In discussing this with my business partner, I mused about whether P&G may be, for the first time, heading toward inclusion in our equity portfolio of consistently superior companies. After all, with a clear-headed, viable focus on consumers, and customer needs, one might think that the firm is within reach of becoming a really well-led, well-managed creator of shareholder returns, based upon solid business concepts and executions leading to consistently superior revenue growth.

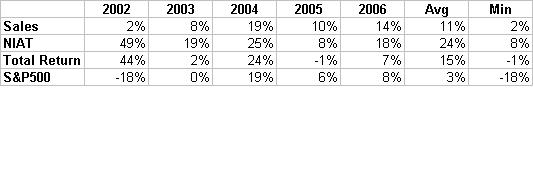

To get a better understanding of this, I did some analysis of the company's recent sales, NIAT, and total returns. They are presented in the table at left, on which you may click to enlarge.

To get a better understanding of this, I did some analysis of the company's recent sales, NIAT, and total returns. They are presented in the table at left, on which you may click to enlarge.The first thing I notice is that P&G's sales accelerated in 2004 and this year. A friend who works at the firm, locally, confirmed that these are the effects of the last two major acquisitions. The latter one being Gillette, last year.

This has an interesting effect on P&G, called "riding the tiger." Notice that its sales growth rates, pre-acquisitions, were in the single digits, on the low side, on average. In the years prior to 2002, they were also rather meager. Thus, P&G has bought growth, twice. The year in between the acquisitions displays a 10% sales growth- higher than the earlier years, but still not so high as with the immediate folding-in of the purchased sales bases.

My proprietary research shows that the market tends to favor companies which can consistently generate superior revenue growth. P&G has begun to buy its growth. Either of two things need to occur, if the company is to have a good chance of becoming a consistently superior total return-generating company.

Either it needs to generate organic growth to match that of the effects of the acquisitions, or it needs to be able to continue its acquisition program, making it a sort of 'standard operating procedure," for which investors are prepared to pay. The company is hitting some pretty high revenue growth targets for a consumer goods conglomerate. While the 10% revenue growth in 2005 was good, and better than the long-term S&P average, it was by no means near the upper end of the distribution of revenue growth in the S&P500.

NIAT growth at P&G has also been getting better, but the best years were in the earlier years of this period.

Taken together, the revenue and NIAT growth pictures lead to the total return performance shown in the table. P&G has a much better average than the S&P for the last five years. However, the last two years have been a close call. Most of the 12 point spread in average total return between the S&P and P&G is accounted for by 2002. I would guess that would have been from a "flight to quality" by investors, as the tech-bubble-bursting recession drove investors to safer havens. Too, the low returns in 2004 and 2006 could be the result of investor verdicts on the prices of each of the two major acquisitions in the the prior two years.

I like P&G's customer focus. I understand the broadening of their product and business portfolios recently. However, from the data above, I seriously wonder if they can sustain raw revenue growth in the next few years. This is where consistency of revenue growth at fairly high rates really challenges a company. If too much of the firm's recent success on this dimension was simply purchasing growth, then I think total returns will ebb, along with organic growth.

It will be very interesting to watch P&G in the next few years to see how their fundamental operating capabilities prove out, and whether the market rewards the firm, if they do.

No comments:

Post a Comment