What initially struck me from the Journal piece is how Toyota CEO Katsuaki Watanbe's incredible insecurity fuels his company's continued excellent performance.

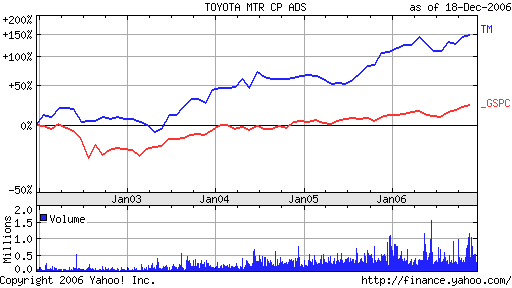

What initially struck me from the Journal piece is how Toyota CEO Katsuaki Watanbe's incredible insecurity fuels his company's continued excellent performance.As the nearby, Yahoo-sourced chart of Toyota's stock price, versus the S&P500 Index, indicates, the company has performed consistently better than the latter for most of the past five years. It's cumulative total return far surpasses that of the index over the entire period. Toyota isn't among the companies in the S&P500, so I don't own it. How I wish I could, and did.

As my proprietary research warns, however, cost-cutting is a relatively limited weapon in the quest for long-term, consistently superior total returns. Toyota's are already nearing an end as a competitive weapon. The rate of cost reductions is slowing, and product design flaws have recently spurred recalls of more vehicles than it sold last year.

I was very impressed with the attention to detail by the CEO. The Journal article discusses his observant manner as he walks the floor of his plants. His questioning of the traditional, long paint shop river, is what recently has led to Toyota's secret new process, which takes far less space and resources. Watanabe is ceaselessly exploring new ways to drive costs down and extend Toyota's lead in this area. To this end, he has commissioned a total re-evaluation of the production of the company's vehicles, with an audacious objective of cutting the number of parts required by 50%.

While, on one hand, Toyota is bumping up against some cost-cutting limits of current production methods, Watanabe is wisely opening up the company's managers to exploring entirely new ways of designing and producing their vehicles, thus, effectively, in microeconomics terms, putting the firm's operations on a new, longer-term, declining cost curve. They have redesigned their machines to be smaller, and their plants as well.

What amazes me about Toyota is that, while GM is catching up to them in some production efficiency measures in some plants, Toyota is already moving to tackle new production challenges that I cannot even imagine GM being ready to address. The production plant challenge is one, as is the paint line. Thus, Toyota is working on changing the very methods by which they will more efficiently pump out vehicles, while GM, and, presumably, Ford, are still working on making existing methods merely more efficient. It's clear that the two American auto giants are not even remotely in the same class as Toyota when it comes to conceiving and implementing continuous methods of improving operating efficiencies, and, thus, value-added.

Will Toyota succeed in these operational changes? Their diminishing lead in current efficiencies demonstrates how cost leadership can shrink, and, thus, lead to a loss of sustained superior performance. However, they are attempting new initiatives to retain this consistently superior total return performance. Either way, they are at risk.

And this, I believe, is one of the most enlightening elements of the Journal's Toyota story. Even a detail- and big-picture-obsessed, experienced and successful CEO, like Watanable, with a willing workforce, and strong competitive position, cannot count on continued superior total return performance. He's betting the company's continued performance every year, with each new initiative.

Sooner or later, Toyota will run into more difficulties in one of its programs for new production methods, or design flaws, that will derail its superb performance of the past few years. The truth is, with each additional year of excellent performance, their odds of another one diminish. It's simply how performance patterns are among large numbers of large corporations.

However, I will take great interest in seeing for how long this impressive auto producer can maintain its record of consistently outperforming the S&P500's total return.

No comments:

Post a Comment