We keep hearing that GM is successfully turning itself around. That Alan Mulally, Ford's new CEO, is planning a turnaround for that ailing auto maker.

What constitutes a "turnaround?" How is it measured? Does it have to take place within some timeframe to qualify as a turnaround, as distinct from, say, an evolution? Or basic business management?

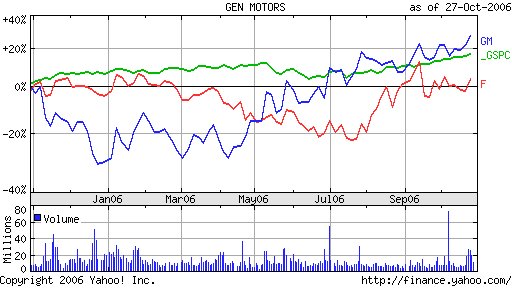

For example, look at the nearby Yahoo price chart (click on the chart to view an enlarged version) for Ford, GM, and the S&P500 for the past 12 months. To the casual eye, GM indeed appears to be "turning around," especially relative to the S&P and Ford.

However, as this second chart, depicting GM's stock price for the past five years, shows, it would not be the only time in the past 60 months that the company's stock price has rallied. However, each prior time, it subsequently fell. Given that this period contains the technology bubble burst, one might argue that that was the reason for the first selloff. In a sense, this makes my point. How many contextual factors must be considered, in order to judge a brief stock price move as a "turnaround?" Is Rick Wagoner correct in celebrating the twin victories of rebuffing Carlos Ghosn and reviving GM already? Or is GM's stock price, and total return, destined to head downward again within a few months, making investors have to time their buying and selling of GM quite finely in order to capture the temporary value gain in the stock?

However, as this second chart, depicting GM's stock price for the past five years, shows, it would not be the only time in the past 60 months that the company's stock price has rallied. However, each prior time, it subsequently fell. Given that this period contains the technology bubble burst, one might argue that that was the reason for the first selloff. In a sense, this makes my point. How many contextual factors must be considered, in order to judge a brief stock price move as a "turnaround?" Is Rick Wagoner correct in celebrating the twin victories of rebuffing Carlos Ghosn and reviving GM already? Or is GM's stock price, and total return, destined to head downward again within a few months, making investors have to time their buying and selling of GM quite finely in order to capture the temporary value gain in the stock?Is a turnaround measured in sales growth, or change in the rate of sales growth? Profit growth? Total return? All of these? Over what timeframes?

I'm curious, because when a firm like GM is claiming to already succeeding at its "turnaround," and then I hear and read analysis that casts doubt on their actual sales to end users, it gives me pause. It makes me think the entire concept has become a self-serving one.

And what about Alan Mulally's Ford Motor Company? It has a similar pattern to that of GM's stock price over the past five years, as the nearby chart illustrates. Twice in the past five years, its price has risen, only to slump, either quickly, or gradually over two and a half years.

And what about Alan Mulally's Ford Motor Company? It has a similar pattern to that of GM's stock price over the past five years, as the nearby chart illustrates. Twice in the past five years, its price has risen, only to slump, either quickly, or gradually over two and a half years.My own preference is to call a "turnaround" when a company's sales growth has placed it among the top large-cap or S&P companies on that measure, consistently, for several years. I feel the same about total returns. A few months, or even a year, of temporary sales growth and stock price rise does not, to me, sufficiently exceed normal S&P500 standard deviations from average performance to constitute anything more than random behavior.

For me, there's way too much going on in the auto sector to allow either Ford or GM to qualify for my portfolios any time soon. A genuine resurgence in sales, with accompanying profits that meet investors' expectations, over enough time to demonstrate lasting changes, not just one year's new models or one-off cost savings, will be required.

My portfolio strategy invests in companies which exhibit the hallmarks of consistently superior sales growth and total returns, not short-term gains, or long-term business uncertainty and inconsistencies in performance.

No comments:

Post a Comment