On September 11th, The Wall Street Journal ran a celebratory piece on Jeff Immelt's five-year anniversary as GE's CEO.

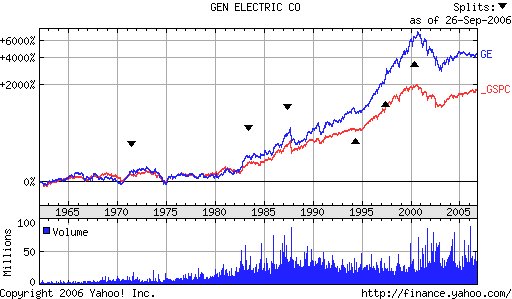

The Yahoo-sourced chart on the left depicts how Immelt's reign compares with those of prior CEOs of the company (Phillippe, Borch, Jones, Welch) going back to the early 1960s.

It's fair to say that long timeline charts such as this one can downplay earlier rough spots, since the end periods tend to have magnified appearances. For instance, the late-80s drop in stock price, coinciding with the 'crash' of 1987, is significant for its time, but pales in comparison to the absolute drop of the last few years.

That being the case, here's a five-year view of the same information, corresponding to Immelt's tenure as CEO.

That being the case, here's a five-year view of the same information, corresponding to Immelt's tenure as CEO.It seems to me that the WSJ is giving Immelt, and GE, the kid glove treatment. Maybe it's because of the fear of loss of GE's advertising revenues, and access to future stories.

However, looking at this Yahoo chart, it's difficult to understand how an industrial conglomerate can have underperformed the S&P500 through these particular last five years, and not be seen as needing to be led by someone else, or simply broken up.

Ask yourself this question:

If GE did not exist today, would someone create it as it currently exists?

I think the answer would almost certainly be, "no." What possible value would investors see in a TV network and movie studio buying: a jet engine business, a locomotive business, a financial services business, and power generation systems businesses, to name a few. There's absolutely no business synergies whatsoever that are unique to these businesses.

As I wrote here early last month, there is no longer any apparent value to the constituent business units of GE being assembled as GE.

Rather than observe the data I did in my earlier piece, the Journal contained quotes like this one, from Immelt's lieutenant, Bob Wright, vice chairman and head of GE's entertainment sector,

"He's in a good dynamic for a guy who has a lot of weight on his shoulders."

Does anybody reading this understand that sentence? Maybe Wright meant this,

"He's making a heckuva lot of money for a guy who has a lot of weight on his shoulders from not delivering for his shareholders."

Toward the end of the article, we perhaps get a clue as to why Immelt's GE is foundering so badly. The Journal relates that Immelt "urges employees to make bigger bets without fearing for their jobs if they fail." "Make it personal," the piece quotes GE's CEO as saying.

So now we have the 'kinder, gentler,' GE in evidence. Maybe Immelt figures, if he is kind to his employees, and forgives lack of performance, or consistently poor investment judgment, his board will do the same for him. Seems to be working, right?

In the end, all of Immelt's changes are not affecting the company's total returns. He can globalize the behemoth, ask his managers to take more risks, and even shuffle businesses in and out of the GE portfolio.

But in the end, over five years, Immelt simply has failed to lead GE to consistently superior performance, while raking in a royal compensation, as I noted here, back in March. In that post, I observed that Immelt has already received at least $21MM in cash compensation for failing to create consistently superior total returns for his shareholders. There's no way he needs to take the risks evidently necessary to make GE's long-term performance superior to the S&P's.

Furthermore, why give up this multi-million dollar gravy train and break the company up?

In this era of concern over "corporate governance," I'm frankly disappointed that the Wall Street Journal gave Immelt such an easy pass while reviewing his first five years at the helm of GE.

A year ago, I wrote, prior to almost any well-known pundit or industry analyst, that Ford and GM were in major trouble. Especially Ford. Back then, I opined that maybe the old media and investment banking giants weren't being candid, because the slowly-dying auto giants still paid a lot of bills for companies in those sectors.

I wonder if the same thing is occurring now, with GE. The truth would be very, perhaps too, costly to the media and financial service sectors, wouldn't it?

No comments:

Post a Comment