As I mentioned in my previous post, Wal-Mart is overhauling its single-store format, in favor of six ethnic-income segmented styles of stores.

At the same time, the head of US store operations, Eduardo Castro-Wright, is relocating regional executives to their regions, from Bentonville. This, by itself, is not such a big deal, one would think.

However, read the comment in the WSJ article from Todd Libbra, responsible for 132 stores in Illinois,

"By reading the newspapers, watching the TV stations and being part of the community, I have a better flavor for what's going on."

In Chicago, perhaps. I happen to be from Illinois- downstate Illinois. He isn't getting a clue as to what is happening outside of the Cook County environs while he's nestled up there near the Windy City.

And, by the way, Todd, ever hear of newspapers online? A little thing you can get via something called the "internet?" I'm sure Todd could have been subscribing to numerous Illinois city and town newspapers via the internet, or his staff could have covered this base. Is this manager a good example of the caliber of executive at, and general awareness level of the world outside, Wal-Mart? exec and getting the tribune

Regarding the ethnic basis of segmentation, lots of companies cater to ethnic tastes, but none that I know of trumpet this as a segmentation lever. What are these guys thinking? Didn't they have even racial trouble last year and this already?

Perhaps the largely white senior executives in Bentonville, starting with CEO Lee Scott, think that by having a Mexican chief of US stores they will deflect further charges of racism. Instead, I wonder if they risk having a truly primitive segmentation strategy, imported from a less-sophisticated consumer society ,Mexico, derail their firm.

And what about the 'other' ethnic groups? Is this an opportunity for Target to welcome them with open arms?

My guess is that a really good segmentation strategy focused on differentiating store types would have resulted in something like three types of stores: rural, ex-urban middle class, and ex-urban on the fringes of upper class locales. Assortments of goods could easily be changed more granularly than merely with store type.

As it is, I wonder if Wal-Mart's historically in-bred management isn't totally fumbling its new segmentation and store-type strategy. They have been successful and well-regarded for doing one thing well throughout America and much of the world- leveraging tremendous purchasing power to offer large assortments of goods to mostly, though not exclusively, lower-income individuals, at very low prices. And, apparently, they have had some success attracting upper-income individuals to the stores to buy basic, low-priced goods for which the source of the product is unimportant.

I just don't see their new move into this complicated, multi-store approach taking full advantage of Wal-Mart's historic strength in low-cost sourcing of supply, while it seems to put them squarely opposite some more savvy retailing competitors in what is, for Wal-Mart, an entirely new product/market space.

Saturday, September 09, 2006

Friday, September 08, 2006

Wal-Mart's New Store-Segmentation Strategy

I think Wal-Mart's recently unveiled strategy of breaking with its standard store format, and moving to one of six types of stores, reflecting buyer types, will fail.

Based upon the information contained in the Wall Street Journal article yesterday, I don't see how Wal-Mart can maintain the value and/or meaning of its brand as it purposely fractures that brand's image in to six different pieces this year.

There are now several aspects to the Wal-Mart dilemma. To begin with, for the past five years, the company's stock price has underperformed the S&P500, which rose modestly, as shown in the chart on the left, with a stock price decline. For comparison, Target, a competitor, saw its stock price rise 50% during the same period.

There are now several aspects to the Wal-Mart dilemma. To begin with, for the past five years, the company's stock price has underperformed the S&P500, which rose modestly, as shown in the chart on the left, with a stock price decline. For comparison, Target, a competitor, saw its stock price rise 50% during the same period.

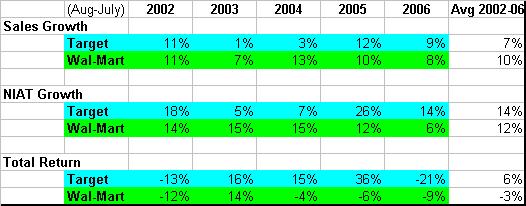

Looking more closely at the last two years, though, as the table on the left shows, Wal-Mart's Net Income After Tax growth underperformed Target's, meaning the former has suffered margin pressure or SG&A costs increases that it can't recover through its low prices.

Looking more closely at the last two years, though, as the table on the left shows, Wal-Mart's Net Income After Tax growth underperformed Target's, meaning the former has suffered margin pressure or SG&A costs increases that it can't recover through its low prices.

According to the Journal article, Target's same-store sales are now outpacing Wal-Mart's, 6% vs. 3%.

If you think back to mid-2005, the general business media sentiment was that Wal-Mart was in trouble for two reasons. On the one hand, high gasoline prices were thought to be crimping the discretionary purchasing power of the average Wal-Mart customer, who is generally typified as among the lower income groups. On the other hand, when the pundits admitted that there has been a consistently healthy, growing US economy for the past three years or so, they worried that Wal-Mart's customers were moving upmarket to.....Target.

And so it seems they were. In fact, it appears as if both assessments were true.

Around that time, in mid-late 2005, Lee Scott, the CEO of Wal-Mart, heralded the company's commitment to move upmarket, too. There was a presence established on New York City's upper 5th Avenue, in order to tap into America's upscale fashion pulse.

At the time, I wrote this post to go on record opining that it would not work. Nothing in the WSJ piece has changed my mind. If anything, it's made me even more convinced that Wal-Mart is about to commit a marketing disaster of Edsel proportions.

Here's why I think this.

First, the architect of the strategy is Eduardo Castro-Wright, the former chief of Wal-Mart stores in Mexico. He did something similar there, stratifying store types based solely on incomes. Sales rose.

Now, Mr. Castro Wright is attempting to apply consumer marketing from Mexico to the more complex US market. Interesting approach. The article states that Wal-Mart has hired various PhDs in ethnicity and food disciplines. And some types of 'research,' though precisely what type is not mentioned.

I don't think transferring a simple, one-dimensional segmentation scheme, based upon income, from the Mexican market to the much more diverse and sophisticated US market, will work. Adding the simplistic dimension of race.....er...ethnicity, won't do much better. The Journal piece lists the ethnic store variants as including those targeted at Black and Hispanic populations.

Most modern market segmentation work involves oceans of data, immense amounts of sophisticated multivariate analysis and modeling, usually done by a well-respected professor from a reputable Graduate School of Business somewhere in the US, and results in a few, less clear-cut segmentation dimensions. This is what factor analysis does- it loads many relevant segmentation bases onto a few operationally-addressable ones. But never have I seen a segmentation strategy expressed in dimensions so crude and tired as, solely, race and income.

Nevermind that Wal-Mart has enough problems with its images among certain ethnic groups already. And, am I the only person who finds it too ironic that Wal-Mart unveils a racially-oriented segmentation strategy only weeks after their now-departed ethnic ambassador, Andrew Young, embarrassed himself and the company with his on-air ethnic slurs against Koreans and Indians?

My second reason for believing Wal-Mart's new strategy will fail is that it undercuts the company's main competitive weapon, which is low cost supply. With product assortments being tailored by segment, volumes will necessarily fall, and costs, predictably, rise. The WSJ piece refers to a Bain & Co., study concluding just that. So Wal-Mart is departing from its historic strength, in quest of higher sales, while margins have already been under pressure lately.

My third reason for predicting the failure of the new store strategy is that it flies in the face of brand theory. The penultimate reason for the establishment of a brand franchise is to communicate one or two key values as identified with the brand. For Wal-Mart, it has been "every day low prices." Now, it's six different messages. Which means much of the historically-built brand value will be blurred and cease to exist. This would seem to fly in the face of most modern brand management theory.

Another related reason which I believe will lead to the multi-store concept's demise is basic consumer behavior regarding luxury and upscale goods, and "the wheel of retailing." I mentioned this latter concept in my previously linked post from last fall. The concept suggests that there is always a lowest-priced retailer, and others gradually try to move upmarket.

However, as I noted in that prior post, it's rarely, if every, been done successfully. In soft goods, both Sears and K-Mart failed with celebrity designers Cheryl Tiegs, Jaclyn Smith, and Martha Stewart. American consumers don't tend to buy luxury goods on price, or to frequent low-end stores for luxury items. Upscale consumers may, and do, head to Sam's Clubs and Costco for low prices on basic staples. But I doubt many real wine connoisseurs will be rushing to Wal-Mart for their $500 bottles of wine. Last I saw, the big move there is into online, out-of-state purchasing of wine at significant discounts.

I could go on in this vein. And I may in a later post. But for now, let me stop and suggest the following. This is one case in which I'd expect, and approve of, a company like Wal-Mart, with its in-bred, home-grown management, to hire outside market research consultants, social trend seers, and maybe even a team from Bain & Co., or McKinsey & Co., to provide some objective, experienced perspectives on the very important question of if, and how, to become a segment-oriented retailer.

Instead, I seriously believe that all Wal-Mart did was promote its most successful country manager to revamp US operations just like he did in Mexico. And being home-grown and in-bred, the senior executives in Bentonville see nothing wrong in rejiggering their marketing approaches without any outside help.

They seem to be clueless as to just how far they are departing from the formula that made them so successful. It may not be an engine of consistently superior total returns, but it is at least fulfilling its mission of dominating the low-priced retail niche.

Moving out of that niche, willy-nilly, with a crudely-designed, racially-oriented market segmentation strategy, to compete with much more nuanced marketers such as Les Wexner's Limited Brands lines, and others, seems to me like a recipe for disaster.

Nothing about this strategy makes sense to me. Not the segmentation, nor the cost implications, or the consumer behavior assumptions.

Time will tell if I am right.

Based upon the information contained in the Wall Street Journal article yesterday, I don't see how Wal-Mart can maintain the value and/or meaning of its brand as it purposely fractures that brand's image in to six different pieces this year.

There are now several aspects to the Wal-Mart dilemma. To begin with, for the past five years, the company's stock price has underperformed the S&P500, which rose modestly, as shown in the chart on the left, with a stock price decline. For comparison, Target, a competitor, saw its stock price rise 50% during the same period.

There are now several aspects to the Wal-Mart dilemma. To begin with, for the past five years, the company's stock price has underperformed the S&P500, which rose modestly, as shown in the chart on the left, with a stock price decline. For comparison, Target, a competitor, saw its stock price rise 50% during the same period. Looking more closely at the last two years, though, as the table on the left shows, Wal-Mart's Net Income After Tax growth underperformed Target's, meaning the former has suffered margin pressure or SG&A costs increases that it can't recover through its low prices.

Looking more closely at the last two years, though, as the table on the left shows, Wal-Mart's Net Income After Tax growth underperformed Target's, meaning the former has suffered margin pressure or SG&A costs increases that it can't recover through its low prices.According to the Journal article, Target's same-store sales are now outpacing Wal-Mart's, 6% vs. 3%.

If you think back to mid-2005, the general business media sentiment was that Wal-Mart was in trouble for two reasons. On the one hand, high gasoline prices were thought to be crimping the discretionary purchasing power of the average Wal-Mart customer, who is generally typified as among the lower income groups. On the other hand, when the pundits admitted that there has been a consistently healthy, growing US economy for the past three years or so, they worried that Wal-Mart's customers were moving upmarket to.....Target.

And so it seems they were. In fact, it appears as if both assessments were true.

Around that time, in mid-late 2005, Lee Scott, the CEO of Wal-Mart, heralded the company's commitment to move upmarket, too. There was a presence established on New York City's upper 5th Avenue, in order to tap into America's upscale fashion pulse.

At the time, I wrote this post to go on record opining that it would not work. Nothing in the WSJ piece has changed my mind. If anything, it's made me even more convinced that Wal-Mart is about to commit a marketing disaster of Edsel proportions.

Here's why I think this.

First, the architect of the strategy is Eduardo Castro-Wright, the former chief of Wal-Mart stores in Mexico. He did something similar there, stratifying store types based solely on incomes. Sales rose.

Now, Mr. Castro Wright is attempting to apply consumer marketing from Mexico to the more complex US market. Interesting approach. The article states that Wal-Mart has hired various PhDs in ethnicity and food disciplines. And some types of 'research,' though precisely what type is not mentioned.

I don't think transferring a simple, one-dimensional segmentation scheme, based upon income, from the Mexican market to the much more diverse and sophisticated US market, will work. Adding the simplistic dimension of race.....er...ethnicity, won't do much better. The Journal piece lists the ethnic store variants as including those targeted at Black and Hispanic populations.

Most modern market segmentation work involves oceans of data, immense amounts of sophisticated multivariate analysis and modeling, usually done by a well-respected professor from a reputable Graduate School of Business somewhere in the US, and results in a few, less clear-cut segmentation dimensions. This is what factor analysis does- it loads many relevant segmentation bases onto a few operationally-addressable ones. But never have I seen a segmentation strategy expressed in dimensions so crude and tired as, solely, race and income.

Nevermind that Wal-Mart has enough problems with its images among certain ethnic groups already. And, am I the only person who finds it too ironic that Wal-Mart unveils a racially-oriented segmentation strategy only weeks after their now-departed ethnic ambassador, Andrew Young, embarrassed himself and the company with his on-air ethnic slurs against Koreans and Indians?

My second reason for believing Wal-Mart's new strategy will fail is that it undercuts the company's main competitive weapon, which is low cost supply. With product assortments being tailored by segment, volumes will necessarily fall, and costs, predictably, rise. The WSJ piece refers to a Bain & Co., study concluding just that. So Wal-Mart is departing from its historic strength, in quest of higher sales, while margins have already been under pressure lately.

My third reason for predicting the failure of the new store strategy is that it flies in the face of brand theory. The penultimate reason for the establishment of a brand franchise is to communicate one or two key values as identified with the brand. For Wal-Mart, it has been "every day low prices." Now, it's six different messages. Which means much of the historically-built brand value will be blurred and cease to exist. This would seem to fly in the face of most modern brand management theory.

Another related reason which I believe will lead to the multi-store concept's demise is basic consumer behavior regarding luxury and upscale goods, and "the wheel of retailing." I mentioned this latter concept in my previously linked post from last fall. The concept suggests that there is always a lowest-priced retailer, and others gradually try to move upmarket.

However, as I noted in that prior post, it's rarely, if every, been done successfully. In soft goods, both Sears and K-Mart failed with celebrity designers Cheryl Tiegs, Jaclyn Smith, and Martha Stewart. American consumers don't tend to buy luxury goods on price, or to frequent low-end stores for luxury items. Upscale consumers may, and do, head to Sam's Clubs and Costco for low prices on basic staples. But I doubt many real wine connoisseurs will be rushing to Wal-Mart for their $500 bottles of wine. Last I saw, the big move there is into online, out-of-state purchasing of wine at significant discounts.

I could go on in this vein. And I may in a later post. But for now, let me stop and suggest the following. This is one case in which I'd expect, and approve of, a company like Wal-Mart, with its in-bred, home-grown management, to hire outside market research consultants, social trend seers, and maybe even a team from Bain & Co., or McKinsey & Co., to provide some objective, experienced perspectives on the very important question of if, and how, to become a segment-oriented retailer.

Instead, I seriously believe that all Wal-Mart did was promote its most successful country manager to revamp US operations just like he did in Mexico. And being home-grown and in-bred, the senior executives in Bentonville see nothing wrong in rejiggering their marketing approaches without any outside help.

They seem to be clueless as to just how far they are departing from the formula that made them so successful. It may not be an engine of consistently superior total returns, but it is at least fulfilling its mission of dominating the low-priced retail niche.

Moving out of that niche, willy-nilly, with a crudely-designed, racially-oriented market segmentation strategy, to compete with much more nuanced marketers such as Les Wexner's Limited Brands lines, and others, seems to me like a recipe for disaster.

Nothing about this strategy makes sense to me. Not the segmentation, nor the cost implications, or the consumer behavior assumptions.

Time will tell if I am right.

Thursday, September 07, 2006

More on Viacom: Freston and Redstone

So much has happened in the business world that a few items almost slip into the cracks. Between Ford's new CEO, Intel's restructuring, and Chevron's new oil find, not to mention HP's board leak fracas, I almost forgot about Viacom's CEO, Tom Freston being fired, or retired, depending on technicalities, by his boss, Sumner Redstone.

In terms of total return performance, it would appear that Freston was giving the lie to Redstone's reason for the recent breakup of CBS and Viacom. As the Yahoo-sourced chart on the left illustrates, Viacom has plunged straight downward since its reincarnation in late 2005. It now has a -20% return, relative to the S&P500's single-digit positive gain, for the period.

In terms of total return performance, it would appear that Freston was giving the lie to Redstone's reason for the recent breakup of CBS and Viacom. As the Yahoo-sourced chart on the left illustrates, Viacom has plunged straight downward since its reincarnation in late 2005. It now has a -20% return, relative to the S&P500's single-digit positive gain, for the period.

Of course, with only a year's worth of separate performance, it's hard to tell if Freston really was failing at his task, or if Redstone was simply following up on reactions to his Tom Cruise dismissal, clearing out anyone who objected to his unilateral move over Freston's head.

From the details of yesterday's Wall Street Journal article, it's not clear what to expect of Viacom going forward. The two cronies that Redstone has re-installed at Viacom, CEO Phillipe Dauman and COO-like Tom Dooley, have a track record of tripling Vicacom's stock price when they last worked with him at the firm. Put that way, it's not clear Freston ever really had a chance. So I wasn't surprised to read that he had been reluctant to take the Viacom CEO job in the first place last year.

Reading further, it sounds unconvincing that Dauman is going to simply "foster innovation within the company," and stress aggressiveness with its "multiplatform" strategy. Couldn't Freston have done that? Wasn't he doing that? My sense has been that Viacom is simply another network whose assets have recently been rendered less valuable by the simple, inexpensive outflanking maneuvers of MySpace and YouTube.

Welcome to the truly "innovative" world, Mr. Dauman. Unlike the more formalized, corporate nature of old media, the new online media world seems to move much more quickly and decisively.

In the final analysis, I'm wondering now whether 82 year-old Sumner Redstone is the new Jack Welch. The cult celebrity Chairman for the decade. He is suddenly all over the papers, and even on a very flattering cable channel semi-bio a few days ago, hosted/narrated by director Brian Grazer, who has worked with Viacom and for Redstone before.

But, like Welch, he's now worried about his legacy. And this past year has apparently, at least in Redstone's mind, seriously jeopardized his image as the media mogul with the Midas touch.

In terms of total return performance, it would appear that Freston was giving the lie to Redstone's reason for the recent breakup of CBS and Viacom. As the Yahoo-sourced chart on the left illustrates, Viacom has plunged straight downward since its reincarnation in late 2005. It now has a -20% return, relative to the S&P500's single-digit positive gain, for the period.

In terms of total return performance, it would appear that Freston was giving the lie to Redstone's reason for the recent breakup of CBS and Viacom. As the Yahoo-sourced chart on the left illustrates, Viacom has plunged straight downward since its reincarnation in late 2005. It now has a -20% return, relative to the S&P500's single-digit positive gain, for the period.Of course, with only a year's worth of separate performance, it's hard to tell if Freston really was failing at his task, or if Redstone was simply following up on reactions to his Tom Cruise dismissal, clearing out anyone who objected to his unilateral move over Freston's head.

From the details of yesterday's Wall Street Journal article, it's not clear what to expect of Viacom going forward. The two cronies that Redstone has re-installed at Viacom, CEO Phillipe Dauman and COO-like Tom Dooley, have a track record of tripling Vicacom's stock price when they last worked with him at the firm. Put that way, it's not clear Freston ever really had a chance. So I wasn't surprised to read that he had been reluctant to take the Viacom CEO job in the first place last year.

Reading further, it sounds unconvincing that Dauman is going to simply "foster innovation within the company," and stress aggressiveness with its "multiplatform" strategy. Couldn't Freston have done that? Wasn't he doing that? My sense has been that Viacom is simply another network whose assets have recently been rendered less valuable by the simple, inexpensive outflanking maneuvers of MySpace and YouTube.

Welcome to the truly "innovative" world, Mr. Dauman. Unlike the more formalized, corporate nature of old media, the new online media world seems to move much more quickly and decisively.

In the final analysis, I'm wondering now whether 82 year-old Sumner Redstone is the new Jack Welch. The cult celebrity Chairman for the decade. He is suddenly all over the papers, and even on a very flattering cable channel semi-bio a few days ago, hosted/narrated by director Brian Grazer, who has worked with Viacom and for Redstone before.

But, like Welch, he's now worried about his legacy. And this past year has apparently, at least in Redstone's mind, seriously jeopardized his image as the media mogul with the Midas touch.

Wednesday, September 06, 2006

Ford's New CEO: Pros and Cons

Yesterday, Ford announced that its Chairman and CEO, Bill Ford, is relinquishing his CEO title to Alan Mulally, late of Boeing.

It looks like my prediction of last October has now partially come true. I thought that one of the companies would be gone within 5 years. Instead, one of the CEOs among Detroit's auto producers is gone. Oddly, in this case, by his own hand. So, technically, while there is not "one less CEO in Detroit," one of the sitting CEOs is gone.

From what I've read about Mulally, he is quite likely a good choice for Ford. Whether even he can save the company is anybody's guess. However, as noted in my post in June on Boeing v. Airbus, here, Boeing's commercial aircraft division, with the 787 Dreamliner, executed fundamentals and out-designed Airbus. Mulally gets the credit for that.

It's easy to see why Ford wants Mulally. He successfully turned Boeing's commercial division around. Bill Ford badly needs to save his family's company, and he's not too proud to fire himself and hire the best senior exec he can find to do it. Mulally led a decidedly marketing-oriented resurgence at Boeing, and Ford is no doubt hoping there is enough time left for a similar magic act at the auto maker.

It's not too hard to see why Mulally will jump to Ford, either. He did the heavy lifting at Boeing, only to have McNerney flee 3M and replace Harry Stonecipher as CEO. Talk about ingratitude. Whether Mulally can succeed at Ford is almost immaterial. Like Lou Gerstner at IBM, or Art Ryan at Prudential, he'll get credit if he turns it around, but the company's bad shape will be blamed if he doesn't. And he'll doubtless still be handsomely rewarded. Most importantly, though, is that he is now a "CEO." And regardless of Ford's outcome, he's in the major leagues now.

It's a very interesting end to a musical chairs game that began with Jack Welch's retirement 5 years ago. As the linked post about McNerney, contained in the prior post about Boeing and Airbus, notes, McNerney hadn't really done anything to write home about while leading 3M. Now, at Boeing, the guy who rescued it prior to his arrival is gone.

So, Alan Mullaly gets to be CEO of something, if not a healthy company. Jim McNerney has to show he can stay in one place and actually create superior shareholder value. And Rick Wagoner can breathe a sigh of relief that he isn't the first automotive CEO to get canned this year. He was noticeably smug about the Mullaly news on an interview with CNBC today. Wagoner's probably just happy everyone's focusing on the other ailing Detroit-based auto company for a while.

In the final analysis, Mulally is probably as good a choice to lead Ford as anyone else, and better than most. Despite many pundits crying for a "car guy" at Ford now, Mulally has actually succeeded at producing a customer-focused new product, the Dreamliner, and then beating the hell out of his competitor, Airbus, with it. And he wants to lessen Ford's dependence on trucks and SUVs, returning to designing and building compelling cars.

I'm not at all sure Mullaly has the time and resources to pull it off, but I will enjoy seeing if he can. And I'll enjoy seeing how much more consolidation, CEO change, etc., continues to occur in the auto industry in the months ahead.

It looks like my prediction of last October has now partially come true. I thought that one of the companies would be gone within 5 years. Instead, one of the CEOs among Detroit's auto producers is gone. Oddly, in this case, by his own hand. So, technically, while there is not "one less CEO in Detroit," one of the sitting CEOs is gone.

From what I've read about Mulally, he is quite likely a good choice for Ford. Whether even he can save the company is anybody's guess. However, as noted in my post in June on Boeing v. Airbus, here, Boeing's commercial aircraft division, with the 787 Dreamliner, executed fundamentals and out-designed Airbus. Mulally gets the credit for that.

It's easy to see why Ford wants Mulally. He successfully turned Boeing's commercial division around. Bill Ford badly needs to save his family's company, and he's not too proud to fire himself and hire the best senior exec he can find to do it. Mulally led a decidedly marketing-oriented resurgence at Boeing, and Ford is no doubt hoping there is enough time left for a similar magic act at the auto maker.

It's not too hard to see why Mulally will jump to Ford, either. He did the heavy lifting at Boeing, only to have McNerney flee 3M and replace Harry Stonecipher as CEO. Talk about ingratitude. Whether Mulally can succeed at Ford is almost immaterial. Like Lou Gerstner at IBM, or Art Ryan at Prudential, he'll get credit if he turns it around, but the company's bad shape will be blamed if he doesn't. And he'll doubtless still be handsomely rewarded. Most importantly, though, is that he is now a "CEO." And regardless of Ford's outcome, he's in the major leagues now.

It's a very interesting end to a musical chairs game that began with Jack Welch's retirement 5 years ago. As the linked post about McNerney, contained in the prior post about Boeing and Airbus, notes, McNerney hadn't really done anything to write home about while leading 3M. Now, at Boeing, the guy who rescued it prior to his arrival is gone.

So, Alan Mullaly gets to be CEO of something, if not a healthy company. Jim McNerney has to show he can stay in one place and actually create superior shareholder value. And Rick Wagoner can breathe a sigh of relief that he isn't the first automotive CEO to get canned this year. He was noticeably smug about the Mullaly news on an interview with CNBC today. Wagoner's probably just happy everyone's focusing on the other ailing Detroit-based auto company for a while.

In the final analysis, Mulally is probably as good a choice to lead Ford as anyone else, and better than most. Despite many pundits crying for a "car guy" at Ford now, Mulally has actually succeeded at producing a customer-focused new product, the Dreamliner, and then beating the hell out of his competitor, Airbus, with it. And he wants to lessen Ford's dependence on trucks and SUVs, returning to designing and building compelling cars.

I'm not at all sure Mullaly has the time and resources to pull it off, but I will enjoy seeing if he can. And I'll enjoy seeing how much more consolidation, CEO change, etc., continues to occur in the auto industry in the months ahead.

Hollywood Struggles: Tom Cruise Is Just The Tip of The Iceberg

Last week's dismissal of Tom Cruise from Viacom's stable of stars by Sumner Redstone turned heads in Hollywood, by all accounts. Once again, we were treated to a display of the glaring differences between how the financial and entertainment communities view the classic Hollywood business style of spending anything to retain and satisfy the "talent."

Saturday's Wall Street Journal carried a timely piece discussing the entertainment industry's woes regarding DVD sales. It seems they are finally cresting, and no replacement vehicle is in sight. The article quoted numerous film execs as focusing on and cutting costs, as well as being more selective in their choice of properties to develop. The role of outside investment partnerships, including hedge funds, was even blamed for bringing too much capital into the sector, causing movies to be made which were best left as only screenplays.

What really shocked me, though, was the realization that Disney studios had, only just last fall, analyzed the contribution of their non-children-oriented films to the studio's profitability, and found them unsustainable.

Which brings me to the title of this post. With this backdrop, does Sumner Redstone really seem so off his rocker? The WSJ piece alleges that Viacom barely broke even on "Mission Impossible III," while Cruise earned a reputed $80 million.

Given Wall Street's harder-nosed approach to business than Hollywood's, is it really likely that a hedge fund is going to pick up funding for Tom Cruise's ventures at the same price that Viacom did? After the allure of Tom visiting a few trading floors, I think reality will sink in.

Remember Kevin Costner's fame some years ago? He began making his own movies, irrespective of the advice of others, critics, or even box office sales. Last time I saw him, he was co-starring with the venerable Robert Duval on a cable channel western movie special. So much for lasting fame and fortune in Hollywood.

Meanwhile, back to the film companies. The other interesting development is how companies as diverse as Apple and Wal-Mart are squaring off over the prices they will pay for online distribution of video content from the studios. Everyone can see the potentials among various distribution channels, and nobody wants to be left out. Wal-Mart, with its 40% of DVD sales, has enormous clout right now. And they appear to be using it.

As I have said before about the digitalization of media, whichever ways things develop, it looks like the consumer is going to make out very well, with great product available at competitively-tested, affordable prices.

Saturday's Wall Street Journal carried a timely piece discussing the entertainment industry's woes regarding DVD sales. It seems they are finally cresting, and no replacement vehicle is in sight. The article quoted numerous film execs as focusing on and cutting costs, as well as being more selective in their choice of properties to develop. The role of outside investment partnerships, including hedge funds, was even blamed for bringing too much capital into the sector, causing movies to be made which were best left as only screenplays.

What really shocked me, though, was the realization that Disney studios had, only just last fall, analyzed the contribution of their non-children-oriented films to the studio's profitability, and found them unsustainable.

Which brings me to the title of this post. With this backdrop, does Sumner Redstone really seem so off his rocker? The WSJ piece alleges that Viacom barely broke even on "Mission Impossible III," while Cruise earned a reputed $80 million.

Given Wall Street's harder-nosed approach to business than Hollywood's, is it really likely that a hedge fund is going to pick up funding for Tom Cruise's ventures at the same price that Viacom did? After the allure of Tom visiting a few trading floors, I think reality will sink in.

Remember Kevin Costner's fame some years ago? He began making his own movies, irrespective of the advice of others, critics, or even box office sales. Last time I saw him, he was co-starring with the venerable Robert Duval on a cable channel western movie special. So much for lasting fame and fortune in Hollywood.

Meanwhile, back to the film companies. The other interesting development is how companies as diverse as Apple and Wal-Mart are squaring off over the prices they will pay for online distribution of video content from the studios. Everyone can see the potentials among various distribution channels, and nobody wants to be left out. Wal-Mart, with its 40% of DVD sales, has enormous clout right now. And they appear to be using it.

As I have said before about the digitalization of media, whichever ways things develop, it looks like the consumer is going to make out very well, with great product available at competitively-tested, affordable prices.

Tuesday, September 05, 2006

Ron Gettelfinger's Flawed Logic On Pensions

Friday's Wall Street Journal contained an editorial by Ron Gettelfinger, current president of the UAW.

Gettelfinger's topic is, of course, the funding of labor union worker pensions in the modern world. He begins by describing the 1950 negotiations between GM and the UAW. In Gettelfinger's world, there are only two possible positions- those of GM's Charles Wilson and the UAW's Walter Reuther. The former wanted company-based benefits, while the latter, not surprisingly, favored "universal" benefits for all workers, meaning, one supposes, a sort of societally- or governmentally-funded approach.

Actually, it turns out that both were probably wrong.

However, back to Gettelfinger. He draws exclusively on one Malcolm Gladwell, a writer who authored a piece entitled "The Risk Pool," in the August 28th issue of the New Yorker. According to Gladwell, European social policy, in which there is universal, state-run pension management and liability, is preferred to the US private system. He further alleges that "....individual companies (are) responsible for the care of their retirees. It is this fact, as much as any other, that explains the current crisis."

Near the end of the article, Gettelfinger argues, based upon Gladwell and his sources, that US companies carry a 15% cost disadvantage because of the lack of a universal pension system. Then, in his logical climax, he opines that the only way American pensions can ever be "safe" is to have a publicly-funded universal program.

The trouble with Gettelfinger's position begins at the very beginning. He puts up private pension schemes as the only straw man alternative to a public pension system.

In one of my first posts on this blog, here, written on September 15, 2005, I argued that the real problem is that anyone ever took anyone else's IOUs, instead of cash on the barrel head in the then-present day.

Simply put, anytime any worker accepts promises of future contributions, in lieu of cash, whether accruing in a personal account or general fund, that worker is assuming counterparty funding risks that no banker would ever take for free. Or on anything like the totally unsecured terms involved in an employment agreement.

Gettelfinger is wrong. The best alternative for any worker is for him, or his union, to demand cash payments, whether as current compensation or contribution to his retirement account, from the funding entity. That way, the funder has to solvently provide the payment, and cannot promise future contributions or payments which it may never actually possess.

Both universal and private pension schemes suffer from the human tendency to promise more than one may be able to certainly deliver. And, in the case of pensions, there is no realistic alternative remedy for the funding entity's breach of contract.

No worker should have to bear the risk of funding promised retirement compensation. He might risk the investment performance of those funds, but that is not the liability of the funding organization. If employers, or the government, had to pay cash, rather than than promises, into retirement accounts, then the "risk pool" concept would evaporate.

Problem solved. Without complete universal, publicly-provided pensions.

Gettelfinger's topic is, of course, the funding of labor union worker pensions in the modern world. He begins by describing the 1950 negotiations between GM and the UAW. In Gettelfinger's world, there are only two possible positions- those of GM's Charles Wilson and the UAW's Walter Reuther. The former wanted company-based benefits, while the latter, not surprisingly, favored "universal" benefits for all workers, meaning, one supposes, a sort of societally- or governmentally-funded approach.

Actually, it turns out that both were probably wrong.

However, back to Gettelfinger. He draws exclusively on one Malcolm Gladwell, a writer who authored a piece entitled "The Risk Pool," in the August 28th issue of the New Yorker. According to Gladwell, European social policy, in which there is universal, state-run pension management and liability, is preferred to the US private system. He further alleges that "....individual companies (are) responsible for the care of their retirees. It is this fact, as much as any other, that explains the current crisis."

Near the end of the article, Gettelfinger argues, based upon Gladwell and his sources, that US companies carry a 15% cost disadvantage because of the lack of a universal pension system. Then, in his logical climax, he opines that the only way American pensions can ever be "safe" is to have a publicly-funded universal program.

The trouble with Gettelfinger's position begins at the very beginning. He puts up private pension schemes as the only straw man alternative to a public pension system.

In one of my first posts on this blog, here, written on September 15, 2005, I argued that the real problem is that anyone ever took anyone else's IOUs, instead of cash on the barrel head in the then-present day.

Simply put, anytime any worker accepts promises of future contributions, in lieu of cash, whether accruing in a personal account or general fund, that worker is assuming counterparty funding risks that no banker would ever take for free. Or on anything like the totally unsecured terms involved in an employment agreement.

Gettelfinger is wrong. The best alternative for any worker is for him, or his union, to demand cash payments, whether as current compensation or contribution to his retirement account, from the funding entity. That way, the funder has to solvently provide the payment, and cannot promise future contributions or payments which it may never actually possess.

Both universal and private pension schemes suffer from the human tendency to promise more than one may be able to certainly deliver. And, in the case of pensions, there is no realistic alternative remedy for the funding entity's breach of contract.

No worker should have to bear the risk of funding promised retirement compensation. He might risk the investment performance of those funds, but that is not the liability of the funding organization. If employers, or the government, had to pay cash, rather than than promises, into retirement accounts, then the "risk pool" concept would evaporate.

Problem solved. Without complete universal, publicly-provided pensions.

Monday, September 04, 2006

Laptop Shopping: Dell's Miscalculation

Saturday saw the East Coast of the US hit with the monsoon-like fallout from hurricane Ernesto. With outdoor activities out of the question, my daughters and I, as many other denizens of the area did, went shopping.

As it happens, I had promised them upgraded personal computer facilities this year. This decision necessitated a long-delayed commitment to a wireless network, so that gear was also on the shopping list. With fall "back to school" sales in full flower, we set off on a rainy, overcast afternoon to buy electronics gear.

At our first stop, Costco, my daughters found several laptops their liking. Upon discussing the array of models displayed with the helpful Costco assistant, I rapidly came to realize that there was a fairly uniform set of features and capabilities available within a $200 price range. Being the first store at which we looked, we held off a purchase decision for later.

The next stop was Staples. I went there for networking gear. As I made sure that the components I selected were appropriate for the intended network setup, my daughters busied themselves with trying out the various laptops on display among the shelves in the back of the store. There must have been at least 20 different models on offer. Soon, they called out to me that they found one which they would like me to buy.

Amazingly, they had chosen a very good machine at a great price. I say "amazingly," not because my daughters chose it, but because we were at Staples. This was about the last place I expected to purchase a computer.

However, they found an HP Pavilion notebook on sale, for about $900. It had the typical 1GB of RAM, 100GB HD, wireless capability, XP operating system, DVD burner/reader, that most machines in the price range possess. Plus an in-lid camera and various additional software titles.

As I wrote in my prior post, here, Dell has seriously miscalculated how consumers buy PCs nowadays. I am a good example. Never before have I purchased a PC in person, at a retail store. Four Gateways and one Dell were bought over the phone, after customization.

Now, however, the typical off-the-shelf notebooks contain nearly-identical features and components, at very similar prices. Thanks to the evolution of various manufacturers' distribution policies, many retailers carry a wide variety of brands: HP, Toshiba, Gateway, Lenovo, and Acer, to name just a few. With this sort of product choice at similar prices, it doesn't take a genius to realize that spending more for marginal customization, while waiting a week for the product, is hard to justify.

Really, about the only option left nowadays is your choice of how much RAM to buy. Otherwise, notebooks in the $1,000 price range are all very similar.

The conclusion which I draw from all of this is that Dell has seriously missed the boat in terms of its understanding of the consumer segment's buying behavior evolution. This notebook, on which I'm writing this post, is intended to provide my daughters with their own computing platform, as well as wireless internet access. As a second (or, in my case, more) computer purchase, sufficient information and product choices are available at retail to obviate the need to custom design a solution.

Dell did very well in the 1990s with their custom-design, fast delivery business model. Now, however, with Saturday's experience fresh in my mind, I see how and why they are outdated in their distribution methods.

One can't denigrate their prior success. But I don't really think they possess any unique competitive advantages anymore to drive further consistently superior total return performance in the years to come.

As it happens, I had promised them upgraded personal computer facilities this year. This decision necessitated a long-delayed commitment to a wireless network, so that gear was also on the shopping list. With fall "back to school" sales in full flower, we set off on a rainy, overcast afternoon to buy electronics gear.

At our first stop, Costco, my daughters found several laptops their liking. Upon discussing the array of models displayed with the helpful Costco assistant, I rapidly came to realize that there was a fairly uniform set of features and capabilities available within a $200 price range. Being the first store at which we looked, we held off a purchase decision for later.

The next stop was Staples. I went there for networking gear. As I made sure that the components I selected were appropriate for the intended network setup, my daughters busied themselves with trying out the various laptops on display among the shelves in the back of the store. There must have been at least 20 different models on offer. Soon, they called out to me that they found one which they would like me to buy.

Amazingly, they had chosen a very good machine at a great price. I say "amazingly," not because my daughters chose it, but because we were at Staples. This was about the last place I expected to purchase a computer.

However, they found an HP Pavilion notebook on sale, for about $900. It had the typical 1GB of RAM, 100GB HD, wireless capability, XP operating system, DVD burner/reader, that most machines in the price range possess. Plus an in-lid camera and various additional software titles.

As I wrote in my prior post, here, Dell has seriously miscalculated how consumers buy PCs nowadays. I am a good example. Never before have I purchased a PC in person, at a retail store. Four Gateways and one Dell were bought over the phone, after customization.

Now, however, the typical off-the-shelf notebooks contain nearly-identical features and components, at very similar prices. Thanks to the evolution of various manufacturers' distribution policies, many retailers carry a wide variety of brands: HP, Toshiba, Gateway, Lenovo, and Acer, to name just a few. With this sort of product choice at similar prices, it doesn't take a genius to realize that spending more for marginal customization, while waiting a week for the product, is hard to justify.

Really, about the only option left nowadays is your choice of how much RAM to buy. Otherwise, notebooks in the $1,000 price range are all very similar.

The conclusion which I draw from all of this is that Dell has seriously missed the boat in terms of its understanding of the consumer segment's buying behavior evolution. This notebook, on which I'm writing this post, is intended to provide my daughters with their own computing platform, as well as wireless internet access. As a second (or, in my case, more) computer purchase, sufficient information and product choices are available at retail to obviate the need to custom design a solution.

Dell did very well in the 1990s with their custom-design, fast delivery business model. Now, however, with Saturday's experience fresh in my mind, I see how and why they are outdated in their distribution methods.

One can't denigrate their prior success. But I don't really think they possess any unique competitive advantages anymore to drive further consistently superior total return performance in the years to come.

Subscribe to:

Posts (Atom)