Today marked the first time in ages that Jack Welch has made an appearance on CNBC.

The occasion was to discuss this article, recently published as the cover story in Fortune magazine. It contends that Jack Welch's "rules" are now out of fashion. That he was a star CEO for the 1990s, but is now passe.

This morning, Welch appeared on CNBC, in a polo shirt, with a lush pastoral scene as a background, from Nantucket. Clearly, Welch chose to rebut the article in the role of retired, wise ex-CEO, rather than suited defender of a track record.

There are several aspects to this topic. One is Fortune's article. The next is Welch's rebuttal. And, finally, there is Welch's actual performance, which is purportedly the basis on which his now controversial views were built.

Betsy Morris' piece is of a mixed nature, in my opinion. While some of her "new rules" are different than Welch's explicit pronouncements, they are not necessarily things with which he would have, or now does, disagree: organizational agility, focus on building niche markets, hiring passionate people, and looking outward from the company.

Morris' "old rules," attributed to Welch, smack of being straw men. I don't personally recall Welch saying any of them verbatim as presented, except for the time honored, still-relevant advice to be #1 or #2 by market share, rather than compete as a distant also-ran. So in this case, Morris probably overstepped herself.

In the main, though, I think her points are well taken. She restated and sharpened them on CNBC this morning, appearing about 20 minutes before Welch did. She essentially noted that Welch and his 'six sigma' preoccupation tended to focus on wringing efficiency from existing businesses. She opined that today, popularly-lauded companies such as Apple and Google rapidly design and release whole new categories of products and services, whereas GE tended to carefully crawl along, grinding out steady earnings increases, rather than torrid product change and revenue growth.

Now, to Welch's reply. He first dismissed the whole matter as directed 'against my wife, Suzy, and me, because we write a weekly column for BusinessWeek, Fortune's competitor.' Then he also dismissed remarks by United Technologies CEO George David, reputed to rebuke Welch, as taken "out of context."

After these qualifiers, Welch essentially lampooned Morris' list of "old rules," and claimed that, in fact, her "new rules" are, in reality, his. And were all along. Welch steadfastly disputed that 'his era' is over, or that his approaches, as CEO, would no longer work, 5 years after his retirement.

A few comments on the matter thus far. Nobody but Jack Welch mentioned his current wife ( #3?) in all of this. Suzy didn't run GE for more than a decade- Jack did. Frankly, I don't really believe anyone else cares what Suzy Welch does or does not think about management.

It's unlikely that Jack Welch would have been against Morris' "new rules," provided that they ground out earnings which fit Welch's GE management style. However, they clearly were not his major foci while leading GE.

My revered mentor, an ex-GE senior planning exec, and Chase SVP of Corporate Planning, used to say, "there are hundreds of business aphorisms, some contradictory. The question at hand is, which are relevant in this situation, for this business."

That's really the nub of the Welch tempest right now. Morris is trying to say, 'Welch never said 'nimble,' so he's against it, and now it's important.' Welch is saying, 'only an idiot would be against a nimble company- I was always for 'nimble.'

Frankly, neither is totally correct. But, on balance, I think Morris is right.

Frankly, neither is totally correct. But, on balance, I think Morris is right.

Despite Morris' citing companies which are, themselves, not consistently superior in growing and delivering total returns to shareholders, I believe she is right in applauding the focus on raw revenue growth and market creation which is shared by companies like Apple, Google, or Gilead.

As I have written before, in this blog, size, by itself, is of little value anymore. Witness GM and Ford. IBM and Microsoft. Intel.

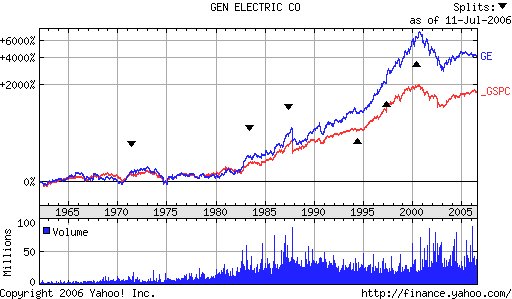

As the chart at the top of this post illustrates, even Welch didn't really manage GE to consistently outperform the S&P over his tenure, from 1981 to 2001. He had a few brief periods of radical outperformance, notably his restructuring of the firm upon his accession to the CEO post. For the most part, GE has never been a highly-consistent growth company which has outperformed the index (GE has never made my portfolio's list of consistently superior performing companies among the S&P500 candidates). I pointed this out to Welch, in person, in a meeting in the mid-1990s. He was shocked, and, literally, speechless for a few minutes, as he studied a chart I presented which showed GE's share price against the Dow-Jones since he took over GE. His comment, when he next spoke, was, "nobody's ever shown me this chart before." Suffice to say, the chart demonstrated that Jack had not added all that much comparative value for his shareholders over his tenure to that point.

As I wrote in a prior post, the most value Welch ever created for his shareholders, comparatively, with the market, was his brilliant triage of the sluggish firm he inherited from Reg Jones, amidst the worst inflationary environment of the modern US business era. The Jones era, for GE, was, as the chart above shows, dismal. Welch revitalized a tired company which had lost its focus and direction. However, owning GE didn't reliably provide equity investors with consistently superior growth and return prospects, as holding many other S&P components would have, over the past 20 years.

Among all of Welch's portfolio of businesses, GE Capital was the only really reliably high-growth unit. Upon taking over GE, Immelt was assailed by critics who suddenly had the scales fall from their eyes, and realized how heavily leveraged the unit was. Somehow, Welch managed to sprinkle magic dust over this easily-observed fact, during his tenure as CEO. Immelt suffered for the clever diversion of analysts' attention to predictable quarterly earnings sans consistently superior topline revenue growth for the firm.

So, for me, this whole episode, while entertaining (hey, it's on CNBC- what'd you expect?), is moot. Welch's GE was never one of those rare, consistently superior growth and return companies which are the hallmark, and components, of my investment portfolios. Arguing over "his rules," is, in my opinion, totally beside the point. If he'd run a more impressively-performing company, I'd feel differently.

But Welch didn't, so I don't.

No comments:

Post a Comment