In the many years that I have run monthly selections for my equity portfolio strategy, I don't believe McGraw's company, McGraw-Hill, has ever been among those chosen. McGraw is apparently the current chairman of the Business Roundtable.

On the same program, a reporter from the Financial Times was interviewed regarding her interview with Jeff Immelt, CEO of GE. This caused someone on the set to refer to Immelt as the "dean of American business."

Now, about this time, I got to wondering, which of the two CEOs has performed better over the past five years? I know Immelt's record- he's essentially wasted his shareholder's money by underperforming the S&P during his "deanship" at the helm of GE.

But, being the data-driven guy that I am, I took a fresh look at the current five-year numbers on sales and NIAT growth, as well as total return, for GE and McGraw-Hill.

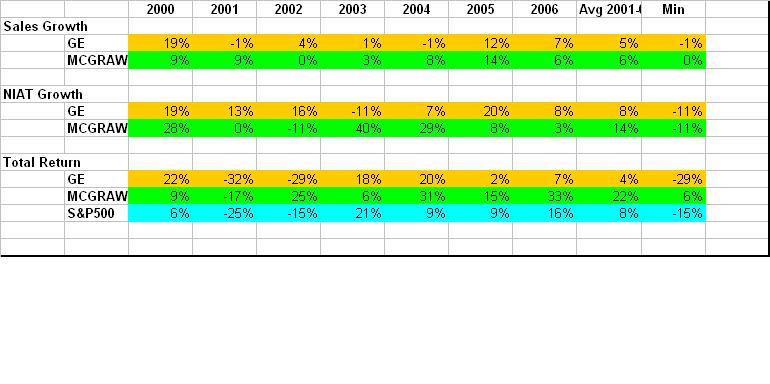

The chart on the left (click on it to view the enlarged version) contains the annual growth rates for the three measures.

The chart on the left (click on it to view the enlarged version) contains the annual growth rates for the three measures.It's not even close- Terry McGraw has clearly outmanaged Jeff Immelt, in terms of performance on these three key variables- for the past five years.

First, it's clear that both companies are among the low-growth type of large-caps. They have nearly identical average sales growth rates of 5% (GE) and 6% (MHP). However, McGraw-Hill, at 14%, has nearly double the average growth rate of GE's 8% for Net Income After Tax. As a result, McGraw-Hill's average annual total return for the last five years is 22%, to GE's 4%, and the S&P's 8%.

As my proprietary research has discovered, for slow-growth companies, profit growth and ROE are important determinants of total return performance. Investors clearly view the companies similarly as low-growth enterprises, and, thus, value McGraw-Hill's superior ability to consistently wring profits out of sluggishly-growing businesses. GE has simply not kept pace.

I think FT missed the boat by focusing on Immelt. For such a diversified and tough collection of businesses, Terry McGraw would have had something more to convey to FT's readership. All Immelt can really discuss is how to get overpaid and underperform while running a mediocre closed-end mutual fund. For more detail on this, simply search this blog for "immelt" and you'll find a collection of my prior pieces on Immelt's dismal performance as CEO of GE.

I'm glad I happened to be watching CNBC that morning, because I have a new respect for McGraw-Hill and its CEO. I'm still doubtful that the company will be selected for even my low-growth portfolio component, because its sales growth, while far slower than that of the average high-growth large-cap company, is still sufficiently high to be exceeding the S&P's average rate periodically.

Despite that, Terry McGraw appears to be producing a low-probability event, in that he has outperformed the S&P consistently over the past five years. There's no denying the data- he's clearly done a better job for his shareholders than Jeff Immelt has for his.

No comments:

Post a Comment