The Money and Investing section of the Wall Street Journal even carried an article yesterday with a chart box headline reading, "There's a new No. 1." CNBC had a special segment featuring Jim Cramer opining on which bank to buy. The network covered the mock "choice" with great fanfare.

To me, this is a silly contest of size between two financial utilities with more similarities than differences. Size of this sort can, and was, purchased. Especially by BofA, which is, in truth, NCNB (which became NationsBank) of Charlotte, which bought the right to rebrand itself with the storied name and logo of the San Francisco takeover victim.

First, let me go on record as stating that the only measure that matters is a longish-term total return for shareholders. As a quick approximation of this, here's a Yahoo-sourced price chart (please click on the chart to see a larger version) of BofA, Citi and the S&P500 for nearly 20 years.

First, let me go on record as stating that the only measure that matters is a longish-term total return for shareholders. As a quick approximation of this, here's a Yahoo-sourced price chart (please click on the chart to see a larger version) of BofA, Citi and the S&P500 for nearly 20 years.I thought it would be interesting to look at how similar the change in stock prices have been throughout the long period. Since 2000, there hasn't been all that much difference in the slopes of the curves for the two banks. It's clear that whatever outperformance Citi has enjoyed came in the 1998-2000 timeframe.

For clarity, though, here's the same chart, for just the last five years. BofA is clearly superior at having generated superior total returns. It confirms, in greater detail, that Citi's best performance period was more than five years ago.

For clarity, though, here's the same chart, for just the last five years. BofA is clearly superior at having generated superior total returns. It confirms, in greater detail, that Citi's best performance period was more than five years ago.All this is somewhat interesting, but perhaps misses the point. In five years, the better performing bank of the two only returned roughly 15%, total. Plus dividends. CitiGroup is a little better than flat, and worse than the S&P.

With a performance like this, maybe something should change at Citi.

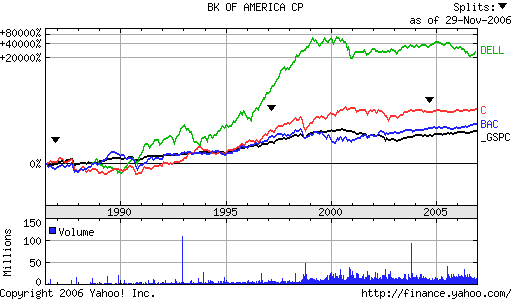

To put this in perspective, let's look at how a fallen growth stock stacks up against these two "large" banks.

To put this in perspective, let's look at how a fallen growth stock stacks up against these two "large" banks.In this chart, I've added Dell to the earlier long-term comparison of Citi, BofA, and the S&P500.

It sort of puts things in perspective for me. All this hue and cry over which bank is larger seems, for me, to rapidly fade into the background, as I see the much larger gain in stock price in Dell over the period. The two banks are literally not even in the same league. Not even after Dell plateaued six years ago.

As an investor, I can't say I even care which bank has which market cap. Both have such anemic returns over the last half decade that I doubt my strategy's selection process would include either company in my equity portfolio.

Yet another case of entertainment trumping news. The 'news' being, no matter which firm is larger, or how large they get, they still can't deliver consistently superior total returns for their shareholders. If one of them could? Now that would be news to me.

{kind=link}

No comments:

Post a Comment