The WSJ piece suggests that Citi CEO Chuck Prince dismantle Citigroup. It's a good idea, and not just for Citi. Who knows, maybe it will catch on. I wrote about the similarities of the three large US commercial banks here in April, and about Citi here, in July, and about banking as a commodity here, more recently. Unfortunately, Blogger is not cooperating with my attempt to paste the one-year stock price performance chart for BofA, Citi and Chase. However, it depicts three nearly lock-step institutions, in terms of price moves.

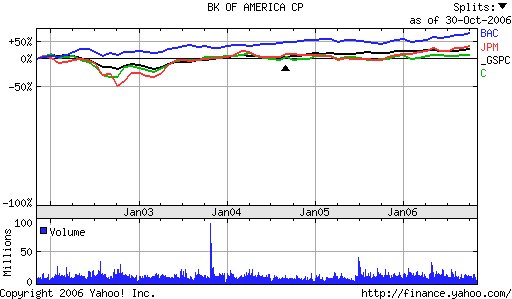

In general, my point has been that none of these financial super-utilities has the slightest chance to consistently outperform the S&P500 anymore. A look at the nearby Yahoo-sourced chart (please click on the chart to see a larger version of it) of the five year performance of Citi, Chase, BofA and the S&P500 illustrates how consistently mediocre the banks have been. Citi is currently the only one which has not, on a point-to-point basis, outperformed the index over five years, although the other banks are doing so only thanks to a recent price runup. Citi, though, has underperformed the index for more than a year, and tracked it, at best, prior to that.

In general, my point has been that none of these financial super-utilities has the slightest chance to consistently outperform the S&P500 anymore. A look at the nearby Yahoo-sourced chart (please click on the chart to see a larger version of it) of the five year performance of Citi, Chase, BofA and the S&P500 illustrates how consistently mediocre the banks have been. Citi is currently the only one which has not, on a point-to-point basis, outperformed the index over five years, although the other banks are doing so only thanks to a recent price runup. Citi, though, has underperformed the index for more than a year, and tracked it, at best, prior to that. None of these financial utilities will consistently earn superior total returns for their shareholders over time. They are simply too large, way beyond the minimum economic size required to operate a financial services business. And their attempts at coordination cost more than the value of the conglomerations.

None of these financial utilities will consistently earn superior total returns for their shareholders over time. They are simply too large, way beyond the minimum economic size required to operate a financial services business. And their attempts at coordination cost more than the value of the conglomerations.As this longer term chart of stock prices depicts, Chase is the only bank to underperform the S&P over the 21 year period, but Citi ceased to outperform the index as of roughly 2000. It's noteworthy that all two of the banks, Chase and Citi, have essentially flat-lined their stock price performance since that year. BofA has merely tracked the S&P for the last few years. None of these financial titans appear to be able to break out of a rut underperforming or merely tracking what an investor can get for total returns from the broader market.

Thus, it can't hurt for Citi to begin undoing the damage that Sandy Weill did to it since his ascension to the top job there so many years ago. If the bank were successfully integrating all of its business in some non-linear, more-than-additive manner, it would show up in the total returns. But it isn't. Like GE, we have a conglomerate that now exists more for senior staff and executive job preservation than for shareholder value creation.

At this point, it's hard to see how shareholders would be worse off by owning, and being offered the opportunity to hold or sell, separated interests in mortgage banking, retail banking, brokerage, institutional banking, and insurance. Each of these Citi units is sufficiently large to self-fund, and would likely prosper when forced to compete and prosper on their own, rather than spend significant resources simply being a compliant part of a financial super-utility.

No comments:

Post a Comment