, if they were in the audience, Bill nervously mumbled something like, ".....ah...we're going to keep you guys honest." I wrote about it in this prior post. I'm sure that struck fear into the hearts of Google's leaders......NOT.Then there was the WSJ story recently about Gates commissioning his former aide to develop a Microsoft VOIP telephony business. Let's see....Vonage is already out front, and SBC/ATT and Verizon are having their own troubles just treading water in the voice business. What is it Microsoft is going to bring to this market, besides some of that now-famous $35B cash hoard? Oh, wait, Google's positioned in that space, too, with instant messaging and email......oops!Corporate failures are replete with examples of companies whose only contribution to a new product/market was the cash they burned through, to their shareholders' dismay. Ask Carl Icahn about Blockbuster.What seems unfailingly clear to me, now, is that Bill Gates is doing his shareholders a tremendous disservice by hanging around Microsoft headquarters. I have been saying for months, in various posts, that his last five years at the helm of the company he founded have been disastrous. It's past time for him to go. When he looks so elated at the chance to give someone else's money away, and be rid of the job of creating shareholder value, it's time for him to do the right thing- right now. Not in two more years.I have to believe that Bill is eager to have a full-time job at which he cannot fail. Oh, sure, maybe the Google guys will somehow convince Warren Buffett to give them part of the $37B promised to Bill and Melinda's foundation, but that's a stretch.I think the sooner Bill totally and completely separates himself from Microsoft, and concentrates on giving away the billions in his foundation, the better it will be for Microsoft shareholders. A new Chairman might even sweep out some of that board deadwood and get a few competent business people in there to help oversee an overdue transformation, unlikely as it would be to succeed.Better late, than never.

Here's another sad story from the inept marketing deparment files.No less a corporate giant than Boeing is reported to be considering sale or closure of its Connexion internet venture. This is the business unit that provides the service to airlines which allows passengers to connect to the internet in flight.According to the Wall Street Journal, in last Thursday's edition, the business is probably on Boeing's books for $1B of asset value, but may only have a market value of $150MM.What surprised me is the marketing strategy that Boeing used for this service. At fees of $10-27/flight, on commercial carriers, it seems rather pricey for the expense budget set. Can you imagine a road warrior defending hundreds of dollars of connection fees per trip to his or her manager?Additionally, these days, you'd think the aforementioned warrior enjoys the relatively brief period of inaccessibility. Perhaps s/he can actually use the time to think and reflect about business, rather than respond pell mell to various assaults from the laptop, blackberry and cell phone.Apparently, Boeing belatedly decided to work with Rockwell Collins to outfit corporate (and, one assumes, time share) jets with this service. Wouldn't you think this would have been the first segment they went after? The folks who fly these planes are, by definition, seen as executives whose time is more valuable than the ones who fly commercial. One would think they could more easily, if it's even necessary, justify the Connexion fees for their trips. If it didn't "fly" with this group, it wouldn't succeed in the larger business travel community. But, if it did show promise in this more elite segment, the business would at least have bought some time to make further penetration into the business travel market.It's astonishing that such a relatively simple business could be mismarketed and mismanaged. Especially when owned and staffed by a capable, credible, large US company of Boeing's stature.It is understandable that not all ideas work out. But you'd think the more adventurous ones would be led and staffed by a more diligent and sensible group that knew basic market segmentation concepts, and how to implement them.

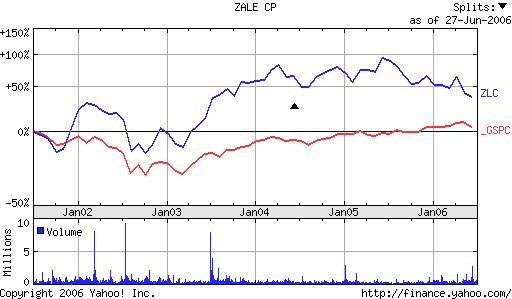

The Wall Street Journal featured two interesting articles last week which provide evidence of a continuing lack of skills in basic business management.One piece concerned Zale jeweler's self-inflicted wounds over the two years. The chart at right (click on it for a full size version), from Yahoo, depicts the company's performance, relative to the S&P, for the past 5 years. Sure enough, the stock price has slid recently. What's interesting is that it was merely mediocre prior to that. It hadn't really fallen steeply since 2003.According to the WSJ article, CEO Mary Forte assumed command and unilaterally took Zale from its low-end positioning as a purveyor of inexpensive diamonds, and frog-marched it upscale. Evidently on the basis of personal hunch and her affinity for upscale retail goods, Forte radically changed product mix and marketing plans. While the article paints a confused picture in which a board member, now interim CEO, alleges that Forte did not disclose the radical nature of her plans, a senior marketing officer claimed that she was refused a meeting with the board to explain the extent of the changes.I find it amazing that, in this day and age, a major, albeit low-end, retailer like Zale could experience such seat-of-the-pants strategy and marketing shifts, amidst poor communications. As I have written regarding Wal-Mart's attempts to move upmarket, this kind of change is always fraught with risk. It's rare in retailing that a major company has successfully moved upmarket without taking a very, very long time to reposition itself.A few days earlier, the WSJ ran a book review of a new tome from two BCG consultants. It is entitled, "Treasure Hunt," and provides the shocking news that consumers sometimes buy on price, and sometimes pay up for premium merchandise.Stop the presses! Revamp the Wharton and Kellogg marketing curricula!Really, are these guys serious? This has been a staple marketing truism since well before I went to undergraduate school in the late-1970s. That two consulting executives feel a need to illuminate the rest of us probably says more about their lack of knowledge of the past, and basic marketing, than about the novelty of their insights.Truthfully, if these two guys, Michael J. Silverstein and John Butman, are surprised by these findings, would you want to pay them to learn more about business on your company's tab? The WSJ review by Laura Landro, for whom I have a good deal of respect, suggests that its unspecified citing of "BCG client work" for data, and its use of fairly generic insights on consumer buying behavior, makes it just the latest of a long series of popular rewrites of basic marketing knowledge and theory going back well over thirty years.Once again, I wonder what it means that these authors thought they found something new, and someone thought this material of sufficient value to publish it. Probably that the average level of business acumen in US companies is far less than you really want to believe.

My partner and I were discussing the modern MBA full-time program the other day. Specifically, we were comparing notes on our situations as relatively inexperienced college graduates applying to Stanford and Wharton over 20 years ago, with a typical full-time, self-funded entrant to a top B-school now.His point, with which I agree, is that business schools such as Columbia, Chicago, Stanford, MIT, Tuck, Harvard and Wharton, in all probability, no longer attract the best students to their day programs. Instead, they now attract a mediocre talent pool. This is largely because of the schools' insistence on substantial work experience by candidates prior to attending their programs.Consider this. A bright young college graduate, after 4-5 years of experience, at a mid-large-sized company, is likely on a decent career path. These days, s/he could probably get the employer to pay for grad school. Otherwise, the potential B-school entrant has to forego two years' compensation, still pay for living expenses, plus the cost of grad school. Rough estimates for this are in the neighborhood, I believe, of $200K.So, one has to ask, why would someone incur all that added expense, when an employer will consider funding a candidate and continuing to keep them on payroll, or perhaps give them leave, in order to retain top talent? One answer is, the current experienced, full-time, self-funded MBA candidate is not the most talented segment of potential program entrants.My partner added, for good measure, the following hypothetical situation. If a young college grad is doing well at his or her job, some years out, would s/he really throw away all the progress, money, momentum, and contacts, for two years of self-funded school? A really good prospect can do better than taking him- or herself out of the workforce for two years on their own tab, only to have to start over career-wise.And, in these days of leaner staffs and heavier workloads, perhaps the non-applicants get better experience and skills by remaining in the workforce, sans graduate degree, and taking on more responsibility. Perhaps this results in better-performing employees. Only two years ago, I read an HBR piece touting the MFA as the advanced degree of the future.Frankly, even in my day, over two decades ago, quite a few of my fellow Penn grad students were far more interested in the added money they'd make upon graduation than in actually learning anything from their course work. Few had an active interest in learning a specific discipline, outside of career retreads wanting to enter the arcane world of M&A or financial instrument trading. I still read of 'best practices' in marketing which bear a striking similarity to those taught back when I was at Penn.Perhaps this explains why, despite the usual outpouring of full-time business school grads from name programs, companies, on average, don't seem to run better, or make fewer management gaffes. It could well be that name-graduate business program education is of decent quality, but the students are not.

My partner and I were, among the other topics I mentioned in my prior post, discussing how the media covers equity markets as if it is a living thing. Thus, the title, which my partner uttered comically to capture my description of CNBC's Bob Pisani's moronic commentary on equity market behavior last week during one of the down/flat days.Despite the signs of investors waffling on the economy's health, Brian Wesbury commented that average mortgage interest rates are still a full point lower than they were during the last expansion. And the Fed is moving to ensure low, long-term inflation. Thus, there's no reason to expect the economy to suddenly sieze up and slide into a recession.But, "the market, she be misguided" for now, I guess. The bulk of investors are too short-sighted, their memories too short, to see beyond a temporary period of seemingly mixed economic and market signals.Of course, if they were otherwise, the better performers probably would not be better, because they would not be pre-positioned for the subsequent equity market rise, when these mediocre investors figure out there is no need to be cautious, and move back into equities.I am reminded here of James O'Shaughnessy's admonition that even the best strategies can have periods of as long as two years of underperformance. Our own strategy strives for annual consistency, and has typically achieved it. Right now, with a market full of investors with no particular lasting directional disposition, our strategy is, as expected, underperforming. But it's only been so for a few months, and is unlikely to remain so for very long.Researching the S&P's historical performance this morning, I found that it had a near-zero trailing 12-month return for several consecutive months only once in the last 15 years- from March, 1994, to January, 1995. Even now, the trailing S&P is above 6%. Last year's first half was similar to this year's in that, by the end of June, the market was negative for the year-to-date. What all this seems to indicate is that the last 3-4 months of weak market returns are unlikely to remain weak for long. Chances are that the index will either plummet or soar sometime within the next few months. And a strategy's relative, or even absolute, performance during these few months of investor indecision could well become moot in another 6 months.".......the market, She be deliberating........."