Ford and GM's recent developments were the subject of a short piece in this week's Wall Street Journal. The author of the piece only went back to January of this year to issue his opinion. His verdict was that GM is in better shape for a "turnaround" because of outside pressure from Kerkorian, while Ford's two-class stock structure kept its value from rising due to the founding family's insulation from common investors. His conclusion is that Ford is less market-sensitive, due to the Ford family's near-controlling 40% voting stake in the firm.

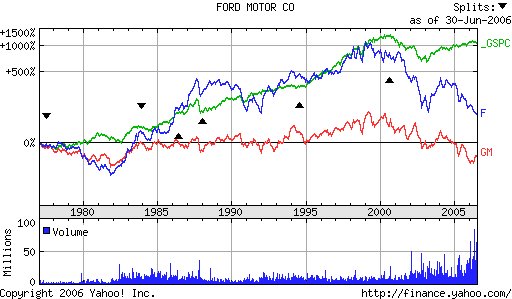

I find this a touch myopic, as the longterm Yahoo chart above shows. Comparing the S&P500, GM and Ford since 1979, it puts the lie to the notion that Ford has typically been slow to respond to market forces, due to the Ford family's control of the firm. Sure, in 2006, GM has displayed a better shareholder return than that of Ford. No question about that. Just not being in Chapter 11 yet is probably a big boost for GM.

However, if you look carefully at the chart above, it continues to echo what I discussed in a recent post about these two firms. While Ford's voting structure may shield it somewhat from market forces, it still has outperformed GM over the past quarter century. And by a rather handsome margin, as GM has been negative, while Ford looks to have returned something in the neighborhood (interpolating on the chart above) of 100%. The S&P returned roughly 1000% over the period.

That Ford had some significant "up" periods, from the early 1980s to 2000, suggests that they were, in fact, quite sensitive to shareholder returns. GM, by contrast, rarely broke out of a flat return curve, save for a few years in the late 1990s.

My point is that, due to an unnecessarily short analytical time horizon, the WSJ has summarily judged Ford to be too insular to save now. While GM, through the mixed blessing of attracting Kirk Kerkorian, and his lieutenant, Jerry York's advice to find a global partner, has temporarily surged ahead of the former in total return terms.

I don't necessarily believe Bill Ford is turning, or will turn around Ford. His "way forward" seems "way too optimistic," in my opinion. If only because the management team that got you to where Ford is now, is unlikely to take you somewhere else, as a shareholder. But the company is sensitive to market pressures all on its own.

I don't think GM is more "investor sensitive." Instead, it has to deal with a veteran value shopper, in Kerkorian. As the WSJ, as well as CNBC, articulated, what's good for GM shareholders, the prospect of a partial rescue in the form of some global tie-up with the likes of Nissan, is probably not good for CEO Wagoner. If anything, Wagoner put GM where it is today through his learned insensitivity to market forces, as a result of a long tenure at the stumbling auto giant.

Yes, GM may well have marginally brighter prospects for its shareholders. But don't attribute GM's idiosyncratic fortune to Ford's share voting structure. Ford is in trouble due to inept management that has tried to grapple with global pressures on an aged, badly-led competitor. Not due to an unwillingness to acknowledge the problem.

No comments:

Post a Comment